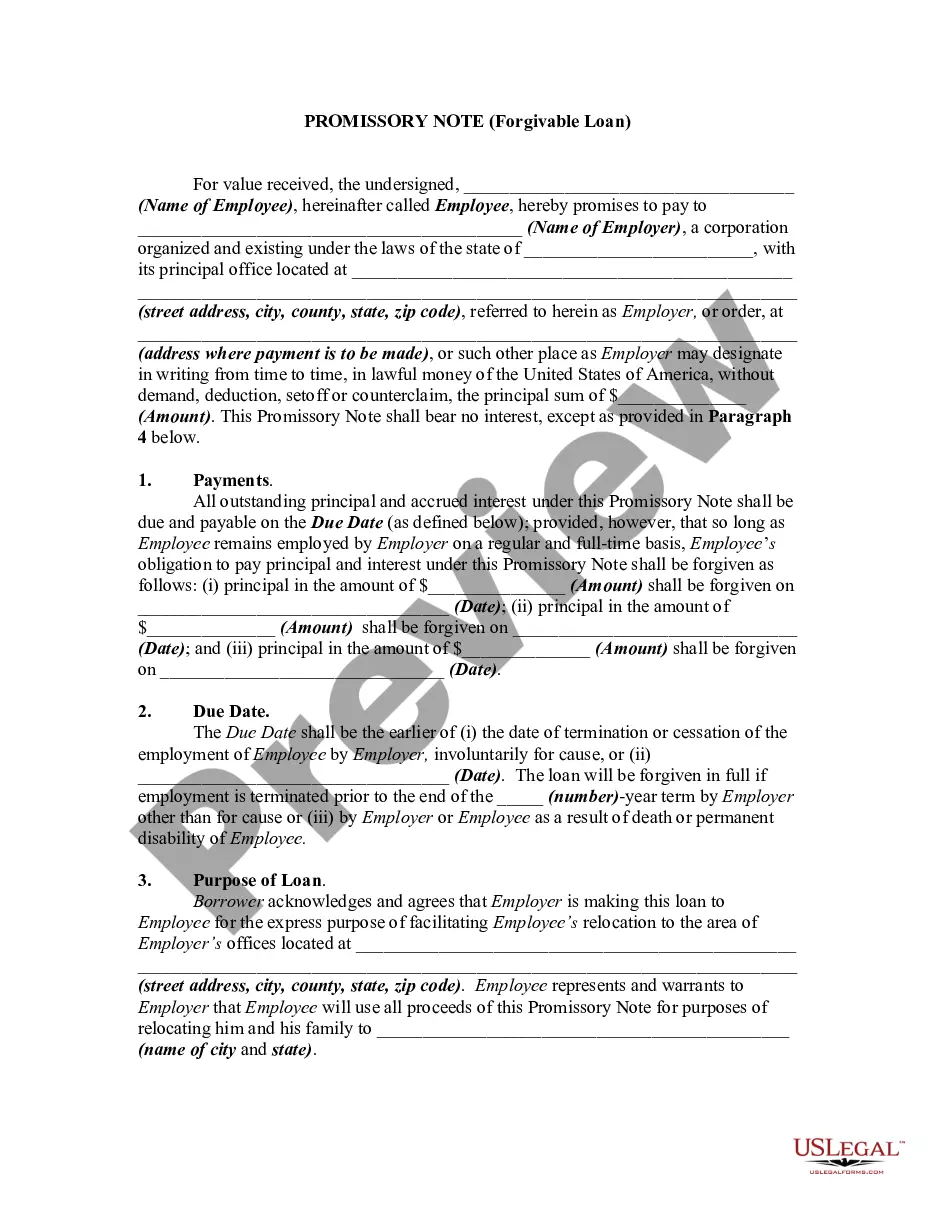

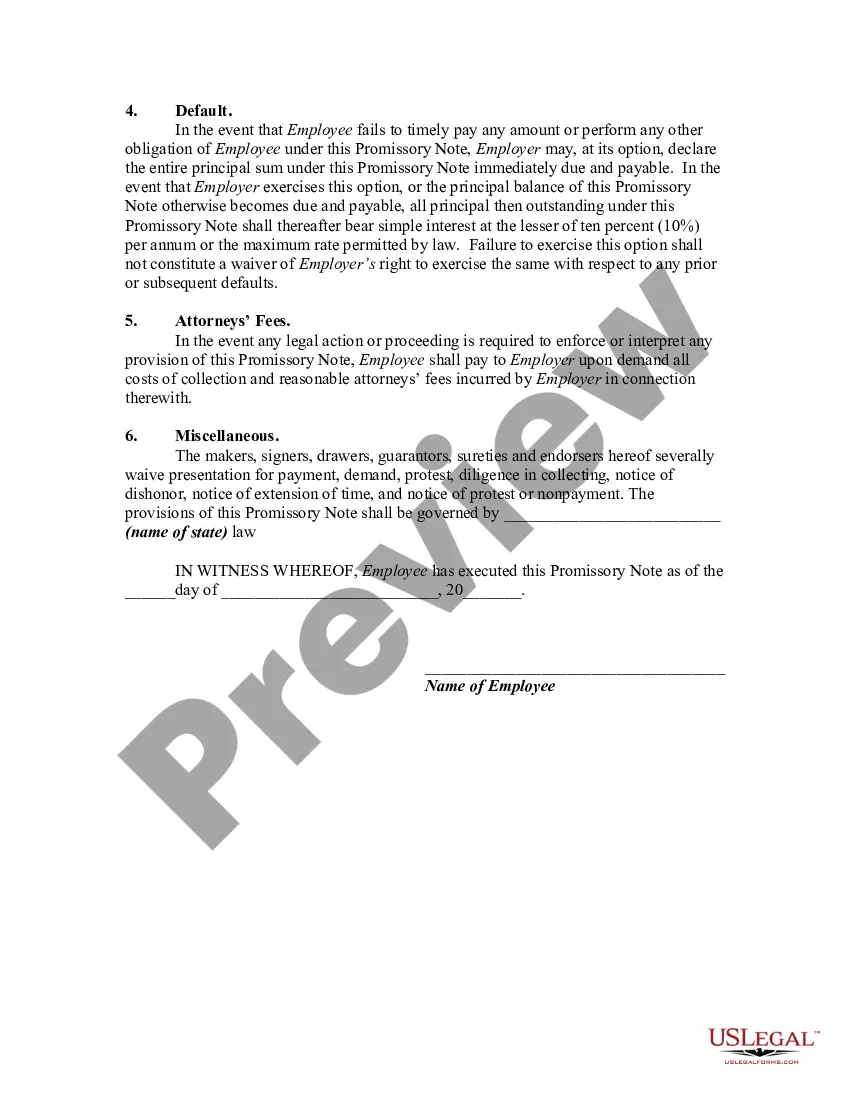

It is not uncommon for employers to make loans to their new executives. The purpose of such a loan may be to assist the executive in the purchase of a home or other relocation expenses. Frequently, the loan is forgivable over a period of time provided the executive remains employed. The loan also may be forgivable if the executive's employment terminates for specified reasons (e.g., death, disability or termination by the employer without cause).

A Kentucky Promissory Note — Forgivable Loan is a legally binding document that outlines the terms and conditions for a loan that may be forgiven under certain circumstances. It is a financial agreement between a lender and a borrower, typically used for financing educational programs, economic development initiatives, entrepreneurship support, or affordable housing projects. In Kentucky, there are several types of Promissory Note — Forgivable Loans offered by various organizations and government agencies. These loans aim to encourage economic growth and support individuals or businesses in need. The common types of Kentucky Promissory Note — Forgivable Loans include: 1. Kentucky Educational Excellence Scholarship (KEEP) Forgivable Loan: The KEEP program provides financial assistance to Kentucky residents who demonstrate academic achievements during high school. Upon entering an eligible Kentucky college or university, a portion of the KEEP award can be converted into a Promissory Note — Forgivable Loan, which can be forgiven if the student graduates with a specific GPA or completes certain qualifying degrees. 2. Kentucky Investment Fund for Nano-Manufacturing (IF): This forgivable loan program supports businesses involved in nano-manufacturing, providing financial assistance to cover eligible project costs such as land acquisition, construction, equipment, and workforce training. The loan can be forgiven if the business meets specific job creation and investment goals within a designated time frame. 3. Kentucky Affordable Housing Trust Fund (KATE) Forgivable Loan: The KATE offers forgivable loans to developers and nonprofit organizations involved in affordable housing projects across the state. The loans can be used to cover predevelopment costs, construction expenses, or preservation efforts. Forgiveness is granted if the project meets specific affordability requirements and remains in compliance with the program's guidelines for a determined period. 4. Kentucky Small Business Tax Credit (SBC) Forgivable Loan: This program is designed to assist small businesses with access to capital for growth and job creation. SBC offers forgivable loans as an incentive for new or existing businesses that create a certain number of qualified jobs within Kentucky. The loan can be forgiven if the business meets the job creation targets over a defined period. These examples showcase the range of Kentucky Promissory Note — Forgivable Loans available, each catering to different sectors and goals. It is essential to carefully review the terms and conditions of each program before entering into a promissory note agreement to fully understand the loan forgiveness conditions, repayment terms, interest rates, and any other applicable requirements. Seeking professional advice from lawyers or financial advisors is recommended to ensure clarity and compliance.A Kentucky Promissory Note — Forgivable Loan is a legally binding document that outlines the terms and conditions for a loan that may be forgiven under certain circumstances. It is a financial agreement between a lender and a borrower, typically used for financing educational programs, economic development initiatives, entrepreneurship support, or affordable housing projects. In Kentucky, there are several types of Promissory Note — Forgivable Loans offered by various organizations and government agencies. These loans aim to encourage economic growth and support individuals or businesses in need. The common types of Kentucky Promissory Note — Forgivable Loans include: 1. Kentucky Educational Excellence Scholarship (KEEP) Forgivable Loan: The KEEP program provides financial assistance to Kentucky residents who demonstrate academic achievements during high school. Upon entering an eligible Kentucky college or university, a portion of the KEEP award can be converted into a Promissory Note — Forgivable Loan, which can be forgiven if the student graduates with a specific GPA or completes certain qualifying degrees. 2. Kentucky Investment Fund for Nano-Manufacturing (IF): This forgivable loan program supports businesses involved in nano-manufacturing, providing financial assistance to cover eligible project costs such as land acquisition, construction, equipment, and workforce training. The loan can be forgiven if the business meets specific job creation and investment goals within a designated time frame. 3. Kentucky Affordable Housing Trust Fund (KATE) Forgivable Loan: The KATE offers forgivable loans to developers and nonprofit organizations involved in affordable housing projects across the state. The loans can be used to cover predevelopment costs, construction expenses, or preservation efforts. Forgiveness is granted if the project meets specific affordability requirements and remains in compliance with the program's guidelines for a determined period. 4. Kentucky Small Business Tax Credit (SBC) Forgivable Loan: This program is designed to assist small businesses with access to capital for growth and job creation. SBC offers forgivable loans as an incentive for new or existing businesses that create a certain number of qualified jobs within Kentucky. The loan can be forgiven if the business meets the job creation targets over a defined period. These examples showcase the range of Kentucky Promissory Note — Forgivable Loans available, each catering to different sectors and goals. It is essential to carefully review the terms and conditions of each program before entering into a promissory note agreement to fully understand the loan forgiveness conditions, repayment terms, interest rates, and any other applicable requirements. Seeking professional advice from lawyers or financial advisors is recommended to ensure clarity and compliance.