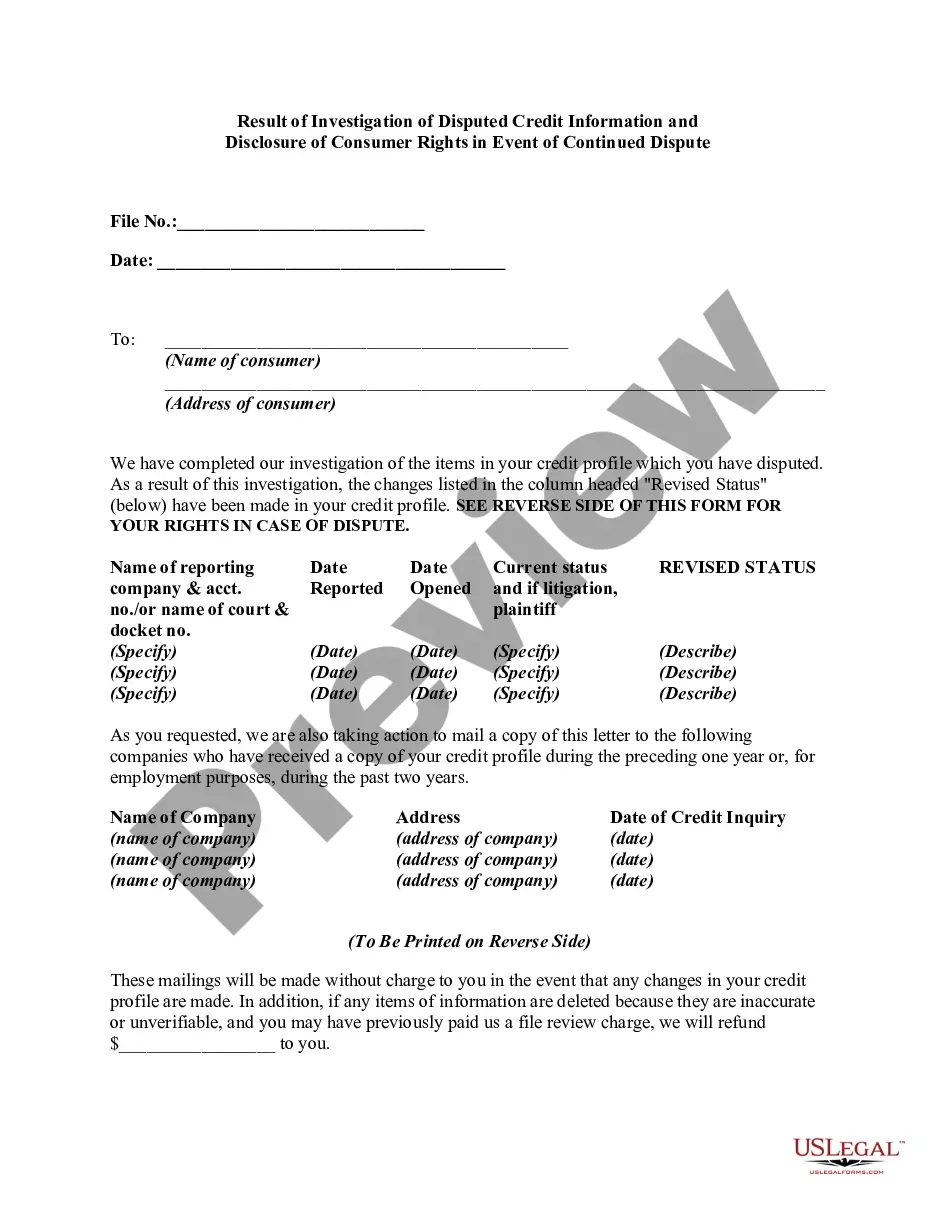

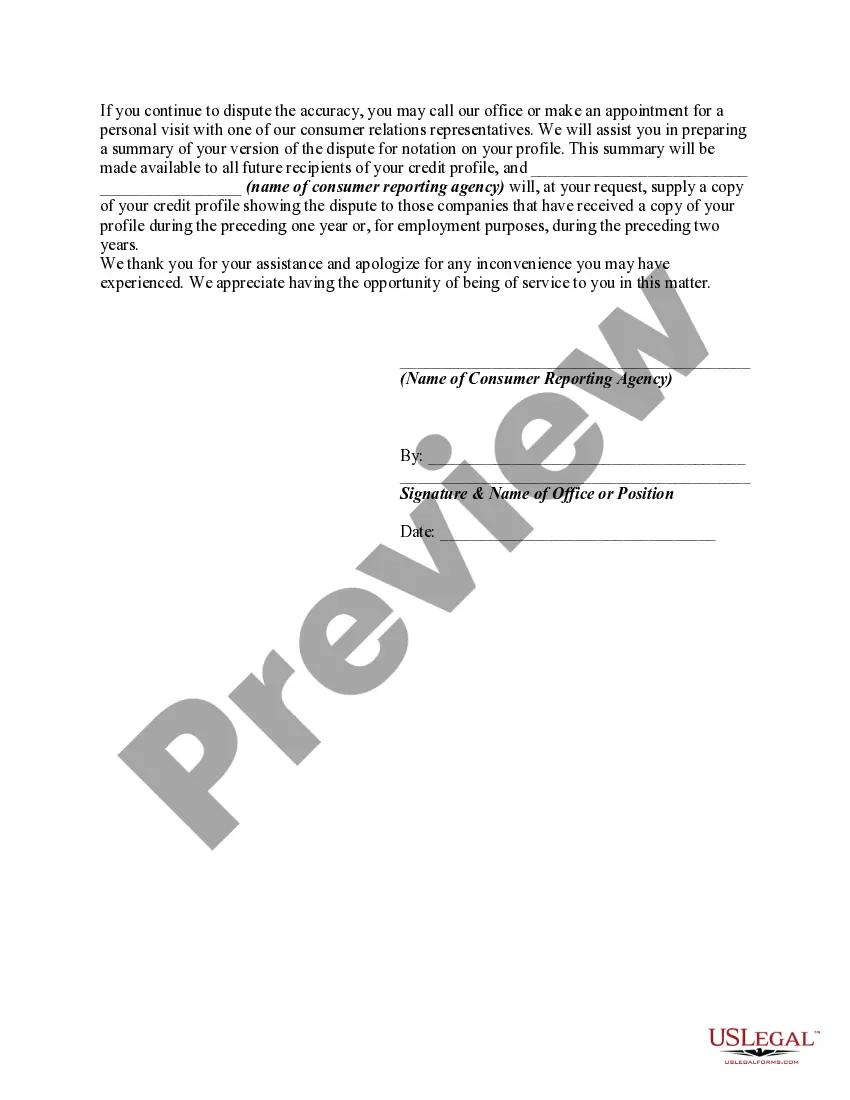

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Kentucky Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: A Comprehensive Overview Introduction: The state of Kentucky holds regulations and laws that protect consumers in cases of disputed credit information and provide them with clear disclosure of their rights throughout the investigation process. This article delves into the details of Kentucky's investigation results, credit information dispute resolution, and consumer rights disclosure, shedding light on the different types of documentation and procedures involved. Keywords: Kentucky, investigate, disputed credit information, consumer rights, disclosure, investigation results, dispute resolution, documentation, procedures. 1. Investigation Process in Kentucky: In Kentucky, when a consumer disputes inaccurate or incomplete credit information, it triggers an investigation conducted by credit reporting agencies (Crash) under the Fair Credit Reporting Act (FCRA). The investigation process assesses the validity and accuracy of the disputed credit information. 2. Dispute Resolution Outcomes: Upon completion of the investigation, Kentucky allows for multiple outcomes based on the investigation results, including but not limited to: a) Verified Information: If the result of the investigation establishes that the disputed credit information is accurate and verifiable, it will remain on the consumer's credit report. b) Inaccurate or Incomplete Information: In cases where the investigation concludes that the disputed credit information is inaccurate or incomplete, the Crash must amend or delete the erroneous data from the consumer's credit report. This correction may positively impact the individual's creditworthiness. c) Notification to Consumer: Kentucky requires the Crash to promptly notify the consumer of the investigation results in writing, which includes details about any modifications made to their credit report. 3. Disclosure of Consumer Rights: Kentucky mandates that consumers be informed of their rights during and after the dispute resolution process. They must receive full disclosure from Crash, creditors, and other relevant entities regarding their rights, such as: a) Right to Dispute: Consumers have the right to dispute inaccuracies or incompleteness on their credit report by submitting a written request to the appropriate Crash. b) Time Limit for Investigation: Kentucky stipulates a timeframe within which Crash must investigate and resolve the dispute, typically within 30 days of receiving the written dispute. c) Right to Free Credit Reports: Consumers have the right to request a free copy of their credit report annually from each of the three major Crash: Equifax, Experian, and TransUnion. d) Right to Appeals Process: If the consumer disagrees with the investigation results, they have the right to appeal the decision and provide additional supporting evidence. e) Legal Options: If the dispute remains unresolved or the credit reporting agencies fail to comply with the FCRA, consumers may pursue legal action to protect their rights and seek appropriate remedies. Conclusion: Kentucky's thorough investigation process for disputes related to credit information provides consumers with a fair chance to rectify inaccuracies or incompleteness in their credit reports. Through comprehensive disclosure of consumer rights, individuals can exercise their entitlement to challenge and rectify any negative impacts on their creditworthiness. Being well-informed about these processes and rights empowers consumers to take control of their financial well-being in Kentucky.Title: Kentucky Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: A Comprehensive Overview Introduction: The state of Kentucky holds regulations and laws that protect consumers in cases of disputed credit information and provide them with clear disclosure of their rights throughout the investigation process. This article delves into the details of Kentucky's investigation results, credit information dispute resolution, and consumer rights disclosure, shedding light on the different types of documentation and procedures involved. Keywords: Kentucky, investigate, disputed credit information, consumer rights, disclosure, investigation results, dispute resolution, documentation, procedures. 1. Investigation Process in Kentucky: In Kentucky, when a consumer disputes inaccurate or incomplete credit information, it triggers an investigation conducted by credit reporting agencies (Crash) under the Fair Credit Reporting Act (FCRA). The investigation process assesses the validity and accuracy of the disputed credit information. 2. Dispute Resolution Outcomes: Upon completion of the investigation, Kentucky allows for multiple outcomes based on the investigation results, including but not limited to: a) Verified Information: If the result of the investigation establishes that the disputed credit information is accurate and verifiable, it will remain on the consumer's credit report. b) Inaccurate or Incomplete Information: In cases where the investigation concludes that the disputed credit information is inaccurate or incomplete, the Crash must amend or delete the erroneous data from the consumer's credit report. This correction may positively impact the individual's creditworthiness. c) Notification to Consumer: Kentucky requires the Crash to promptly notify the consumer of the investigation results in writing, which includes details about any modifications made to their credit report. 3. Disclosure of Consumer Rights: Kentucky mandates that consumers be informed of their rights during and after the dispute resolution process. They must receive full disclosure from Crash, creditors, and other relevant entities regarding their rights, such as: a) Right to Dispute: Consumers have the right to dispute inaccuracies or incompleteness on their credit report by submitting a written request to the appropriate Crash. b) Time Limit for Investigation: Kentucky stipulates a timeframe within which Crash must investigate and resolve the dispute, typically within 30 days of receiving the written dispute. c) Right to Free Credit Reports: Consumers have the right to request a free copy of their credit report annually from each of the three major Crash: Equifax, Experian, and TransUnion. d) Right to Appeals Process: If the consumer disagrees with the investigation results, they have the right to appeal the decision and provide additional supporting evidence. e) Legal Options: If the dispute remains unresolved or the credit reporting agencies fail to comply with the FCRA, consumers may pursue legal action to protect their rights and seek appropriate remedies. Conclusion: Kentucky's thorough investigation process for disputes related to credit information provides consumers with a fair chance to rectify inaccuracies or incompleteness in their credit reports. Through comprehensive disclosure of consumer rights, individuals can exercise their entitlement to challenge and rectify any negative impacts on their creditworthiness. Being well-informed about these processes and rights empowers consumers to take control of their financial well-being in Kentucky.