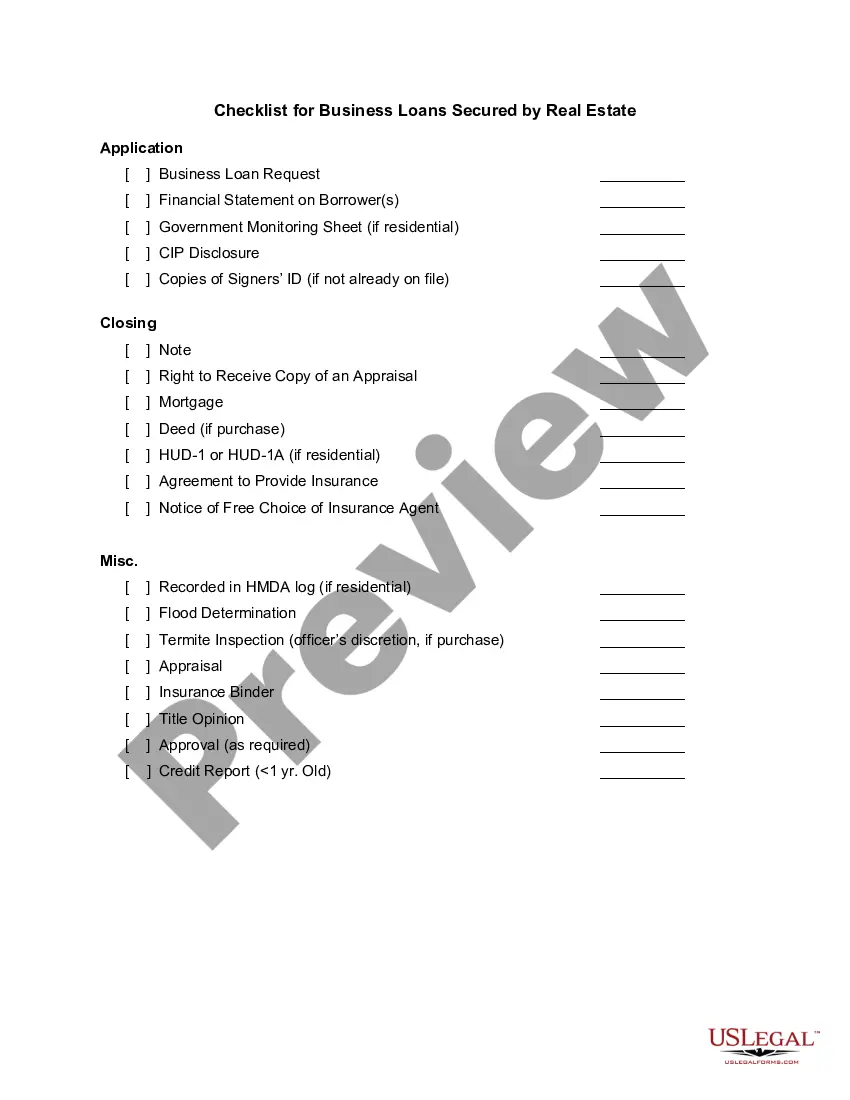

Kansas Checklist for Business Loans Secured by Real Estate: A Comprehensive Guide In Kansas, securing a business loan using real estate as collateral requires careful consideration and adherence to specific guidelines. To help potential borrowers navigate the lending process, the Kansas checklist for business loans secured by real estate offers a detailed breakdown of the requirements and steps involved. Here, we will outline the key factors involved in securing such loans and highlight various types of business loans available in Kansas. 1. Loan Application Documentation: To initiate the loan application process, borrowers must gather essential documentation, including their business plan, financial statements (both personal and business), tax returns, credit reports, and any additional information that demonstrates the feasibility and viability of their business. 2. Property Evaluation: Lenders in Kansas will evaluate the property offered as collateral to assess its value and determine the loan amount eligible for approval. An appraisal, typically conducted by a certified professional, will be required to determine the current market value and ensure it aligns with the loan request. 3. Loan-to-Value Ratio: The loan-to-value (LTV) ratio is an essential consideration for lenders. Typically, they will lend up to a certain percentage of the property's value, often around 70-80% of the appraised value. A higher LTV ratio may signify higher collateral risk, potentially impacting the loan terms or interest rates. 4. Debt-Service Coverage Ratio: Lenders pay particular attention to the debt-service coverage ratio (DSC), which indicates the borrower's ability to cover loan payments. Kansas lenders typically require a DSC of at least 1.25 or higher, ensuring that the property's income will sufficiently cover the mortgage payments. 5. Personal Credit and Financial History: Alongside the property evaluation, lenders will scrutinize the borrower's personal credit history, financial standing, and previous loan repayments. A solid credit score is crucial to demonstrate reliability and creditworthiness, increasing the chances of loan approval. Types of Kansas Checklist for Business Loans Secured by Real Estate: 1. Commercial Real Estate Loans: These loans are specifically designed to finance commercial properties such as retail spaces, offices, warehouses, or industrial facilities. Kansas lenders assess the property's value and its potential income-generating capability while considering the borrower's financial stability. 2. Agricultural Loans: Kansas's agricultural sector is significant, and securing loans for farming operations, ranches, or agricultural properties is relatively common. Lenders evaluate the rural property's potential income, the borrower's expertise in the agricultural sector, and the viability of the farming operation. 3. Construction Loans: Individuals or businesses seeking funds for constructing or renovating commercial properties can explore construction loans secured by real estate. Kansas lenders will assess the construction plans, projected budgets, and repayments based on the property's future value. 4. Small Business Administration (SBA) Loans: In collaboration with the Small Business Administration, banks and lenders offer SBA loans, encouraging the growth and development of small businesses. These loans typically require real estate collateral and follow the SBA's guidelines and criteria for eligibility. Securing a business loan secured by real estate in Kansas involves meticulous planning, documentation, and meeting lender-specific criteria. By adhering to the Kansas checklist for business loans secured by real estate, borrowers can increase their chances of obtaining the necessary funds to fuel their business growth and achieve their entrepreneurial goals.

Kansas Checklist for Business Loans Secured by Real Estate

Description

How to fill out Kansas Checklist For Business Loans Secured By Real Estate?

US Legal Forms - one of the most significant libraries of legal kinds in the United States - provides an array of legal record web templates you may down load or print. Using the internet site, you can get a huge number of kinds for business and personal functions, sorted by classes, suggests, or keywords and phrases.You will find the most recent types of kinds like the Kansas Checklist for Business Loans Secured by Real Estate in seconds.

If you have a subscription, log in and down load Kansas Checklist for Business Loans Secured by Real Estate from your US Legal Forms collection. The Acquire key can look on each and every kind you view. You have accessibility to all earlier saved kinds from the My Forms tab of your respective accounts.

If you wish to use US Legal Forms initially, listed here are easy guidelines to help you started out:

- Be sure to have selected the proper kind for the city/area. Click on the Preview key to analyze the form`s articles. Browse the kind explanation to actually have chosen the correct kind.

- In the event the kind doesn`t match your demands, utilize the Search field near the top of the display screen to find the the one that does.

- If you are satisfied with the shape, validate your option by clicking the Buy now key. Then, choose the prices strategy you favor and give your accreditations to sign up for the accounts.

- Method the financial transaction. Make use of your bank card or PayPal accounts to complete the financial transaction.

- Choose the structure and down load the shape on your own system.

- Make alterations. Fill out, edit and print and signal the saved Kansas Checklist for Business Loans Secured by Real Estate.

Every design you included in your bank account does not have an expiry particular date and is also your own permanently. So, in order to down load or print yet another duplicate, just check out the My Forms section and then click around the kind you need.

Gain access to the Kansas Checklist for Business Loans Secured by Real Estate with US Legal Forms, probably the most considerable collection of legal record web templates. Use a huge number of expert and express-distinct web templates that satisfy your organization or personal requires and demands.