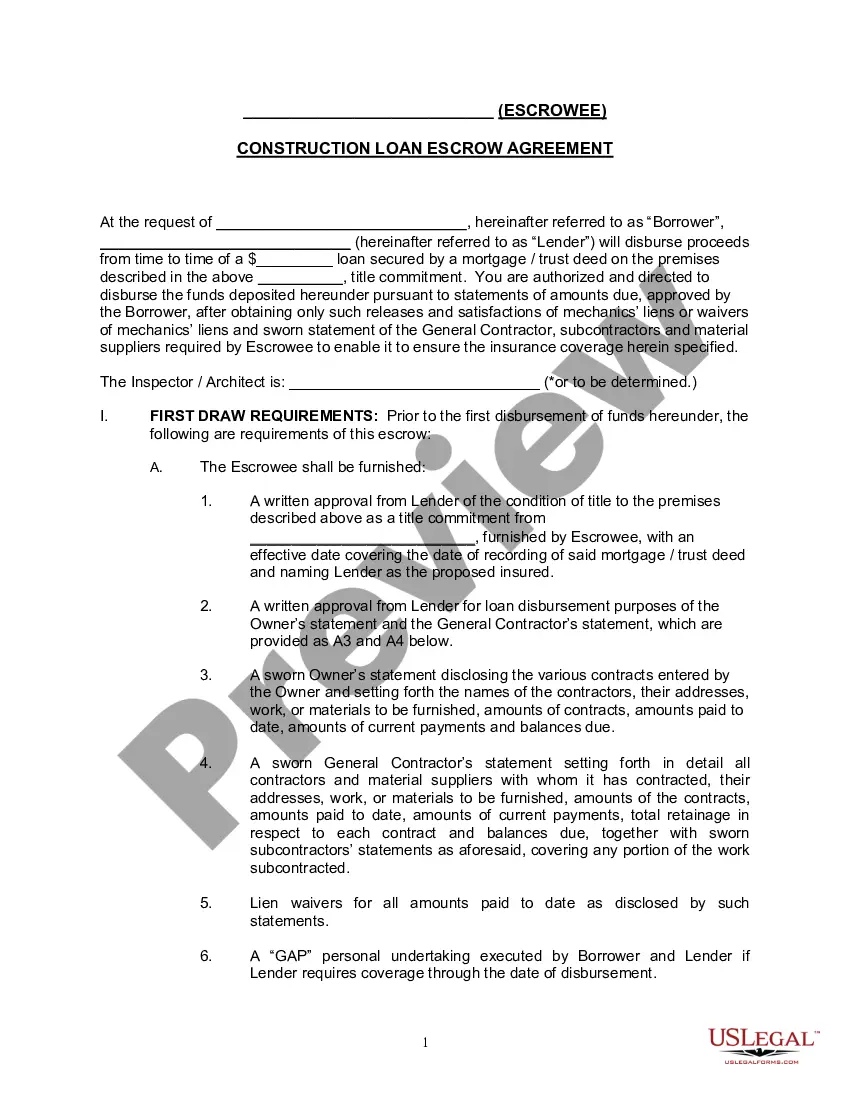

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

Indiana Construction Loan Agreement

Category:

State:

Multi-State

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Construction Loan Agreement?

US Legal Forms - among the largest libraries of lawful varieties in the United States - offers a wide array of lawful papers layouts it is possible to download or produce. Using the internet site, you may get a huge number of varieties for enterprise and specific uses, sorted by classes, claims, or keywords and phrases.You will find the most up-to-date models of varieties much like the Indiana Construction Loan Agreement in seconds.

If you currently have a membership, log in and download Indiana Construction Loan Agreement from your US Legal Forms collection. The Download switch will show up on every develop you see. You have accessibility to all formerly delivered electronically varieties inside the My Forms tab of your respective account.

In order to use US Legal Forms the first time, listed below are basic instructions to obtain started off:

- Make sure you have selected the proper develop for your city/state. Go through the Review switch to review the form`s content material. Browse the develop description to actually have selected the proper develop.

- In the event the develop does not fit your requirements, take advantage of the Look for area at the top of the display screen to find the one that does.

- If you are pleased with the shape, verify your option by simply clicking the Purchase now switch. Then, choose the prices program you favor and offer your credentials to sign up to have an account.

- Procedure the financial transaction. Make use of your charge card or PayPal account to finish the financial transaction.

- Choose the format and download the shape on your system.

- Make adjustments. Load, modify and produce and signal the delivered electronically Indiana Construction Loan Agreement.

Each and every template you added to your account does not have an expiry particular date which is the one you have eternally. So, if you would like download or produce one more duplicate, just visit the My Forms segment and click about the develop you require.

Obtain access to the Indiana Construction Loan Agreement with US Legal Forms, one of the most comprehensive collection of lawful papers layouts. Use a huge number of skilled and state-certain layouts that meet your company or specific requires and requirements.

Form popularity

FAQ

This Deed of Assignment of Loan covers the situation where a lender assigns its rights relating to a loan agreement to a new lender. Only the original lender's rights under the loan agreement (i.e. the right to receive repayment of the loan, and to receive interest) are assigned.

For loans by a commercial lender, the lender will provide the agreement. But for loans between friends or relatives, you will need to create your own loan agreement.

However, the do-it-yourself approach is perfectly acceptable and just as legally enforceable. Once you have both agreed on the terms, you may want to have the personal loan contract notarized or ask a third party to act as a witness during the signing.

What to include in your loan agreement? The amount of the loan, also known as the principal amount. The date of the creation of the loan agreement. The name, address, and contact information of the borrower. The name, address, and contact information of the lender.

Elements of a construction contract Name of contractor and contact information. ... Name of homeowner and contact information. ... Describe property in legal terms. ... List attachments to the contract. ... The cost. ... Failure of homeowner to obtain financing. ... Description of the work and the completion date. ... Right to stop the project.

Top 10 Common Mistakes that We See in Construction Contracts It's not written down. ... Both parties haven't signed the contract. ... Not all of the terms of the agreement are in writing and in the contract. ... The timeline is unclear. ... Particular terms aren't defined. ... There's no written approval of any changes to the contract.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.