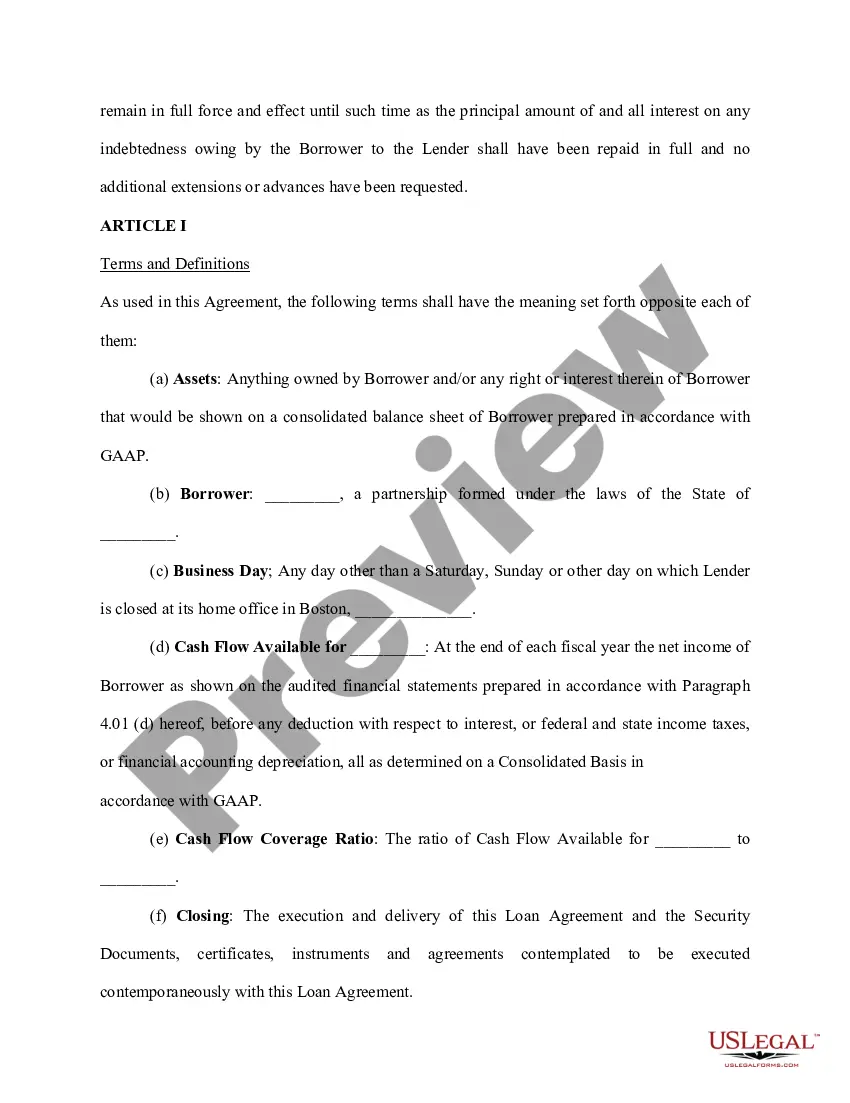

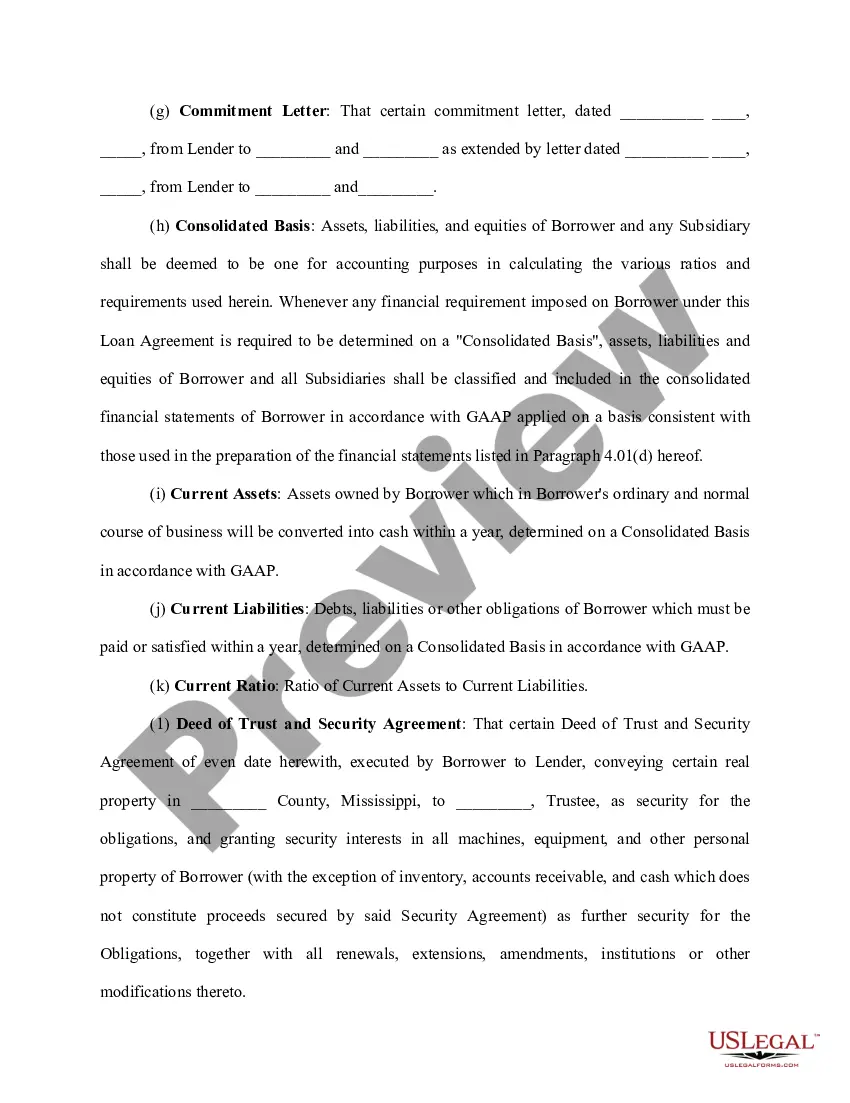

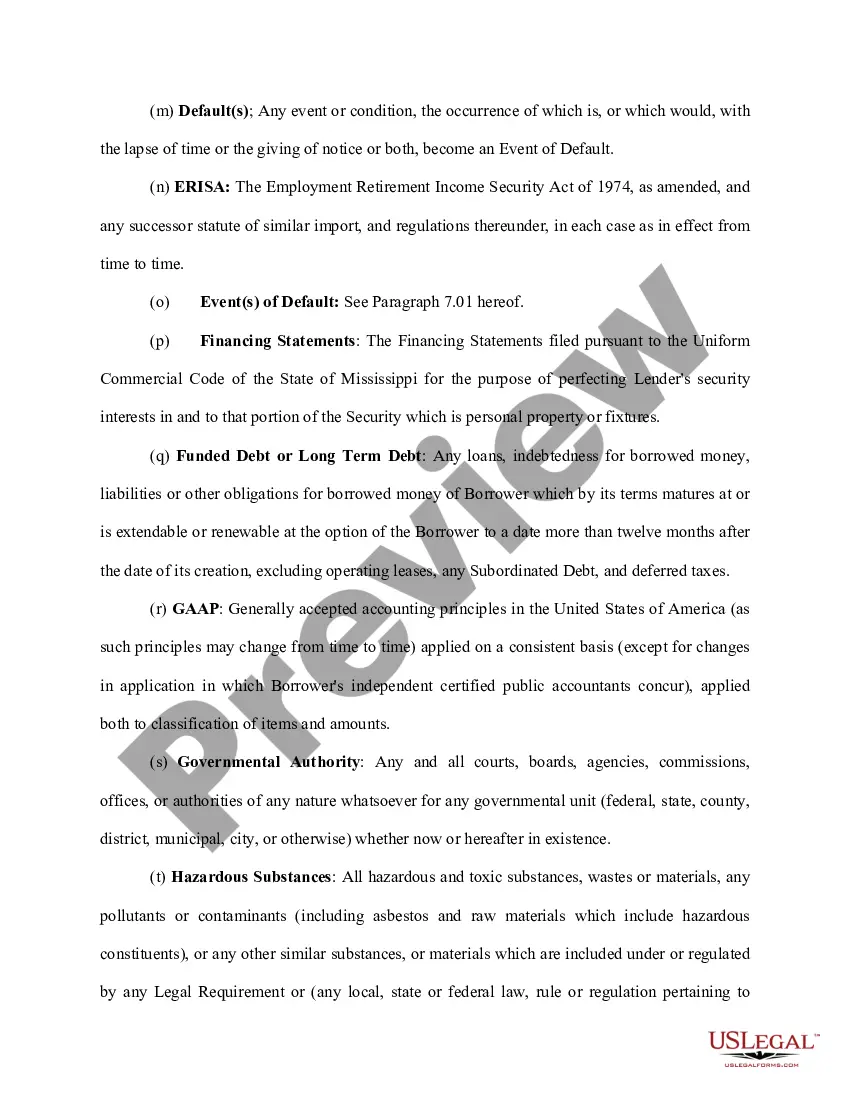

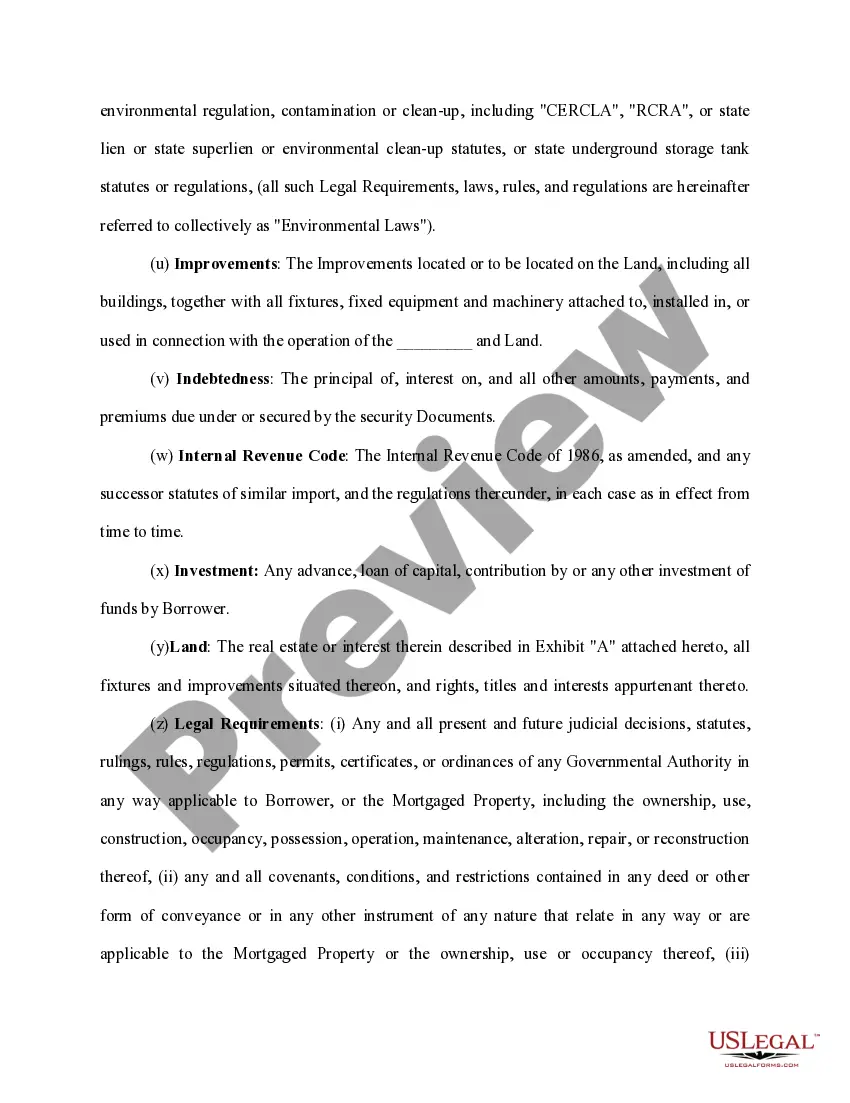

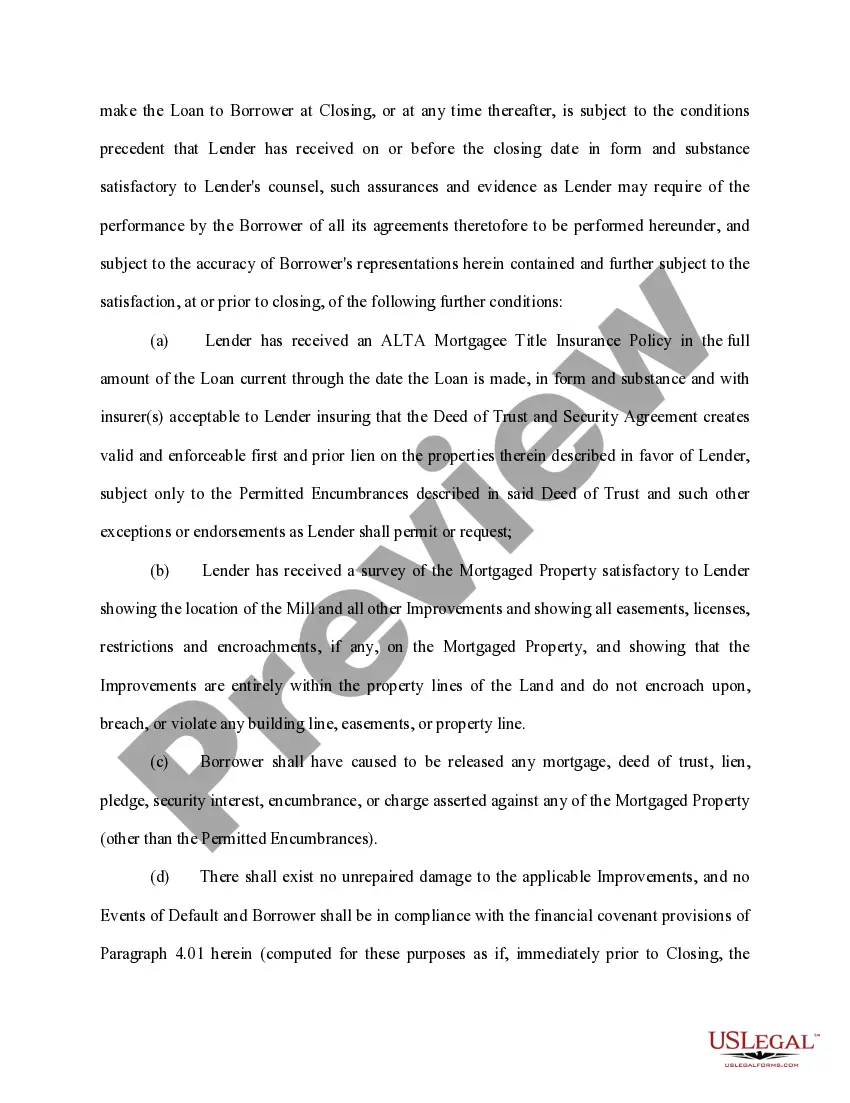

A Kansas Loan Agreement is a legal document that outlines the terms and conditions surrounding a loan transaction between a lender and a borrower in the state of Kansas. This agreement serves as evidence of the loan and provides clarity to both parties regarding their rights and obligations. The Kansas Loan Agreement typically includes important details such as the names and contact information of the lender and borrower, the loan amount, the interest rate or finance charges, the repayment schedule, and any collateral or security provided by the borrower. It also outlines the consequences of defaulting on the loan and any applicable fees or penalties. There are several types of Kansas Loan Agreements, each tailored to different circumstances and loan arrangements. Some common types include: 1. Personal Loan Agreement: This type of loan is usually made between individuals for personal expenses, such as medical bills, vacations, or home renovations. The agreement specifies the terms for repayment, including the interest rate and the schedule. 2. Business Loan Agreement: This agreement is used when a business or entrepreneur needs financial assistance to grow their enterprise or cover operational expenses. It establishes the loan amount, interest rate, repayment terms, and any assets pledged as collateral. 3. Mortgage Loan Agreement: When purchasing a property, a mortgage loan agreement is created to specify the terms of the loan, including the principal amount, interest rate, repayment schedule, and the property's collateral. 4. Student Loan Agreement: This agreement is used when individuals borrow money to fund their education. It outlines the terms of repayment, including any available repayment plans, interest rates, and deferment or forbearance options. 5. Auto Loan Agreement: When purchasing a vehicle, an auto loan agreement specifies the loan amount, interest rate, repayment terms, and any collateral or security agreements related to the vehicle. 6. Payday Loan Agreement: Payday loans are short-term loans typically used for emergency situations. This agreement outlines the loan amount, fees, repayment schedule, and any penalties for late payment or default. It is crucial for both lenders and borrowers to carefully review and understand the terms and conditions set forth in a Kansas Loan Agreement before signing. Seeking legal advice or consulting with a financial professional can provide additional guidance and ensure compliance with applicable laws and regulations.

Kansas Loan Agreement

Description

How to fill out Kansas Loan Agreement?

Choosing the right legal papers design can be a have difficulties. Naturally, there are a lot of themes available online, but how can you get the legal kind you will need? Make use of the US Legal Forms internet site. The services delivers a large number of themes, such as the Kansas Loan Agreement, which can be used for company and personal requires. Each of the forms are checked out by professionals and satisfy federal and state specifications.

In case you are already authorized, log in in your profile and click the Obtain key to find the Kansas Loan Agreement. Use your profile to check throughout the legal forms you possess bought earlier. Visit the My Forms tab of your profile and acquire yet another version in the papers you will need.

In case you are a new user of US Legal Forms, here are simple directions so that you can follow:

- First, make sure you have selected the proper kind for your personal city/region. You may look through the form while using Preview key and look at the form description to make sure this is the right one for you.

- In case the kind does not satisfy your expectations, make use of the Seach discipline to get the proper kind.

- Once you are positive that the form is suitable, click on the Buy now key to find the kind.

- Choose the prices strategy you want and type in the needed details. Design your profile and pay money for the order using your PayPal profile or Visa or Mastercard.

- Choose the file format and down load the legal papers design in your system.

- Total, change and printing and sign the obtained Kansas Loan Agreement.

US Legal Forms will be the largest collection of legal forms in which you will find a variety of papers themes. Make use of the service to down load professionally-manufactured papers that follow state specifications.