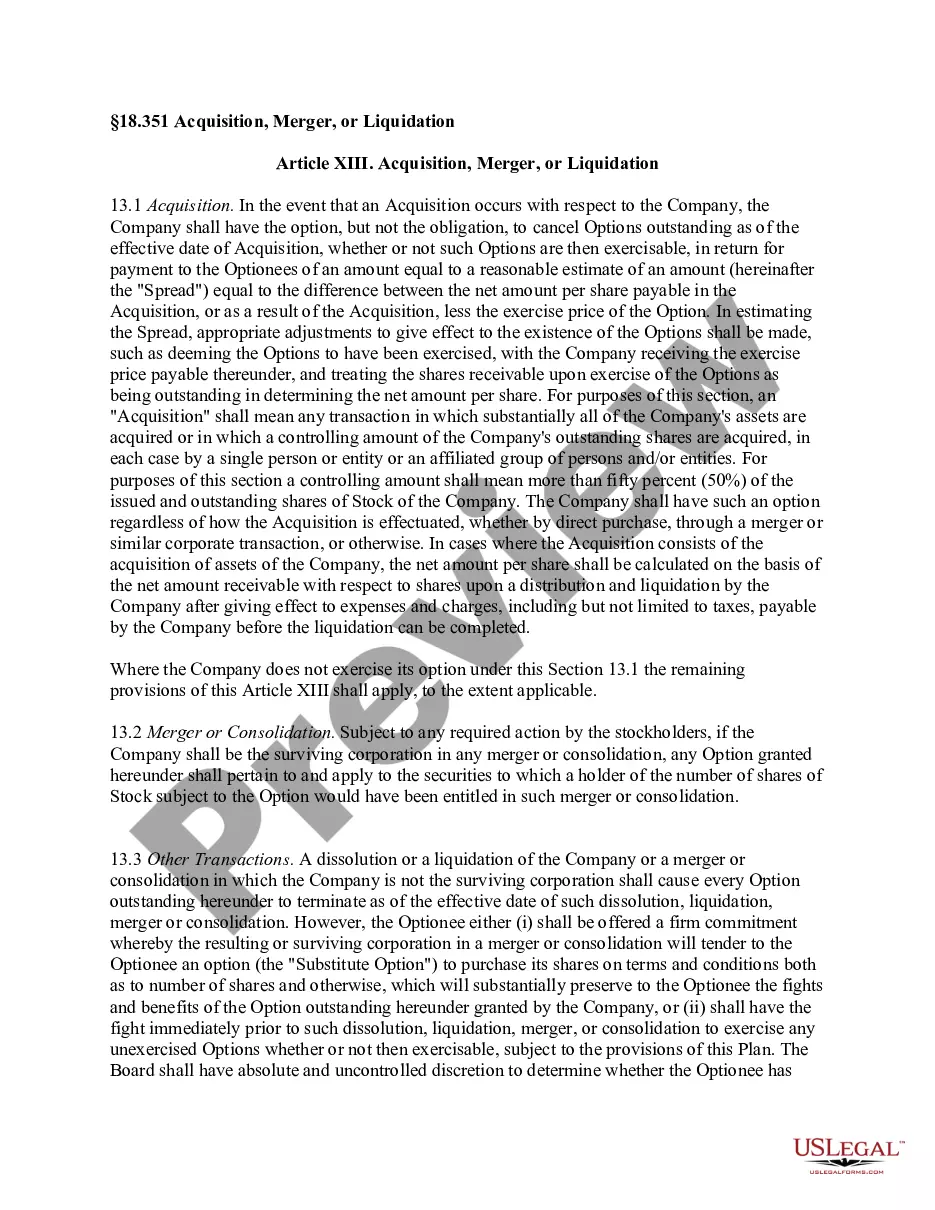

Kansas Acquisition, Merger, or Liquidation: Exploring Business Restructuring Strategies In the world of business, acquisitions, mergers, and liquidations play crucial roles in shaping the corporate landscape. When it comes to Kansas, these terms hold particular significance, with diverse types of such business restructuring strategies taking place within the state. This article aims to provide a detailed description of what Kansas Acquisition, Merger, or Liquidation entail, while also highlighting some of their distinct variations. Acquisition refers to the process through which one company purchases another, thereby gaining control over its assets, liabilities, and operations. In Kansas, acquisitions can occur between companies of different sizes, in various sectors, and have different intentions. Here are a few notable types of acquisitions in Kansas: 1. Horizontal Acquisition: This type of acquisition takes place when two companies operating in the same industry merge or one acquires the other. For example, a prominent Kansas-based manufacturing company may acquire another manufacturing firm operating in a similar field to expand its market reach or eliminate competition. 2. Vertical Acquisition: In this case, the acquiring company targets businesses operating in the supply chain of its primary operations. For instance, a Kansas-based agricultural equipment manufacturer might acquire a raw material supplier or a distributor to have better control over its supply chain and reduce costs. Mergers, on the other hand, represent a form of business restructuring strategy where two companies unite to form a single entity, sharing resources, operations, and decision-making. Various types of mergers exist, including: 1. Horizontal Merger: Similar to a horizontal acquisition, a horizontal merger occurs when two companies in the same industry merge to form a stronger, more competitive entity in the market. Kansas may witness such mergers within sectors like technology or retail, as businesses strive to consolidate their market positions. 2. Conglomerate Merger: In this merger type, companies from unrelated industries join forces to diversify their operations and expand their market presence. For instance, a Kansas-based energy company might merge with a pharmaceutical company to diversify its revenue streams and reduce market risks. Liquidation, meanwhile, refers to the winding up of a company's affairs and distribution of its assets to stakeholders or creditors. While liquidation typically marks the end of a company's operations, Kansas may witness different types of liquidation, including: 1. Voluntary Liquidation: This occurs when a company decides to shut down its operations and distributes its assets voluntarily. It may happen due to financial difficulties or strategic decisions. In Kansas, small businesses or startups that fail to sustain their operations may opt for voluntary liquidation. 2. Involuntary Liquidation: In cases of insolvency or unresolved financial issues, creditors or regulatory authorities can force a company into liquidation. These situations often arise when a company fails to meet its financial obligations or regulatory requirements. In conclusion, Kansas Acquisition, Merger, or Liquidation refers to the varied business restructuring strategies prevalent within the state. Acquisitions involve one company gaining control over another, while mergers unite two entities to form a stronger corporation. Liquidation signifies the dissolution of a company's operations. Understanding these terms and their variations can provide valuable insights into the ever-evolving dynamics of Kansas' corporate landscape.

Kansas Acquisition, Merger, or Liquidation

Description

How to fill out Kansas Acquisition, Merger, Or Liquidation?

Discovering the right legitimate record template could be a battle. Obviously, there are a variety of layouts available on the Internet, but how do you obtain the legitimate kind you require? Take advantage of the US Legal Forms web site. The assistance delivers thousands of layouts, like the Kansas Acquisition, Merger, or Liquidation, that you can use for enterprise and personal requires. Each of the kinds are checked out by specialists and meet up with federal and state demands.

When you are already authorized, log in to the account and then click the Down load switch to get the Kansas Acquisition, Merger, or Liquidation. Make use of your account to search throughout the legitimate kinds you possess ordered previously. Go to the My Forms tab of your own account and acquire one more duplicate in the record you require.

When you are a brand new end user of US Legal Forms, listed here are simple recommendations for you to comply with:

- Initially, be sure you have chosen the appropriate kind to your metropolis/area. You can look over the form while using Review switch and read the form description to guarantee it is the right one for you.

- In the event the kind will not meet up with your needs, utilize the Seach area to find the correct kind.

- When you are sure that the form is suitable, click the Buy now switch to get the kind.

- Choose the costs strategy you want and type in the needed information and facts. Design your account and purchase the transaction using your PayPal account or bank card.

- Select the data file file format and obtain the legitimate record template to the system.

- Comprehensive, revise and printing and indicator the acquired Kansas Acquisition, Merger, or Liquidation.

US Legal Forms may be the biggest local library of legitimate kinds in which you can find various record layouts. Take advantage of the company to obtain appropriately-created files that comply with express demands.

Form popularity

FAQ

Type C reorganization: A stock-for-asset deal, where the target company ?sells? all of its targets to the parent company in exchange for voting stock. Included in this transaction is a necessary amount of consideration that is not equity. This is known as a boot. The target company then liquidates (IRC § 368(a)(1)(C)).

and acquisitive Dreorganizations are both ?asset? reorgani zations and are both acquisitive in nature. Thus, the tax analysis of both of these types of reorganizations is very similar. A difference, however, is that reorgani zations have the solely for voting stock requirement and Dreorganizations do not.

Also, to qualify as a section 368(a) reorganization, a transaction generally must satisfy three nonstatutory requirements: business purpose, continuity of interest, and continuity of business enterprise.

Overview. In a D reorganization, one corporation transfers all or part of its assets to another corporation. Immediately after the transfer, the transferring corporation or one or more of its shareholders must be in control of the corporation that acquired the assets.

Using the method of ?upstream C with a drop? you can move assets within related entities without being taxed on it. The parent company acquires the subsidiary's assets through a reorganization of the subsidiary's assets under 26 U.S. Code § 368(a)(1)(C).

Overview. Practically speaking, a Type C reorganization is an asset-for-stock acquisition that is remarkably similar in result to an A reorganization. In an A reorganization, assets and liabilities of the target corporation are transferred to the acquiring corporation automatically by operation of statute.

Section 368(c) defines ?control? to mean the ownership of stock possessing at least 80 percent of the total combined voting power of all classes of stock entitled to vote and at least 80 percent of the total number of shares of all other classes of stock of the corporation.

An upstream C with a drop involves a parent corporation acquiring a subsidiary's assets, followed by reincorporation of some of those subsidiary's assets.