A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

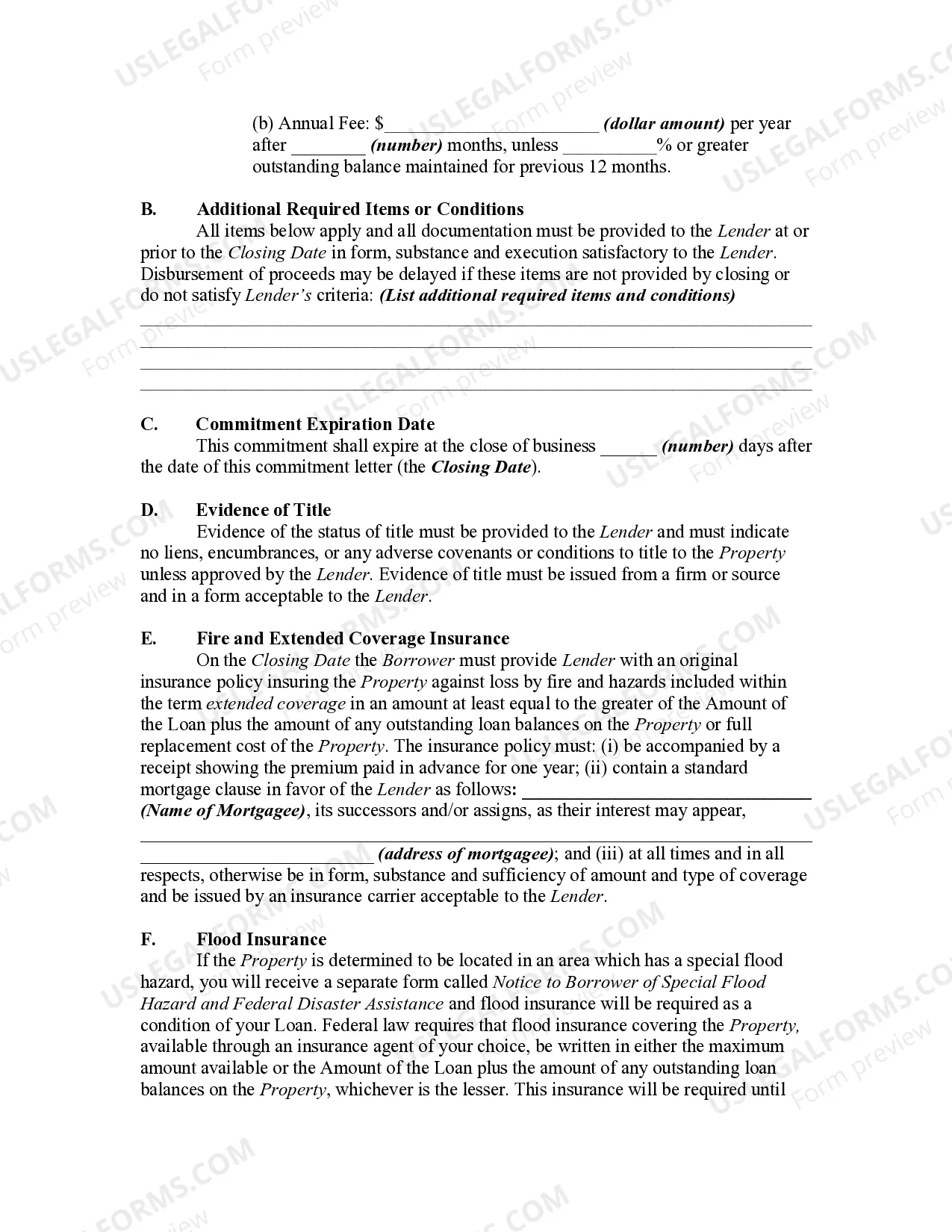

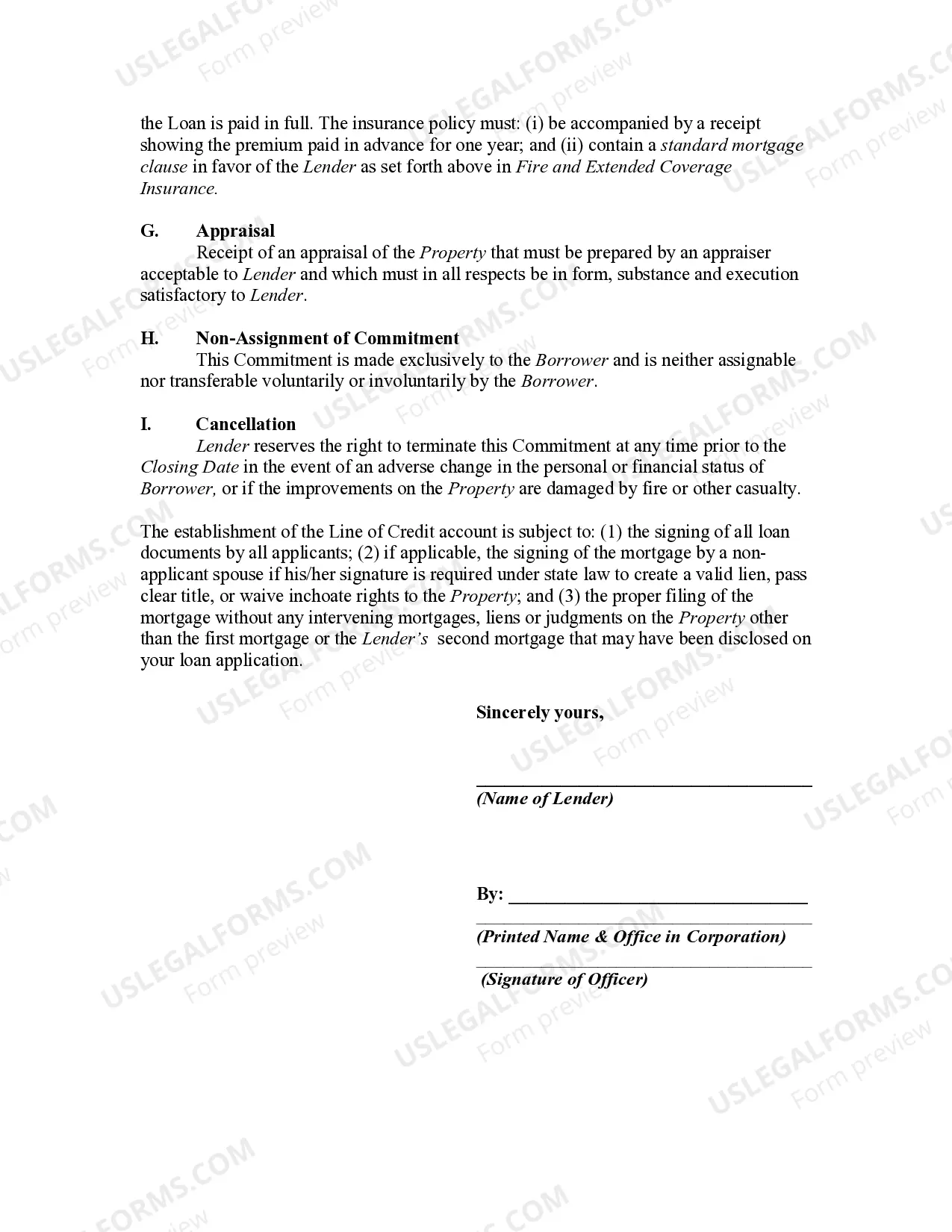

A Kansas Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a legal agreement between a borrower and a lender that outlines the terms and conditions for borrowing against the equity in a Kansas property. This type of loan commitment allows homeowners to access a line of credit using their home's equity as collateral. Helots are often used for home improvement projects, debt consolidation, or other major expenses. The Kansas Mortgage Loan Commitment for HELOT typically includes information such as the loan amount, interest rate, repayment terms, and any additional fees or charges associated with the loan. There are several types of Kansas Mortgage Loan Commitment for Home Equity Line of Credit. These variations are designed to cater to different financial needs and preferences of borrowers. Some common types of Helots available in Kansas include: 1. Fixed-Rate HELOT: This type of commitment offers a fixed interest rate throughout the loan term, providing stability in monthly payments. 2. Variable-Rate HELOT: With a variable rate commitment, the interest rate fluctuates based on market conditions, potentially resulting in varying monthly payments. 3. Open-End HELOT: An open-end commitment allows borrowers to continuously borrow against the line of credit during the draw period without needing to reapply for a new loan. 4. Closed-End HELOT: In contrast to an open-end commitment, a closed-end HELOT provides a one-time lump sum disbursement of funds, similar to a traditional mortgage, and does not allow for future borrowing against the line of credit. 5. Interest-Only HELOT: With an interest-only commitment, borrowers are only required to pay the interest on the loan during the draw period, allowing for lower monthly payments. It is crucial to carefully review the terms and conditions of a Kansas Mortgage Loan Commitment for HELOT and understand the implications of each type before choosing the best option. Consulting with a mortgage professional or financial advisor can help borrowers make an informed decision based on their specific financial situation and goals.A Kansas Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a legal agreement between a borrower and a lender that outlines the terms and conditions for borrowing against the equity in a Kansas property. This type of loan commitment allows homeowners to access a line of credit using their home's equity as collateral. Helots are often used for home improvement projects, debt consolidation, or other major expenses. The Kansas Mortgage Loan Commitment for HELOT typically includes information such as the loan amount, interest rate, repayment terms, and any additional fees or charges associated with the loan. There are several types of Kansas Mortgage Loan Commitment for Home Equity Line of Credit. These variations are designed to cater to different financial needs and preferences of borrowers. Some common types of Helots available in Kansas include: 1. Fixed-Rate HELOT: This type of commitment offers a fixed interest rate throughout the loan term, providing stability in monthly payments. 2. Variable-Rate HELOT: With a variable rate commitment, the interest rate fluctuates based on market conditions, potentially resulting in varying monthly payments. 3. Open-End HELOT: An open-end commitment allows borrowers to continuously borrow against the line of credit during the draw period without needing to reapply for a new loan. 4. Closed-End HELOT: In contrast to an open-end commitment, a closed-end HELOT provides a one-time lump sum disbursement of funds, similar to a traditional mortgage, and does not allow for future borrowing against the line of credit. 5. Interest-Only HELOT: With an interest-only commitment, borrowers are only required to pay the interest on the loan during the draw period, allowing for lower monthly payments. It is crucial to carefully review the terms and conditions of a Kansas Mortgage Loan Commitment for HELOT and understand the implications of each type before choosing the best option. Consulting with a mortgage professional or financial advisor can help borrowers make an informed decision based on their specific financial situation and goals.