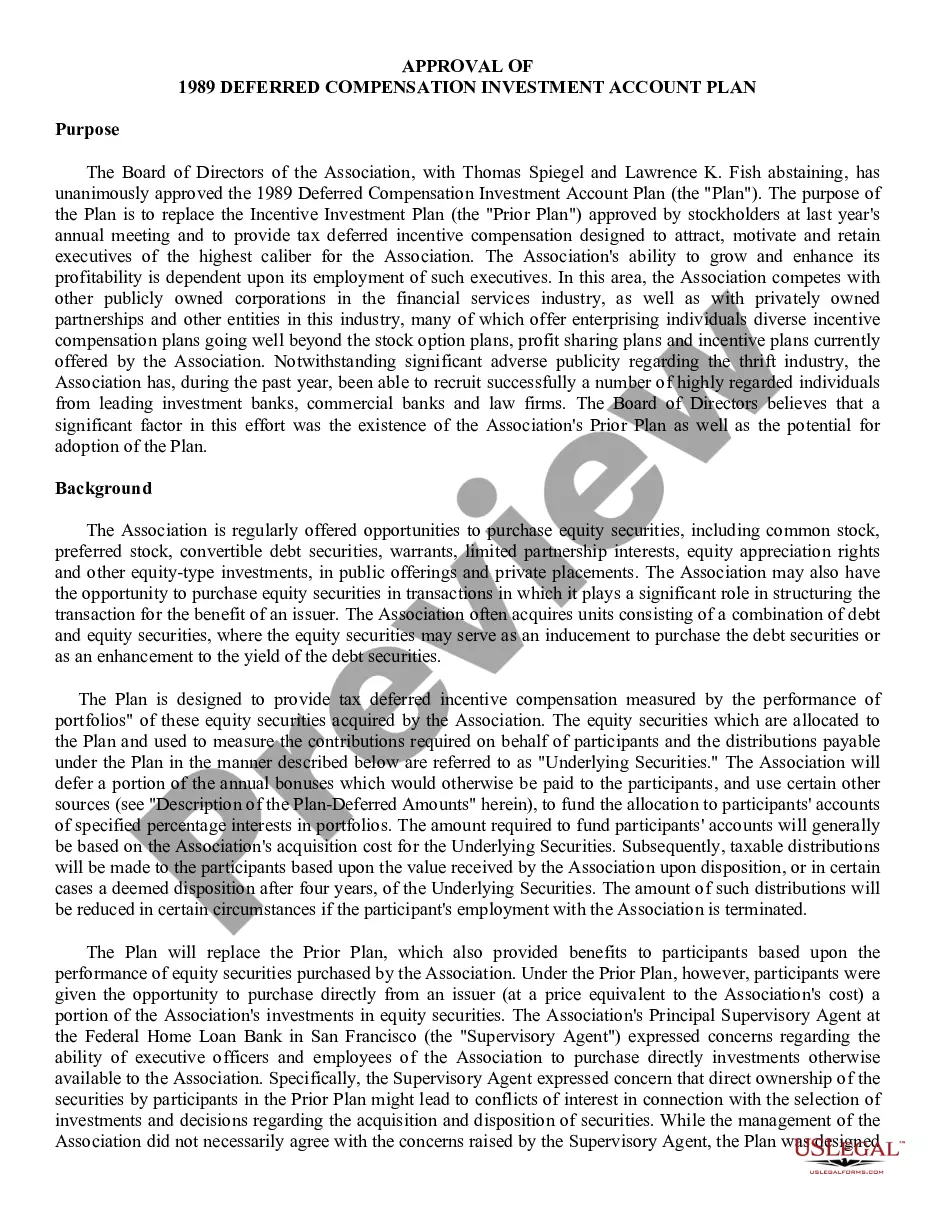

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Kansas Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

US Legal Forms - one of many largest libraries of lawful varieties in America - provides a wide array of lawful papers templates it is possible to obtain or print. While using web site, you can find a huge number of varieties for organization and individual functions, sorted by types, says, or keywords and phrases.You will find the most recent versions of varieties just like the Kansas Deferred Compensation Investment Account Plan in seconds.

If you have a monthly subscription, log in and obtain Kansas Deferred Compensation Investment Account Plan from the US Legal Forms catalogue. The Acquire button can look on every single develop you look at. You gain access to all formerly acquired varieties inside the My Forms tab of your own profile.

If you would like use US Legal Forms for the first time, listed below are easy guidelines to get you started out:

- Make sure you have picked the best develop for your personal metropolis/county. Click the Review button to examine the form`s content. Look at the develop description to ensure that you have chosen the appropriate develop.

- If the develop doesn`t match your needs, take advantage of the Lookup industry near the top of the monitor to get the one which does.

- In case you are satisfied with the form, validate your decision by simply clicking the Purchase now button. Then, select the prices program you want and offer your qualifications to register to have an profile.

- Approach the transaction. Utilize your charge card or PayPal profile to accomplish the transaction.

- Find the formatting and obtain the form on the gadget.

- Make changes. Load, modify and print and indicator the acquired Kansas Deferred Compensation Investment Account Plan.

Every single web template you added to your account does not have an expiration particular date and it is your own property forever. So, in order to obtain or print yet another backup, just proceed to the My Forms portion and then click in the develop you need.

Get access to the Kansas Deferred Compensation Investment Account Plan with US Legal Forms, by far the most substantial catalogue of lawful papers templates. Use a huge number of expert and state-specific templates that satisfy your business or individual needs and needs.

Form popularity

FAQ

Deferred compensation plans are funded informally. There's essentially a promise from the employer to pay the deferred funds, plus any investment earnings, to the employee at the time specified. In contrast, with a 401(k), a formally established account exists.

While similar, the main difference between 401(a) and 403(b) plans is often eligibility and plan design. 401(a) plans allow employers to require enrollment for eligible workers and set contribution models?but employers must also contribute to these plans. 403(b) plans, on the other hand, make enrollment voluntary.

A 401k plan has certain limitations on the amount that an individual can contribute each year. A deferred compensation plan, on the other hand, has no maximum contribution limit in any given year.

Deferred compensation plans are funded informally. There's essentially a promise from the employer to pay the deferred funds, plus any investment earnings, to the employee at the time specified. In contrast, with a 401(k), a formally established account exists.

Deferring income to retirement might help avoid high state income taxes (ex: California, New York, etc) if you're planning to move to a low-tax state. The biggest risk of deferred compensation plans is they're not guaranteed; if your company goes bankrupt, you might receive none of the income you deferred.

With a 401(k), an employee sets a percentage of their income to be automatically taken out of each paycheck and invested in their account. Participants can choose how to allocate their funds among the investment choices offered by the plan, which usually include a variety of mutual funds.

Investing your deferred compensation Your plan might offer you several options for the benchmark?often, major stock and bond indexes, the 10-year US Treasury note, the company's stock price, or the mutual fund choices in the company 401(k) plan.

ADP or Actual Deferral Percentage is an annual test in a 401(k) plan that compares the average salary deferrals of highly compensated employees to that of nonhighly compensated employees. Each employee's deferral percentage is the percentage of compensation that has been deferred to the 401(k) plan.