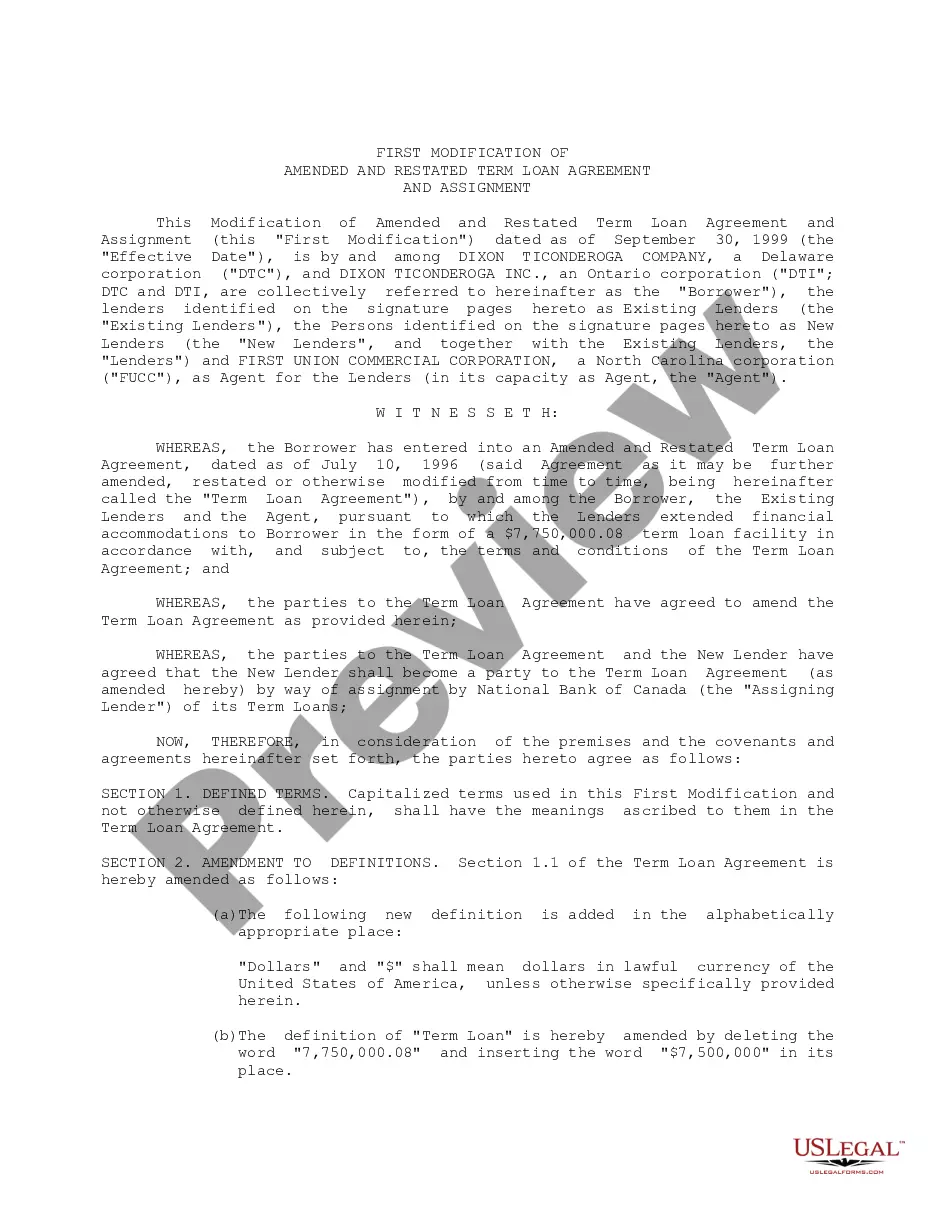

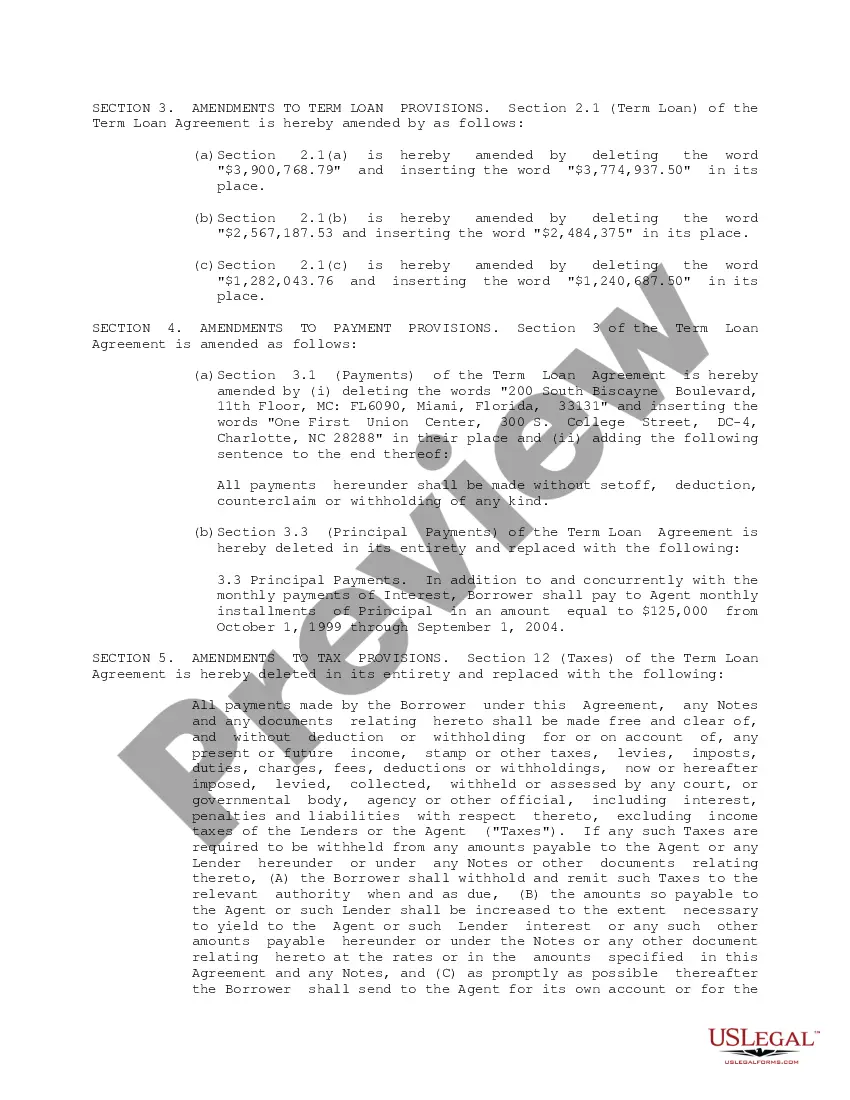

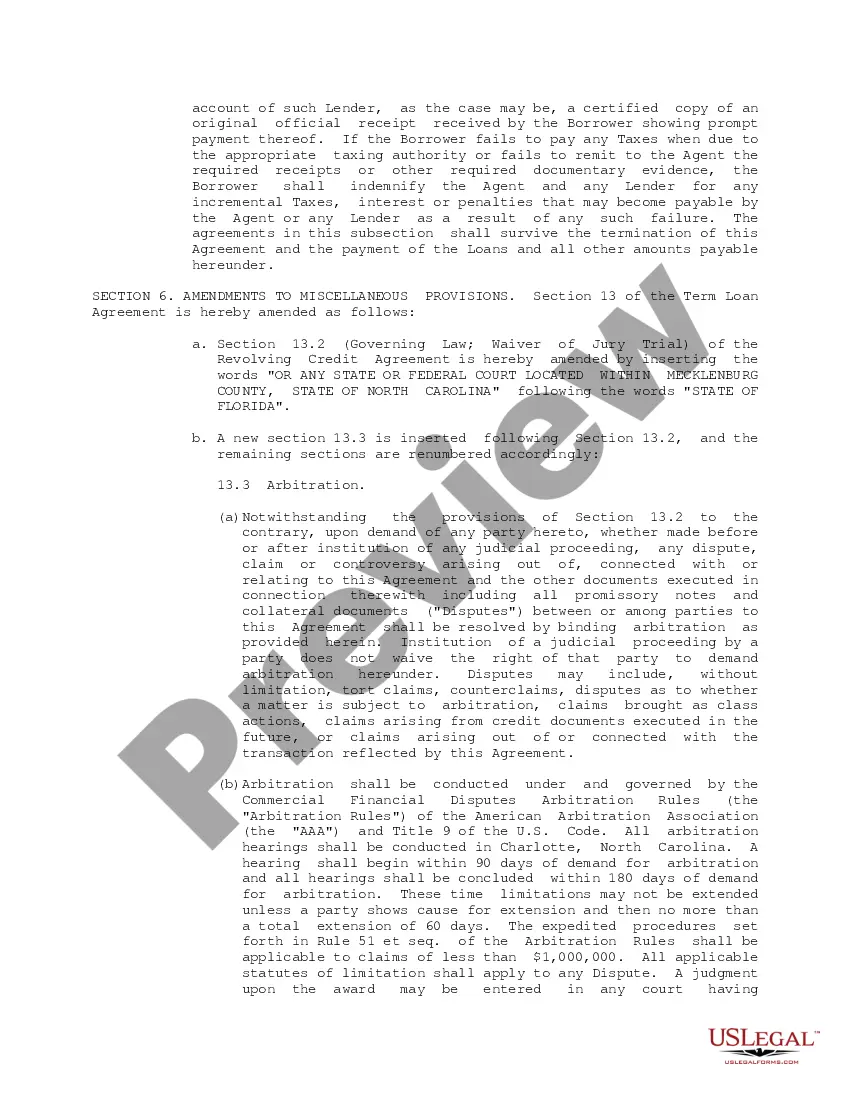

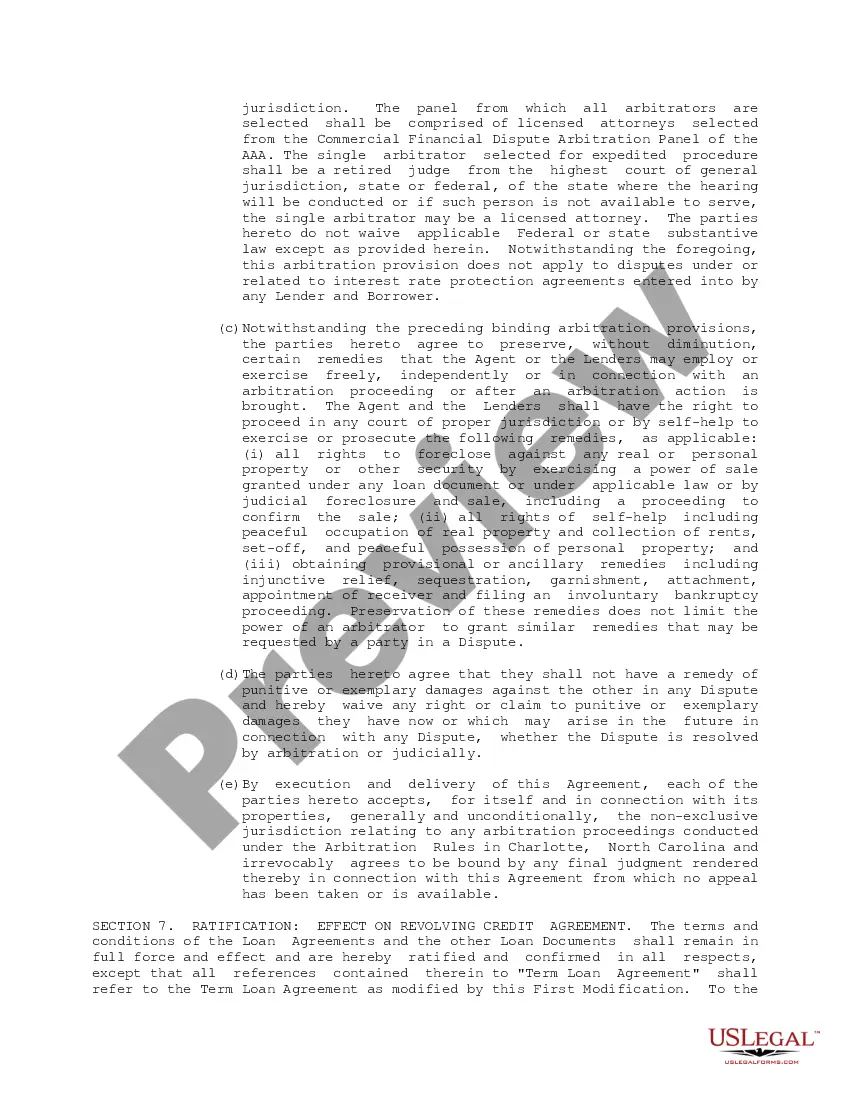

A Kansas Term Loan Agreement refers to a legal contract established between a lender and a borrower in the state of Kansas, governing the terms and conditions of a term loan. This type of loan is typically used by businesses to fund specific projects, equipment purchases, or operational expenses. The Kansas Term Loan Agreement outlines the specifics of the loan, including the principal amount, interest rate, repayment terms, and any collateral or guarantees provided by the borrower. It also includes provisions related to the rights and responsibilities of both parties, default and remedies, as well as any fees or charges associated with the loan. There are various types of Kansas Term Loan Agreements available, tailored to meet different business needs and circumstances. These include: 1. Fixed-Term Loan Agreement: This type of term loan agreement specifies a fixed term, during which the borrower must make regular repayments, typically on a monthly basis, until the loan is fully repaid. The interest rate is usually fixed for the entire loan duration. 2. Revolving Term Loan Agreement: In this type of agreement, the lender provides a revolving line of credit to the borrower up to a predetermined limit. The borrower can borrow, repay, and re-borrow funds throughout the term of the agreement, providing flexibility for short-term financing requirements. Interest is charged only on the outstanding balance. 3. Secured Term Loan Agreement: This agreement involves the borrower providing collateral, such as property or equipment, to secure the loan. If the borrower defaults on the loan, the lender has the right to seize and sell the asset to recover the outstanding balance. 4. Unsecured Term Loan Agreement: Unlike a secured loan agreement, an unsecured term loan does not require collateral. This type of loan agreement typically involves higher interest rates due to the increased risk to the lender. 5. Bridge Term Loan Agreement: Bridge loans are short-term loans that "bridge the gap" between the immediate need for financing and securing a long-term loan or other permanent financing solution. They are often used in real estate transactions or during periods of financial uncertainty. It is crucial for both lenders and borrowers to understand the terms and conditions outlined in the Kansas Term Loan Agreement before entering into the agreement. Consulting legal and financial professionals can provide guidance and ensure that the agreement complies with Kansas state laws and regulations.

Kansas Term Loan Agreement

Description

How to fill out Kansas Term Loan Agreement?

Discovering the right legitimate record design could be a have a problem. Naturally, there are a variety of themes available online, but how do you discover the legitimate kind you need? Take advantage of the US Legal Forms web site. The assistance gives a large number of themes, for example the Kansas Term Loan Agreement, which can be used for company and personal needs. Each of the kinds are examined by specialists and satisfy state and federal needs.

If you are presently authorized, log in to the bank account and click the Download option to obtain the Kansas Term Loan Agreement. Make use of bank account to appear throughout the legitimate kinds you may have purchased in the past. Check out the My Forms tab of your respective bank account and get one more backup of your record you need.

If you are a brand new end user of US Legal Forms, listed below are simple guidelines that you can stick to:

- Initially, be sure you have chosen the appropriate kind for the town/region. You may look over the form while using Preview option and browse the form outline to make sure it is the best for you.

- If the kind will not satisfy your preferences, make use of the Seach area to obtain the appropriate kind.

- When you are sure that the form would work, click the Acquire now option to obtain the kind.

- Choose the prices prepare you desire and enter in the necessary information and facts. Create your bank account and purchase an order utilizing your PayPal bank account or bank card.

- Select the data file file format and down load the legitimate record design to the system.

- Comprehensive, change and print out and indicator the attained Kansas Term Loan Agreement.

US Legal Forms will be the largest collection of legitimate kinds where you can find different record themes. Take advantage of the service to down load skillfully-manufactured documents that stick to status needs.