This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

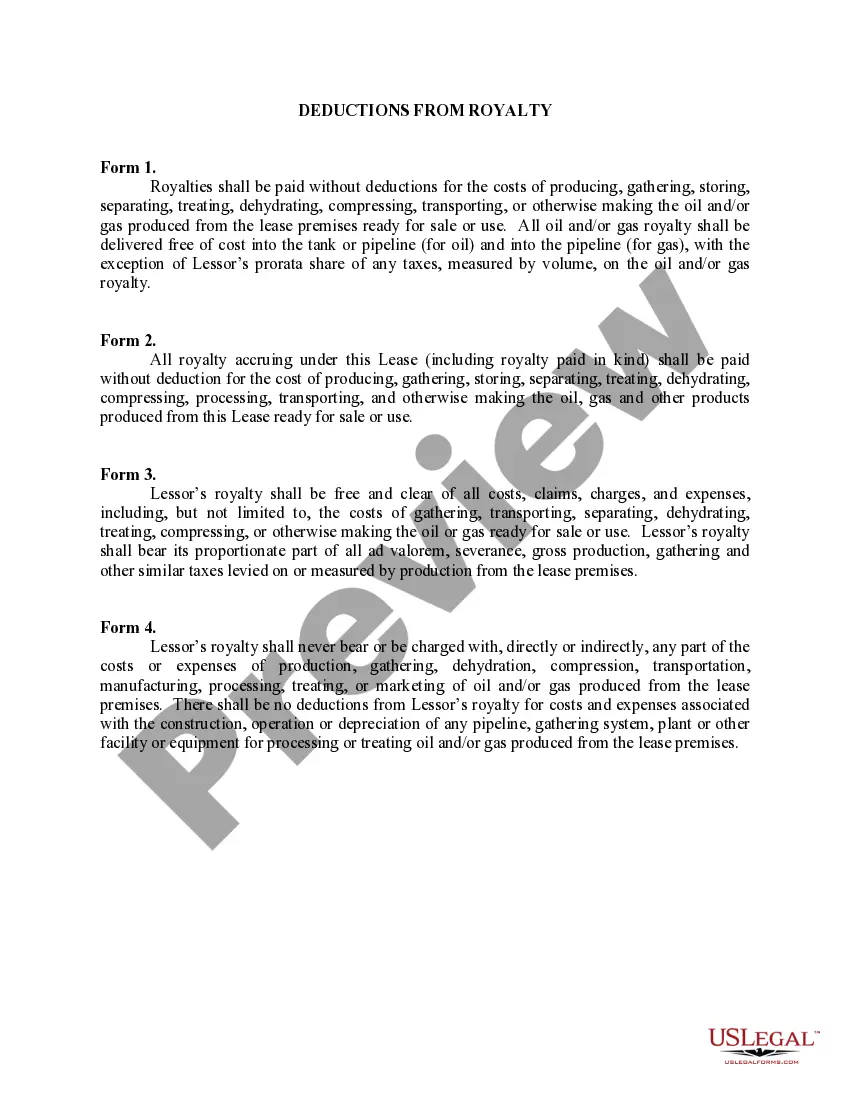

Indiana Deductions from Royalty refers to the various deductions allowed by the state of Indiana pertaining to royalty income earned by individuals or businesses. These deductions help reduce the taxable income derived from royalties, allowing taxpayers to minimize their overall tax liability. Here is a detailed description of the Indiana Deductions from Royalty, along with relevant keywords: 1. Overview: Indiana Deductions from Royalty are provisions outlined by the Indiana Department of Revenue that enable taxpayers to claim deductions for expenses related to royalty income. Royalties include various types of payments received for the use or transfer of intellectual property rights, such as patents, copyrights, trademarks, and mineral rights. 2. Types of Indiana Deductions from Royalty: a. Ordinary and Necessary Expenses: Taxpayers can deduct ordinary and necessary expenses directly related to the production or collection of royalty income. This may include costs incurred for research and development, advertising, and legal fees. b. Depletion Allowance: If the royalty income comes from the extraction or sale of natural resources, such as oil, gas, or minerals, taxpayers can claim a depletion allowance. It enables them to deduct a portion of the income to account for the depletion of the resource. c. Intangible Drilling Costs: In the case of royalty income derived from oil and gas drilling, taxpayers may be eligible to claim intangible drilling costs as deductions. These costs include expenses associated with labor, drilling equipment, fuel, and supplies. 3. Eligibility and Limitations: Taxpayers should meet certain eligibility criteria and comply with specific regulations to claim Indiana Deductions from Royalty. Some key points to consider are: — Deductions are typically available to both individuals and businesses. — Documentation and records supporting the claimed deductions must be maintained. — Limitations may apply based on the type of royalty income and the specific deduction being claimed. — Deductions should comply with federal tax laws and regulations. 4. Claiming Indiana Deductions from Royalty: Taxpayers can claim these deductions while preparing their Indiana state income tax returns. Relevant forms and schedules should be filled out accurately to report the deductible expenses and calculate the reduced taxable income. In conclusion, Indiana Deductions from Royalty provide taxpayers the opportunity to minimize their tax liability by deducting qualifying expenses associated with royalty income. By leveraging these deductions, individuals and businesses can optimize their tax returns and potentially retain a higher portion of their royalty earnings.Indiana Deductions from Royalty refers to the various deductions allowed by the state of Indiana pertaining to royalty income earned by individuals or businesses. These deductions help reduce the taxable income derived from royalties, allowing taxpayers to minimize their overall tax liability. Here is a detailed description of the Indiana Deductions from Royalty, along with relevant keywords: 1. Overview: Indiana Deductions from Royalty are provisions outlined by the Indiana Department of Revenue that enable taxpayers to claim deductions for expenses related to royalty income. Royalties include various types of payments received for the use or transfer of intellectual property rights, such as patents, copyrights, trademarks, and mineral rights. 2. Types of Indiana Deductions from Royalty: a. Ordinary and Necessary Expenses: Taxpayers can deduct ordinary and necessary expenses directly related to the production or collection of royalty income. This may include costs incurred for research and development, advertising, and legal fees. b. Depletion Allowance: If the royalty income comes from the extraction or sale of natural resources, such as oil, gas, or minerals, taxpayers can claim a depletion allowance. It enables them to deduct a portion of the income to account for the depletion of the resource. c. Intangible Drilling Costs: In the case of royalty income derived from oil and gas drilling, taxpayers may be eligible to claim intangible drilling costs as deductions. These costs include expenses associated with labor, drilling equipment, fuel, and supplies. 3. Eligibility and Limitations: Taxpayers should meet certain eligibility criteria and comply with specific regulations to claim Indiana Deductions from Royalty. Some key points to consider are: — Deductions are typically available to both individuals and businesses. — Documentation and records supporting the claimed deductions must be maintained. — Limitations may apply based on the type of royalty income and the specific deduction being claimed. — Deductions should comply with federal tax laws and regulations. 4. Claiming Indiana Deductions from Royalty: Taxpayers can claim these deductions while preparing their Indiana state income tax returns. Relevant forms and schedules should be filled out accurately to report the deductible expenses and calculate the reduced taxable income. In conclusion, Indiana Deductions from Royalty provide taxpayers the opportunity to minimize their tax liability by deducting qualifying expenses associated with royalty income. By leveraging these deductions, individuals and businesses can optimize their tax returns and potentially retain a higher portion of their royalty earnings.