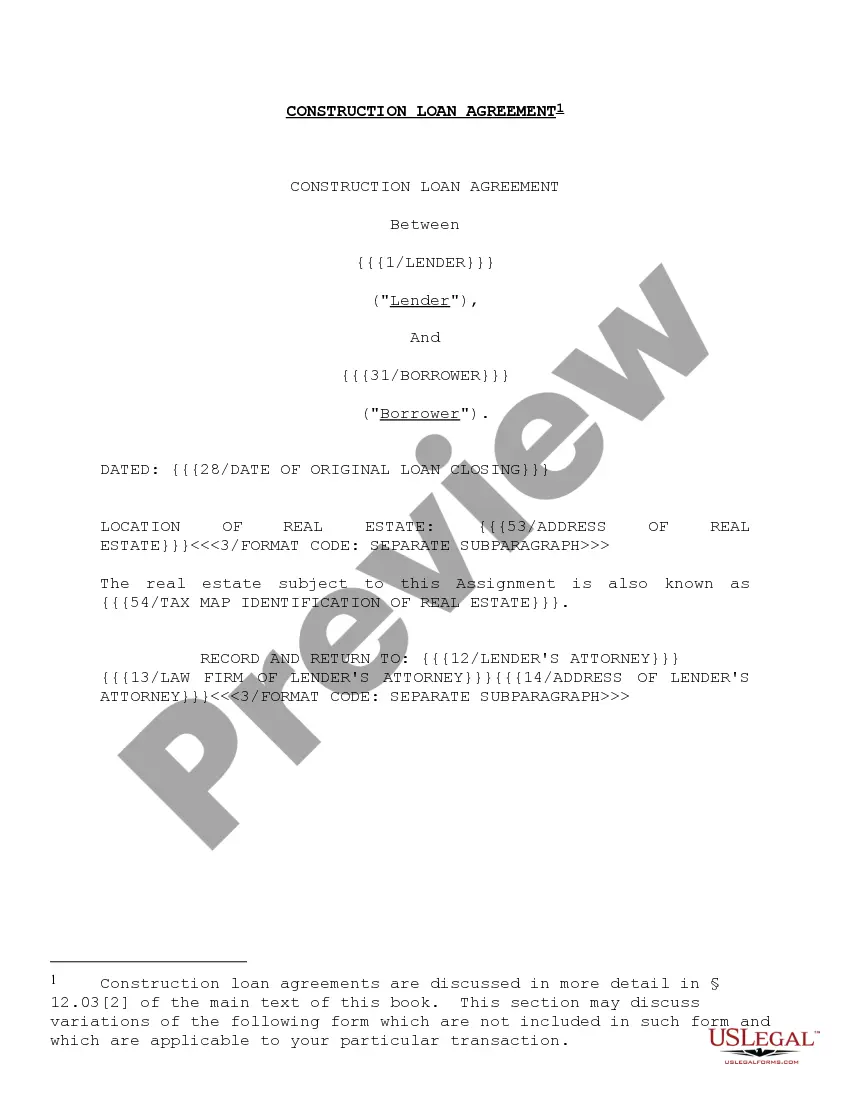

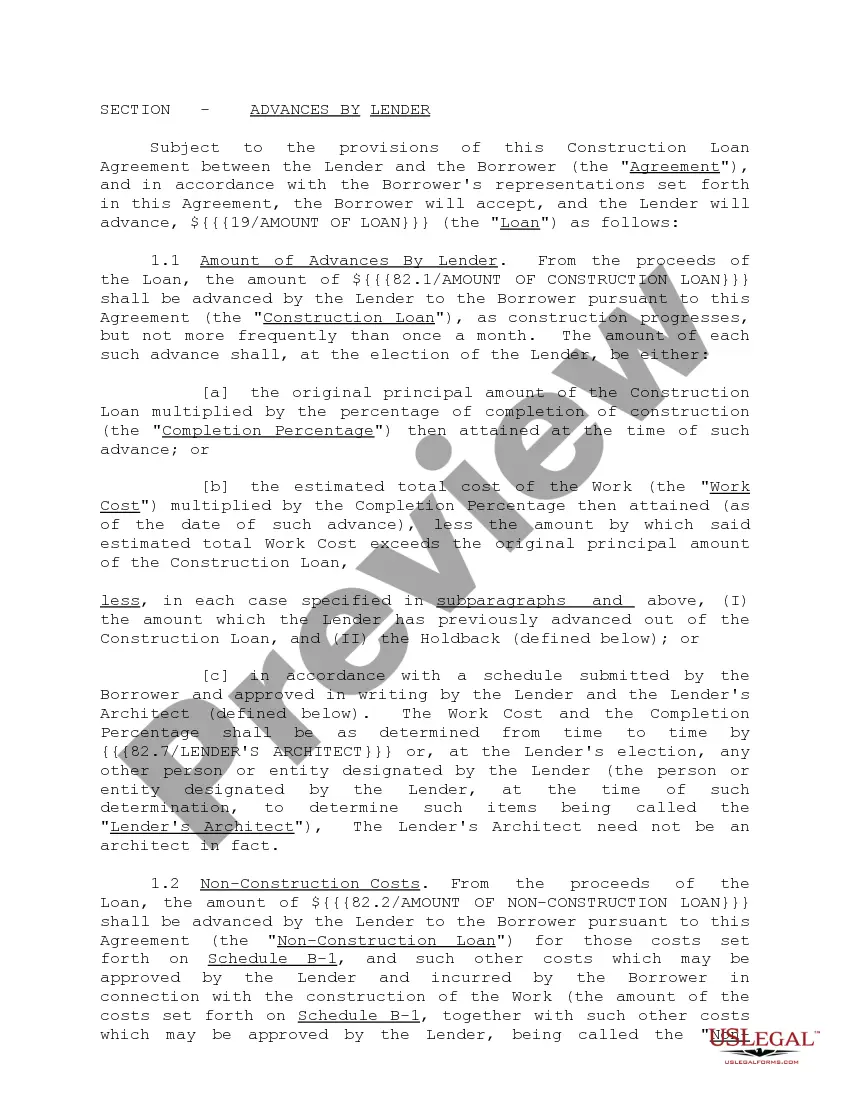

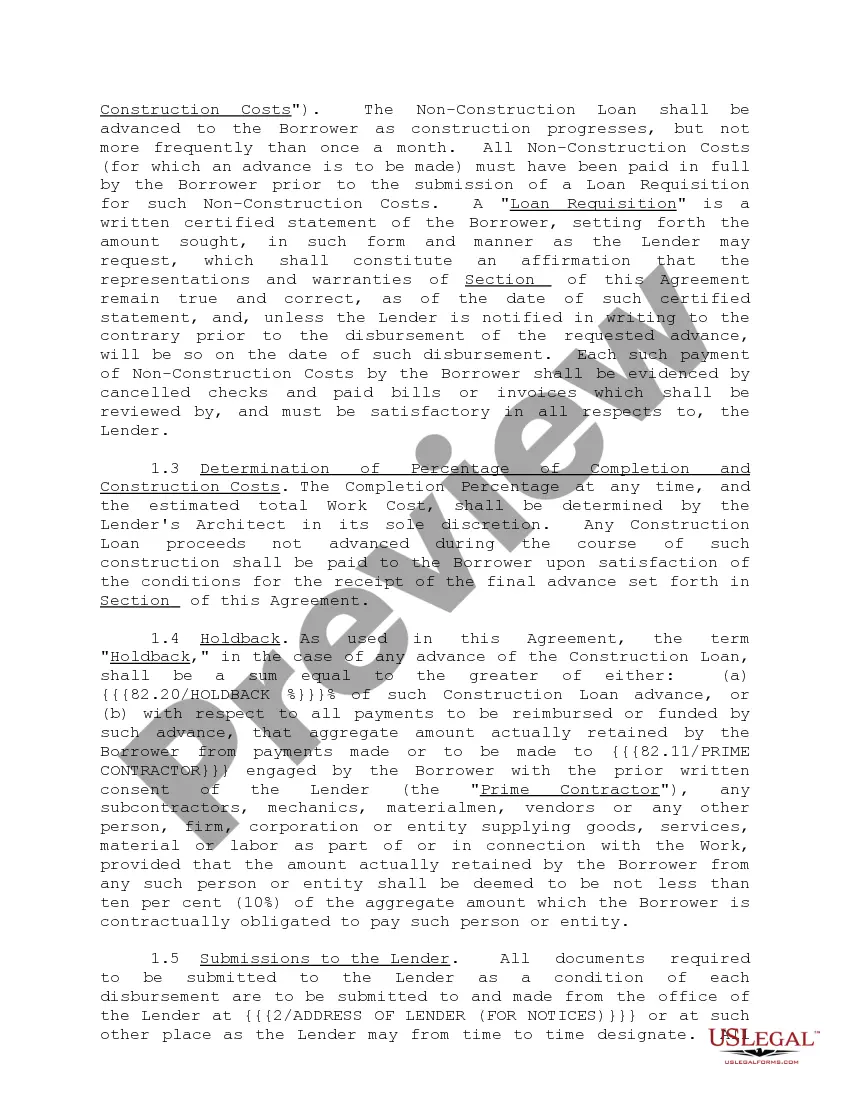

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Indiana Construction Loan Agreements and Variations: A Detailed Description In the realm of construction financing, Indiana Construction Loan Agreements and their variations hold utmost importance. These agreements are legally binding contracts that outline the terms and conditions between lenders and borrowers for financing construction projects in the state of Indiana. They are specifically designed to cater to the unique requirements and complexities of the construction industry. Construction Loan Agreements in Indiana generally consist of several key components. Firstly, they define the parties involved, including the lender, borrower, and any other relevant stakeholders such as contractors, architects, or subcontractors. Secondly, these agreements delineate the amount of the loan, the interest rates, repayment schedules, and any associated fees or penalties. One common type of Indiana Construction Loan Agreement is the Construction-Permanent Loan Agreement. This agreement combines the financing for both the construction phase and the permanent mortgage into a single loan. It offers the borrower the convenience of a single application and closing process, streamlining the overall financing procedure. Another notable variation is the Construction-Only Loan Agreement, which provides financing solely for the construction phase of a project. Under this arrangement, the borrower must secure a separate permanent loan to cover the remaining costs once construction is completed. This type of loan agreement is commonly utilized when borrowers have already arranged their permanent financing or are planning to sell the property shortly after construction. In addition to these variations, there may be other customized loan agreements specific to certain projects or circumstances. These agreements can incorporate provisions such as progress payment schedules, project completion timelines, and mechanisms for handling construction delays or cost overruns. Given the unique nature of the construction industry, Indiana Construction Loan Agreements often include additional clauses that address factors like builder's risk insurance, lien waivers, and compliance with local zoning regulations. These agreements also detail the procedure for approving change orders, which are modifications to the project plans or specifications. It is crucial for both lenders and borrowers to pay close attention to the terms and conditions laid out in Indiana Construction Loan Agreements. By understanding and adhering to these agreements, all parties can ensure smooth construction financing, minimize disputes, and protect their rights and interests. In summary, Indiana Construction Loan Agreements serve as vital tools for facilitating construction projects within the state. Whether it is a Construction-Permanent Loan Agreement or a Construction-Only Loan Agreement, these agreements instill clarity and accountability into the lending process. Properly executed agreements enable builders to secure necessary funds, while lenders mitigate risk and protect their investments. By comprehending the nuances of these loan agreements and their variations, all stakeholders can enhance the success of construction ventures in Indiana.Indiana Construction Loan Agreements and Variations: A Detailed Description In the realm of construction financing, Indiana Construction Loan Agreements and their variations hold utmost importance. These agreements are legally binding contracts that outline the terms and conditions between lenders and borrowers for financing construction projects in the state of Indiana. They are specifically designed to cater to the unique requirements and complexities of the construction industry. Construction Loan Agreements in Indiana generally consist of several key components. Firstly, they define the parties involved, including the lender, borrower, and any other relevant stakeholders such as contractors, architects, or subcontractors. Secondly, these agreements delineate the amount of the loan, the interest rates, repayment schedules, and any associated fees or penalties. One common type of Indiana Construction Loan Agreement is the Construction-Permanent Loan Agreement. This agreement combines the financing for both the construction phase and the permanent mortgage into a single loan. It offers the borrower the convenience of a single application and closing process, streamlining the overall financing procedure. Another notable variation is the Construction-Only Loan Agreement, which provides financing solely for the construction phase of a project. Under this arrangement, the borrower must secure a separate permanent loan to cover the remaining costs once construction is completed. This type of loan agreement is commonly utilized when borrowers have already arranged their permanent financing or are planning to sell the property shortly after construction. In addition to these variations, there may be other customized loan agreements specific to certain projects or circumstances. These agreements can incorporate provisions such as progress payment schedules, project completion timelines, and mechanisms for handling construction delays or cost overruns. Given the unique nature of the construction industry, Indiana Construction Loan Agreements often include additional clauses that address factors like builder's risk insurance, lien waivers, and compliance with local zoning regulations. These agreements also detail the procedure for approving change orders, which are modifications to the project plans or specifications. It is crucial for both lenders and borrowers to pay close attention to the terms and conditions laid out in Indiana Construction Loan Agreements. By understanding and adhering to these agreements, all parties can ensure smooth construction financing, minimize disputes, and protect their rights and interests. In summary, Indiana Construction Loan Agreements serve as vital tools for facilitating construction projects within the state. Whether it is a Construction-Permanent Loan Agreement or a Construction-Only Loan Agreement, these agreements instill clarity and accountability into the lending process. Properly executed agreements enable builders to secure necessary funds, while lenders mitigate risk and protect their investments. By comprehending the nuances of these loan agreements and their variations, all stakeholders can enhance the success of construction ventures in Indiana.