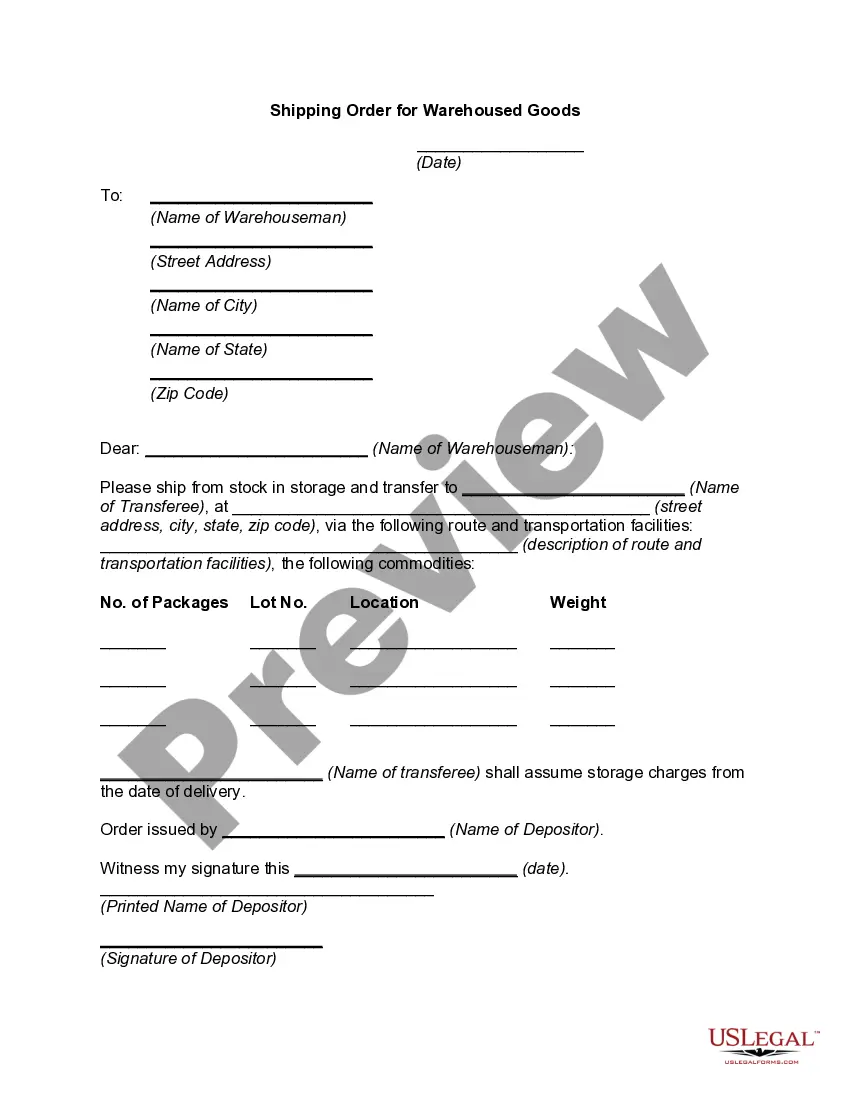

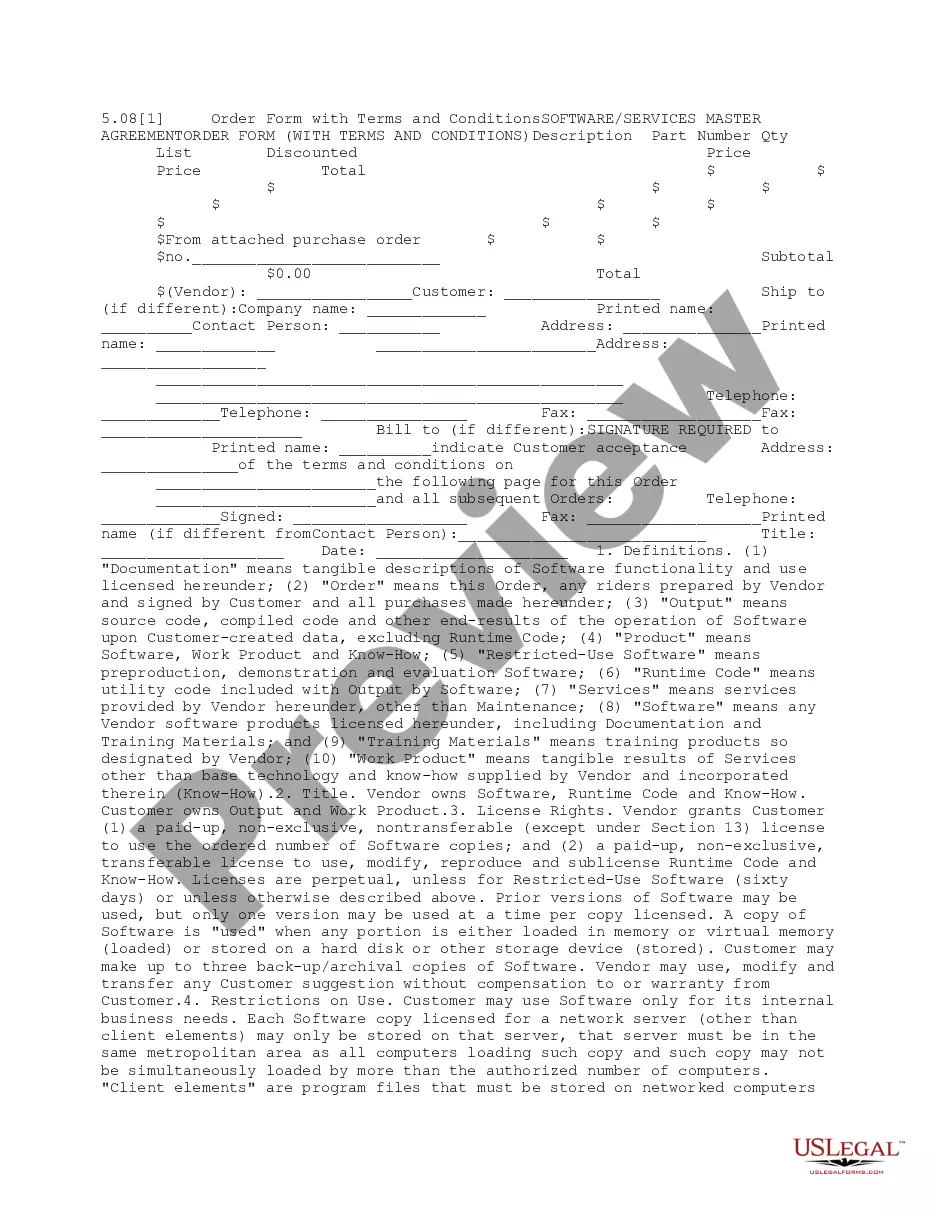

Kentucky Shipping and Order Form for Software Purchase

Description

How to fill out Shipping And Order Form For Software Purchase?

US Legal Forms - one of the largest collections of legal documents in the United States - provides an extensive range of legal document templates that you can download or print.

By using the website, you can find thousands of forms for business and personal needs, organized by type, state, or keywords.

You can access the latest versions of forms such as the Kentucky Shipping and Order Form for Software Purchase in moments.

Check the form information to ensure you've chosen the appropriate document.

If the form doesn't meet your requirements, utilize the Lookup field at the top of the screen to find the one that does.

- If you already have a monthly subscription, Log In and download the Kentucky Shipping and Order Form for Software Purchase from the US Legal Forms collection.

- The Download button will be visible on each form you view.

- You can access all previously downloaded forms in the My documents tab of your account.

- If you are using US Legal Forms for the first time, here are simple instructions to help you get started.

- Ensure you have selected the correct form for your city/region.

- Click on the Preview button to examine the form’s content.

Form popularity

FAQ

Sales tax on shipping charges in KentuckyKentucky does apply sales tax to shipping costs. The rule of thumb is that if what you're selling is subject to tax, then the shipping charges are also subject to tax.

Only two states Tennessee and Vermont have specific statutes in place to address SaaS transactions and sales tax.

Cloud-Based SoftwareThe sale or lease of prewritten software and software license fees are subject to Kentucky sales and use tax as the sale of tangible personal property as prescribed in KRS 139.200 and KRS 139.010(29) and (41).

However, shipping charges are generally taxable if the actual seller of the product makes the delivery. In addition, handling charges are always taxable. When a seller invoices the customer for a single charge for shipping and handling, then this combined charge is taxable regardless of who makes the delivery.

SaaS is not identified as a taxable service within these guidelines. Based on this information, SaaS is likely not taxable. However, if you sell Software-as-a-Service in Colorado, you may need a Private Letter Ruling to clarify if your product is taxable in their state.

In general, delivery-related charges for taxable products are not taxable when you ship directly to the purchaser via common carrier, contract carrier, or USPS; delivery, shipping, freight, or postage charges are separately stated; and the charge isn't greater than the actual cost of delivery.

Kentucky SaaS is non-taxable because it isn't tangible personal property.

10A100(P) (06-21) Employer's Withholding Tax Account. Sales and Use Tax Account/Permit. Transient Room Tax Account. Motor Vehicle Tire Fee Account.

Certain goods are exempt from sales and use tax including coal and other energy-producing fuels, certain medical items, locomotives or rolling stock, certain farm machinery and livestock, certain seeds and farm chemicals, machinery for new and expanded industry, tombstones, textbooks, property certified as an alcohol

Goods that are subject to sales tax in Kentucky include physical property, like furniture, home appliances, and motor vehicles. Groceries, prescription medicine, and gasoline are all tax-exempt. Some services in Kentucky are subject to sales tax.