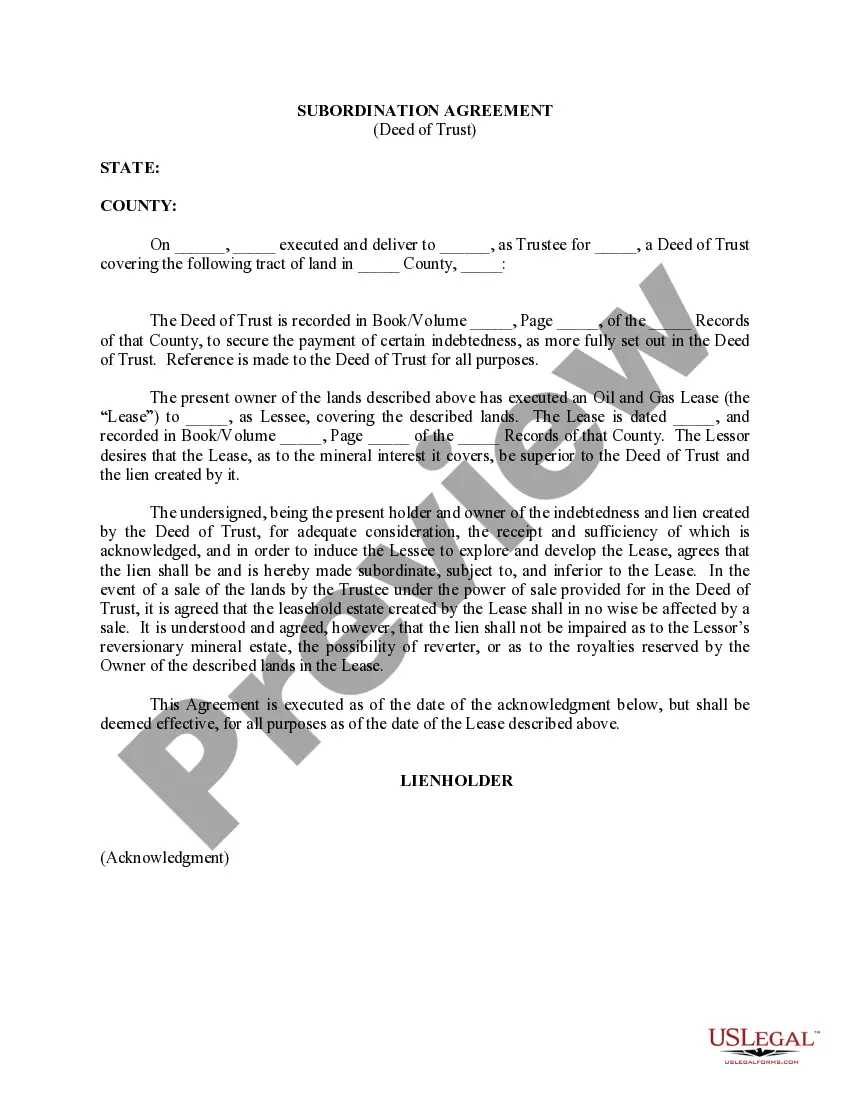

A Kansas Subordination Agreement, also known as a Deed of Trust, is a legally-binding document that establishes the priority of different liens or claims on a property. It outlines the order in which creditors will be repaid in the event of foreclosure or the sale of the property. In Kansas, there are various types of Subordination Agreements that can be utilized depending on the circumstances. These include: 1. First lien subordination agreement: This type of agreement is commonly used when a property owner wants to refinance their first mortgage while maintaining the existing second mortgage. It involves the first lien holder agreeing to subordinate their lien to the new first mortgage. 2. Second lien subordination agreement: In situations where a property owner has an existing first mortgage and wants to take out a second mortgage, a second lien subordination agreement is employed. It allows the second lien holder to gain a position of priority over any subsequent liens. 3. Subordination agreement for construction loans: When a property owner applies for a construction loan to fund building or renovating a property, a subordination agreement is often required. This agreement ensures that the construction lender's lien takes priority over any other liens, allowing them to be repaid first in case of default or foreclosure. 4. Subordination agreement for junior liens: Junior liens, such as home equity loans or lines of credit, may require a subordination agreement if the property owner wishes to refinance the first mortgage. This agreement grants the new lender priority over the junior liens, ensuring proper repayment order. Kansas Subordination Agreements play a crucial role in the mortgage and lending industry. They provide clarity and establish the rights and priorities of various lien holders in case of default or sale of the property. It ensures a fair and predictable repayment structure, protecting the interests of all parties involved. When entering into a Kansas Subordination Agreement, it is essential to consult with legal professionals or title companies to ensure compliance with state laws and regulations. A carefully drafted and executed agreement can provide security and eliminate confusion in the event of financial distress or property transactions.

Kansas Subordination Agreement (Deed of Trust)

Description

How to fill out Kansas Subordination Agreement (Deed Of Trust)?

You may invest hrs on-line looking for the authorized record web template that suits the federal and state needs you require. US Legal Forms supplies thousands of authorized varieties which can be examined by experts. You can easily obtain or printing the Kansas Subordination Agreement (Deed of Trust) from your assistance.

If you currently have a US Legal Forms accounts, you can log in and then click the Acquire key. After that, you can total, edit, printing, or signal the Kansas Subordination Agreement (Deed of Trust). Every authorized record web template you acquire is the one you have permanently. To have one more version for any purchased develop, check out the My Forms tab and then click the corresponding key.

If you work with the US Legal Forms site the very first time, keep to the simple guidelines listed below:

- Initially, make certain you have chosen the correct record web template for that area/town of your choice. See the develop outline to make sure you have chosen the correct develop. If accessible, use the Preview key to check from the record web template also.

- If you wish to discover one more edition of your develop, use the Look for discipline to obtain the web template that meets your needs and needs.

- After you have located the web template you would like, just click Purchase now to move forward.

- Find the pricing plan you would like, type in your qualifications, and sign up for a free account on US Legal Forms.

- Total the purchase. You can use your charge card or PayPal accounts to purchase the authorized develop.

- Find the format of your record and obtain it to your system.

- Make alterations to your record if required. You may total, edit and signal and printing Kansas Subordination Agreement (Deed of Trust).

Acquire and printing thousands of record themes utilizing the US Legal Forms website, which provides the largest collection of authorized varieties. Use expert and express-particular themes to tackle your organization or individual demands.