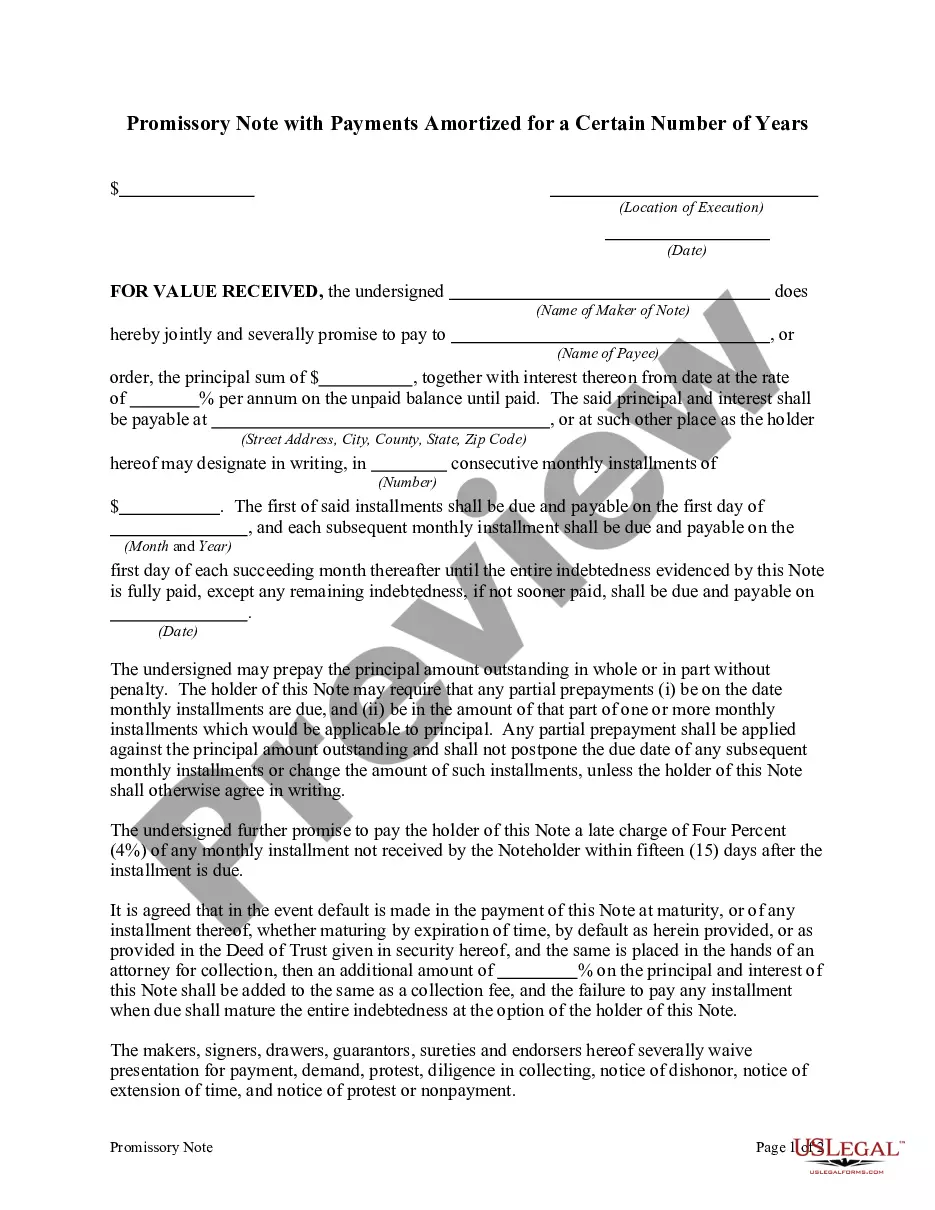

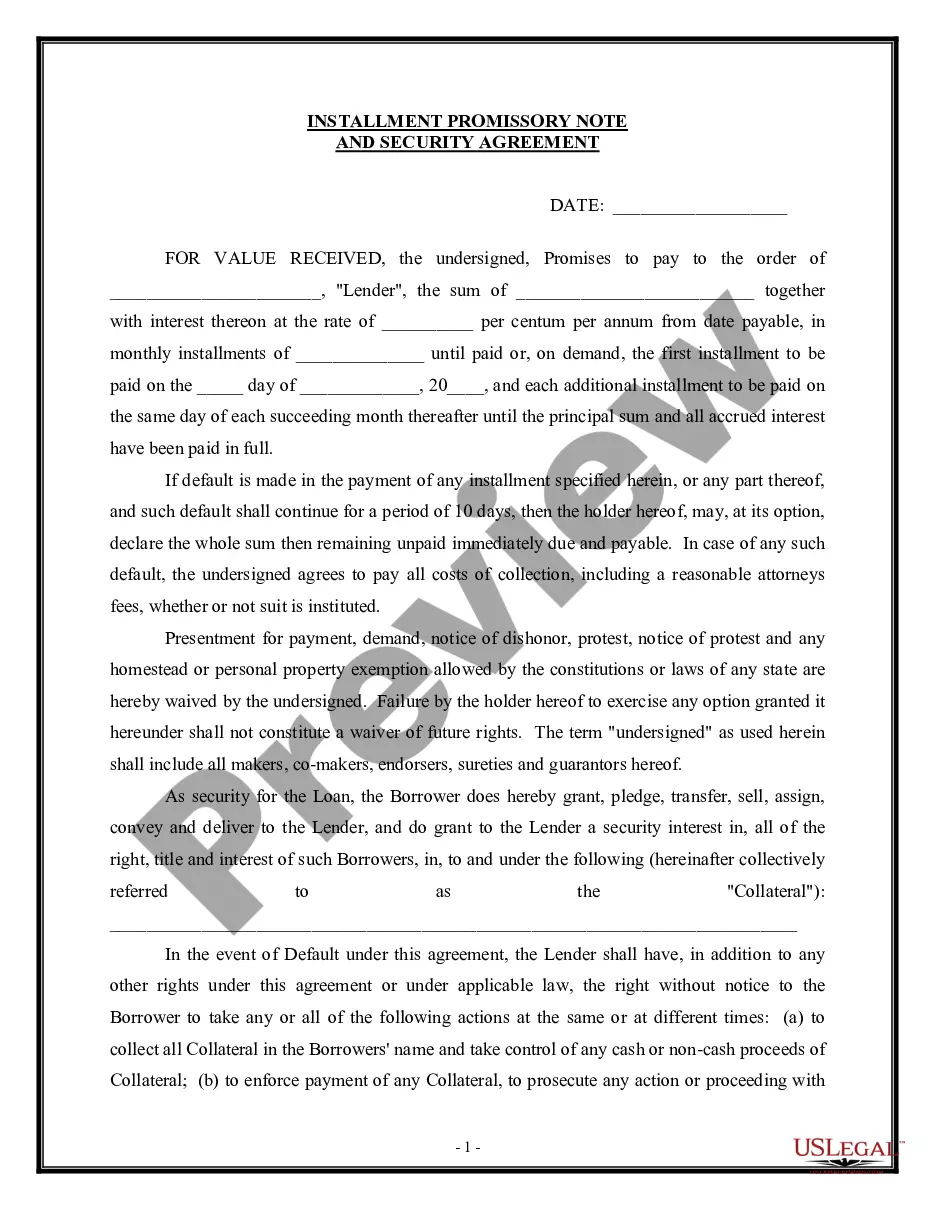

This form is a Promissory Note. The form provides that the borrower promises to pay the lender in monthly installments. The agreement also provides that there will not be a pre-payment penalty on the note.

Kentucky Promissory Note with Installment Payments

Category:

State:

Multi-State

Control #:

US-00598

Format:

Word;

Rich Text

Instant download

Description

How to fill out Promissory Note With Installment Payments?

Are you presently within a situation where you require documentation for periodic professional or personal purposes each day.

There are numerous legitimate form templates accessible online, but finding reliable versions can be challenging.

US Legal Forms provides a wide array of template forms, such as the Kentucky Promissory Note with Installment Payments, which can be tailored to comply with state and federal regulations.

Once you find the suitable form, simply click Buy now.

Choose the pricing structure you prefer, complete the necessary information to create your account, and place an order using your PayPal or credit card.

- If you are already acquainted with the US Legal Forms site and possess an account, simply Log In.

- Then, you can obtain the Kentucky Promissory Note with Installment Payments template.

- If you do not have an account and wish to begin utilizing US Legal Forms, follow these steps.

- Select the form you require and ensure it corresponds to your specific city/state.

- Utilize the Preview option to review the form.

- Check the details to confirm that you have chosen the correct form.

- If the form does not meet your expectations, use the Research field to find the form that suits your needs and requirements.

Form popularity

FAQ

To obtain your promissory note, make sure you have a signed copy from all involved parties, as this serves as proof of the agreement. If you need assistance drafting or retrieving this document, services like uslegalforms can provide guidance and templates tailored for a Kentucky Promissory Note with Installment Payments, making the process seamless.

When making a promissory note for a balance payment, include the total amount owed, the date of payment, and any interest if applicable. Clearly state how the payment will be delivered and any consequences for late payment. Utilizing a Kentucky Promissory Note with Installment Payments template can help you maintain clarity and legality in your agreement.

There are several types of promissory notes, each designed to fit specific financial situations. For instance, a Kentucky Promissory Note with Installment Payments is specifically tailored for loans repaid in regular installments over time. Other types include demand promissory notes, which require repayment upon request, and secured promissory notes, backed by collateral. Understanding these variations helps you choose the right option for your needs.

To ensure that a Kentucky Promissory Note with Installment Payments is valid, it must include specific elements. First, it needs clear identification of the parties involved, which means naming both the borrower and the lender. Additionally, the note must state the amount borrowed, the repayment terms, and the interest rate, if applicable. Finally, both parties should sign the document to confirm their agreement on these terms.

To write a promissory note for payment, start by clearly stating the date, the names of both parties, and the amount in question. Next, outline the payment terms, especially when dealing with Kentucky Promissory Note with Installment Payments. This should include the due dates for each installment, interest rate if applicable, and any late fees.

Prepayment. Maker may prepay all or any part of the principal balance of this Promissory Note at any time without premium or penalty. Amounts prepaid may not be reborrowed. 5.

A banknote is frequently referred to as a promissory note, as it is made by a bank and payable to bearer on demand. Mortgage notes are another prominent example. If the promissory note is unconditional and readily saleable, it is called a negotiable instrument.

Types of Promissory NotesPersonal Promissory Notes This is a particular loan taken from family or friends.Commercial Here, the note is made when dealing with commercial lenders such as banks.Real Estate This is similar to commercial notes in terms of nonpayment consequences.More items...

An installment note is a form of promissory note calling for payment of both principal and interest in specified amounts, or specified minimum amounts, at specific time intervals.