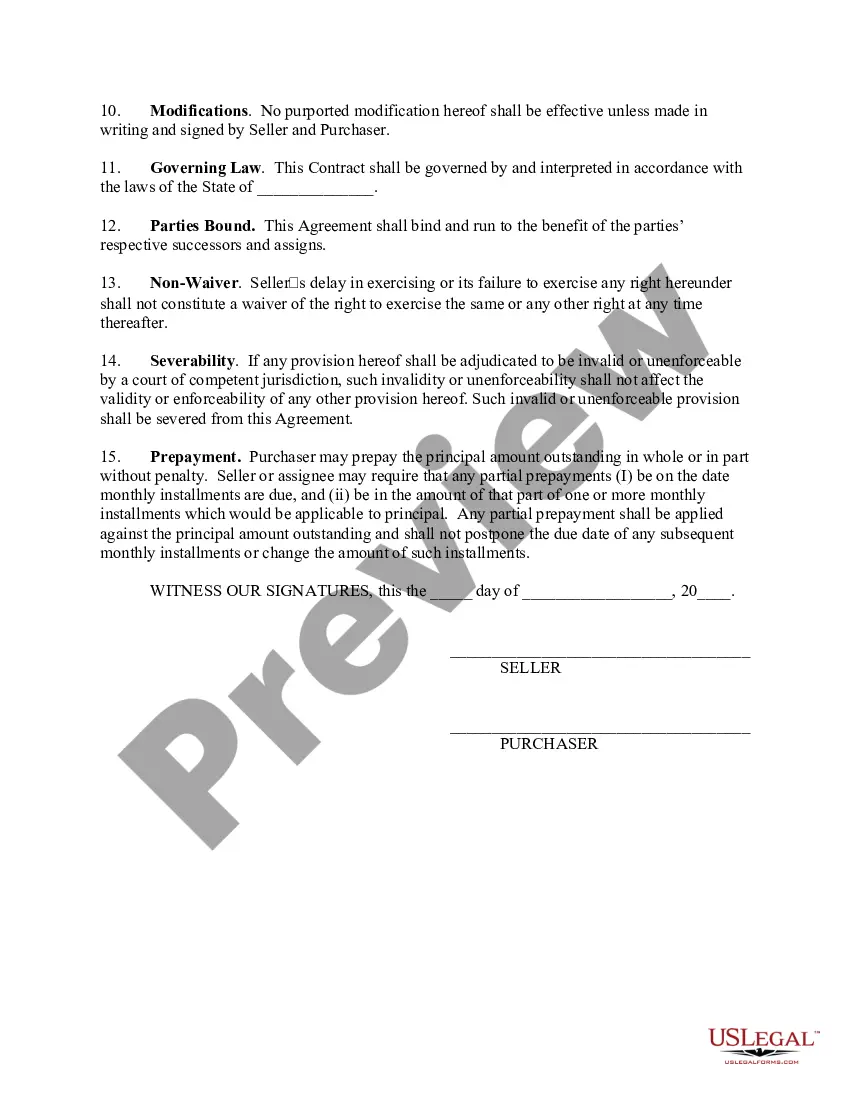

A retail installment agreement is an agreement signed by the Purchaser involving a finance charge and providing for the sale of goods or services. Federal and some State Laws (Consumer Credit Protection Acts) require the disclosure of what the Purchaser is being charged for the credit he/she is receiving. These disclosures include such things as the amount being financed; finance charges; the annual percentage rate; and the number of payments and when due. However, such disclosures are usually only required when a person regularly extends consumer credit (e.g. more than 25 times in the preceding calendar year).

This form is for a casual seller who does not enter into such transactions on a regular basis. It can also be used in commercial transactions (e.g., credit that is not being extended primarily for personal, family, or household purposes).

The Purchaser in this form grants the Seller a security interest in the collateral being sold. A security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. The Seller requires the Purchaser to secure the obligation with the personal property being purchased so that if the Purchaser does not pay as promised, the Purchaser can take the collateral back, sell it, and apply the proceeds against the unpaid obligation of the Purchaser.

A Kansas Retail Installment Contract or Agreement refers to a legally binding document between a consumer and a retail seller for the purchase of goods or services. This agreement sets out the terms and conditions of the transaction, including the purchase price, interest rates, payment schedule, and any additional charges or fees. In Kansas, there are two main types of Retail Installment Contracts or Agreements: 1. Closed-end Retail Installment Contract: This type of agreement is commonly used for a one-time purchase of a product or service. The total cost of the purchase, including any interest or finance charges, is predetermined and stated in the contract. The consumer agrees to pay the amount in installments over a specified period. Once all payments are made, the contract is considered fulfilled, and the consumer becomes the owner of the purchased item. 2. Open-end Retail Installment Agreement: This type of agreement is typically used for revolving credit accounts, such as store credit cards. Unlike closed-end contracts, open-end agreements have no fixed end date. Consumers can make purchases up to a predetermined credit limit and are required to make minimum monthly payments based on the outstanding balance. Interest is charged on the unpaid balance. Both types of agreements must comply with the Kansas Retail Installment Sales Act, which regulates consumer protection in retail transactions. This act specifies certain requirements for these contracts, including the disclosure of the annual percentage rate (APR), prepayment penalties, and late payment fees. The agreement must also clearly state the consumer's rights to cancel or rescind the contract within a specified period. Failure to comply with the Kansas Retail Installment Sales Act may result in legal consequences for the retail seller, including fines, penalties, or rescission of the contract. In summary, a Kansas Retail Installment Contract or Agreement is a legal document that outlines the terms and conditions of a retail purchase and provides protection for consumers in the state. The two main types are closed-end and open-end contracts, each with its own features and obligations.A Kansas Retail Installment Contract or Agreement refers to a legally binding document between a consumer and a retail seller for the purchase of goods or services. This agreement sets out the terms and conditions of the transaction, including the purchase price, interest rates, payment schedule, and any additional charges or fees. In Kansas, there are two main types of Retail Installment Contracts or Agreements: 1. Closed-end Retail Installment Contract: This type of agreement is commonly used for a one-time purchase of a product or service. The total cost of the purchase, including any interest or finance charges, is predetermined and stated in the contract. The consumer agrees to pay the amount in installments over a specified period. Once all payments are made, the contract is considered fulfilled, and the consumer becomes the owner of the purchased item. 2. Open-end Retail Installment Agreement: This type of agreement is typically used for revolving credit accounts, such as store credit cards. Unlike closed-end contracts, open-end agreements have no fixed end date. Consumers can make purchases up to a predetermined credit limit and are required to make minimum monthly payments based on the outstanding balance. Interest is charged on the unpaid balance. Both types of agreements must comply with the Kansas Retail Installment Sales Act, which regulates consumer protection in retail transactions. This act specifies certain requirements for these contracts, including the disclosure of the annual percentage rate (APR), prepayment penalties, and late payment fees. The agreement must also clearly state the consumer's rights to cancel or rescind the contract within a specified period. Failure to comply with the Kansas Retail Installment Sales Act may result in legal consequences for the retail seller, including fines, penalties, or rescission of the contract. In summary, a Kansas Retail Installment Contract or Agreement is a legal document that outlines the terms and conditions of a retail purchase and provides protection for consumers in the state. The two main types are closed-end and open-end contracts, each with its own features and obligations.