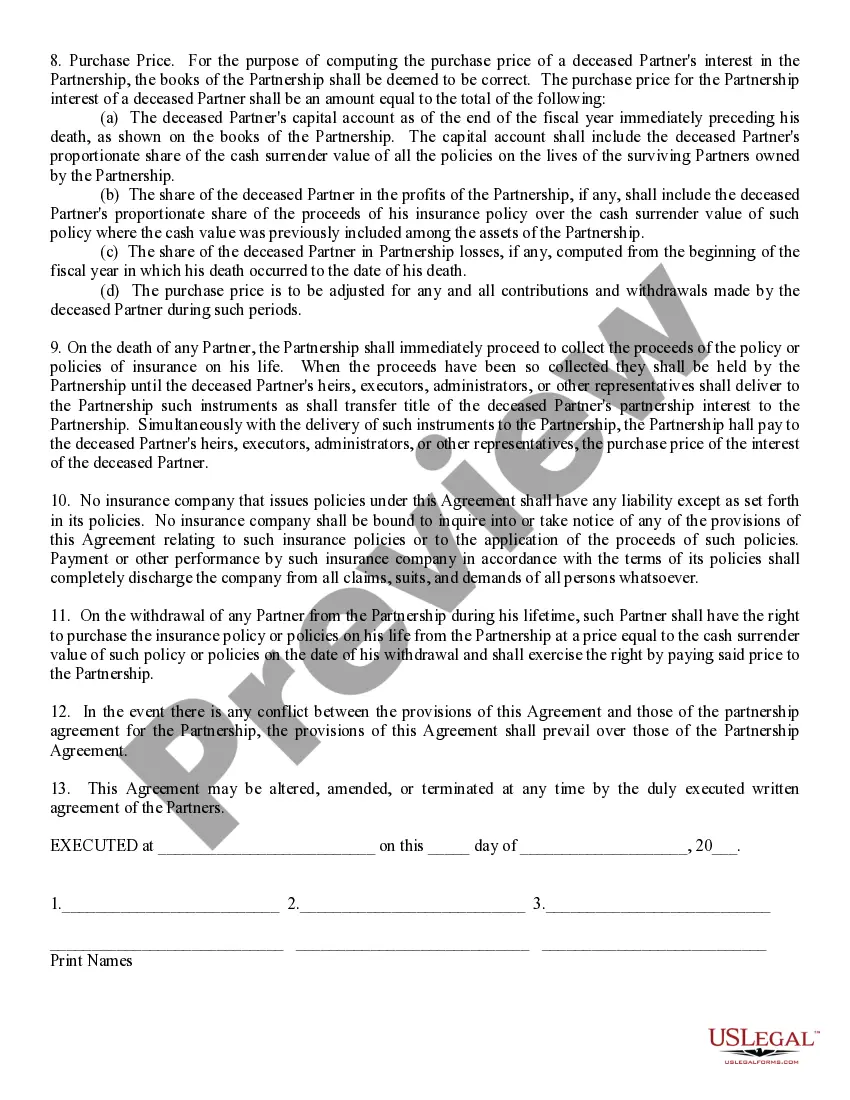

The Kansas Sale of Deceased Partner's Interest refers to the legal process involved in the transfer or sale of a deceased partner's ownership stake or interest in a business located in the state of Kansas. This procedure is critical in managing the affairs of a business and ensuring a smooth transition of ownership after the death of a partner. In the event of a partner's death, it is crucial for the remaining partners to understand their rights and obligations in selling the deceased partner's interest. The Kansas Revised Uniform Partnership Act (GUPTA) provides guidelines and regulations for the sale of such interests, acting as a legal framework to ensure fairness and transparency. There are several types of Kansas Sale of Deceased Partner's Interest, which include: 1. Voluntary Sale: In certain cases, partners may agree to sell their deceased partner's interest voluntarily, without any legal disputes. This type of sale typically occurs when partners have a pre-existing buy-sell agreement or when the deceased partner has provided written instructions for the sale in their will or estate planning documents. 2. Judicial Sale: If the remaining partners cannot agree on a voluntary sale, the matter may be taken to court. The court will oversee the sale process and ensure that the deceased partner's interest is sold fairly and for a reasonable value. The proceeds from the sale will then be distributed in accordance with Kansas probate laws. 3. Public Auction: In some situations, the deceased partner's interest may be sold through a public auction. This method involves listing the interest for sale and allowing interested parties to bid on it. The highest bidder will ultimately purchase the interest, and funds will be distributed according to applicable laws and agreements. The process of Kansas Sale of Deceased Partner's Interest involves several steps. Initially, the partners must determine whether there are any pre-existing agreements or provisions in place that regulate the sale of a partner's interest upon death. If so, these agreements will dictate the specifics of the sale process. If there is no pre-existing agreement, the remaining partners must work together to establish a fair market value for the deceased partner's interest. This may involve consulting with appraisers or financial advisors to assess the business's overall value and the deceased partner's share. Once the value is determined, the partners can proceed with the chosen method of sale: voluntary, judicial, or public auction. During this phase, legal paperwork, including necessary filings and documents, must be prepared to facilitate the sale process. Upon completion of the sale, the proceeds will be distributed among the partners in accordance with the partnership agreement or Kansas probate laws. It is crucial for the parties involved to adhere to legal procedures and consult with legal professionals to ensure compliance with Kansas partnership laws and regulations. In summary, the Kansas Sale of Deceased Partner's Interest encompasses various types and procedures for transferring a deceased partner's ownership stake in a business. Understanding these processes and seeking appropriate legal guidance is essential for a smooth and legally compliant transition of ownership.

Kansas Sale of Deceased Partner's Interest

Description

How to fill out Kansas Sale Of Deceased Partner's Interest?

US Legal Forms - one of the most significant libraries of lawful forms in the United States - gives a variety of lawful file themes you may down load or produce. Making use of the internet site, you may get a large number of forms for business and individual reasons, categorized by types, claims, or search phrases.You can find the latest variations of forms like the Kansas Sale of Deceased Partner's Interest within minutes.

If you already have a registration, log in and down load Kansas Sale of Deceased Partner's Interest from the US Legal Forms collection. The Acquire switch can look on every single form you look at. You get access to all previously delivered electronically forms from the My Forms tab of your own accounts.

If you would like use US Legal Forms the very first time, allow me to share simple guidelines to get you started:

- Ensure you have picked the best form to your town/region. Click on the Review switch to check the form`s content. Read the form explanation to actually have chosen the right form.

- In case the form doesn`t match your requirements, utilize the Research area on top of the monitor to obtain the the one that does.

- Should you be satisfied with the shape, confirm your selection by simply clicking the Acquire now switch. Then, pick the costs plan you favor and provide your credentials to register for the accounts.

- Process the deal. Utilize your Visa or Mastercard or PayPal accounts to perform the deal.

- Select the structure and down load the shape on your system.

- Make adjustments. Fill up, revise and produce and indicator the delivered electronically Kansas Sale of Deceased Partner's Interest.

Every template you included in your bank account does not have an expiration date and is also your own property for a long time. So, in order to down load or produce yet another version, just visit the My Forms area and then click in the form you want.

Gain access to the Kansas Sale of Deceased Partner's Interest with US Legal Forms, the most considerable collection of lawful file themes. Use a large number of specialist and status-particular themes that satisfy your organization or individual demands and requirements.