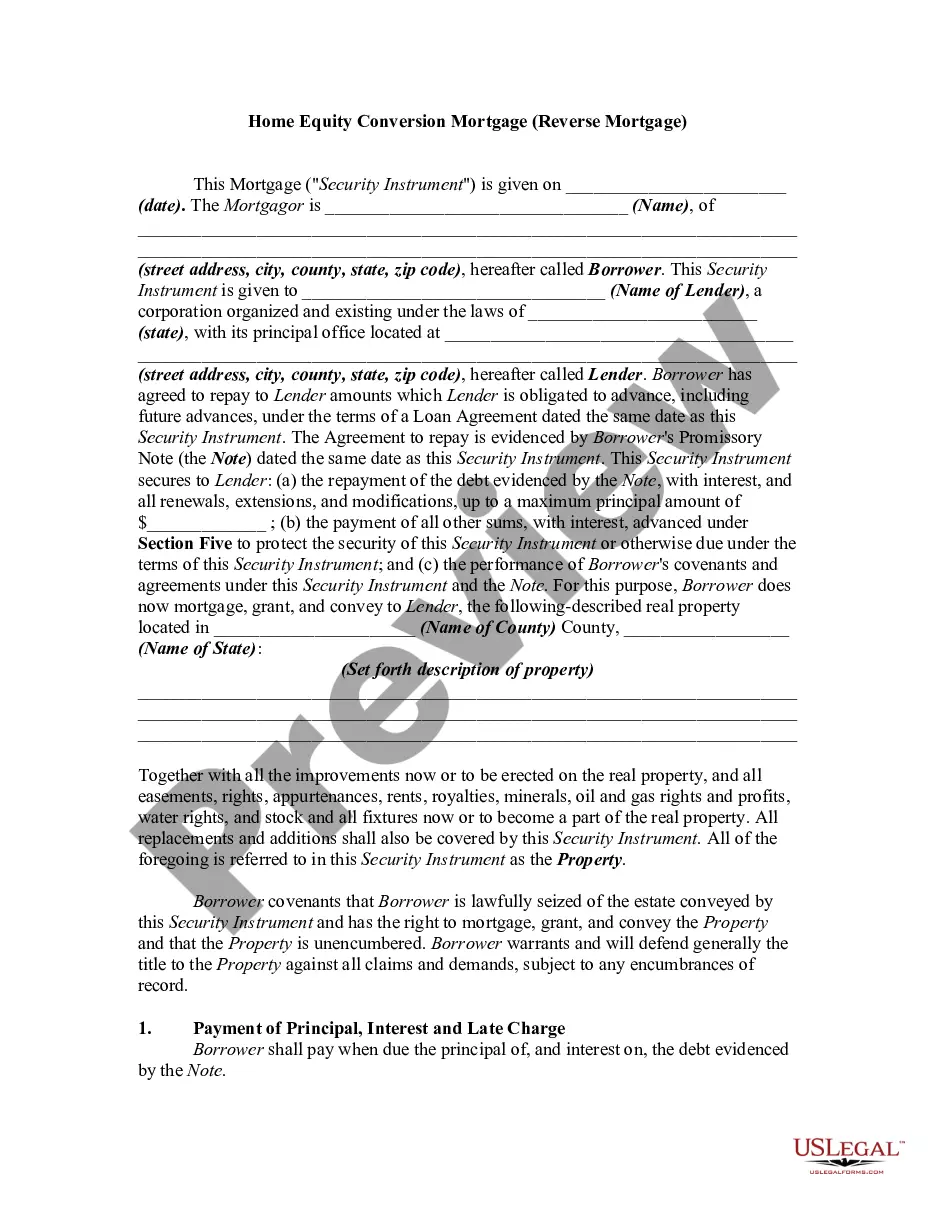

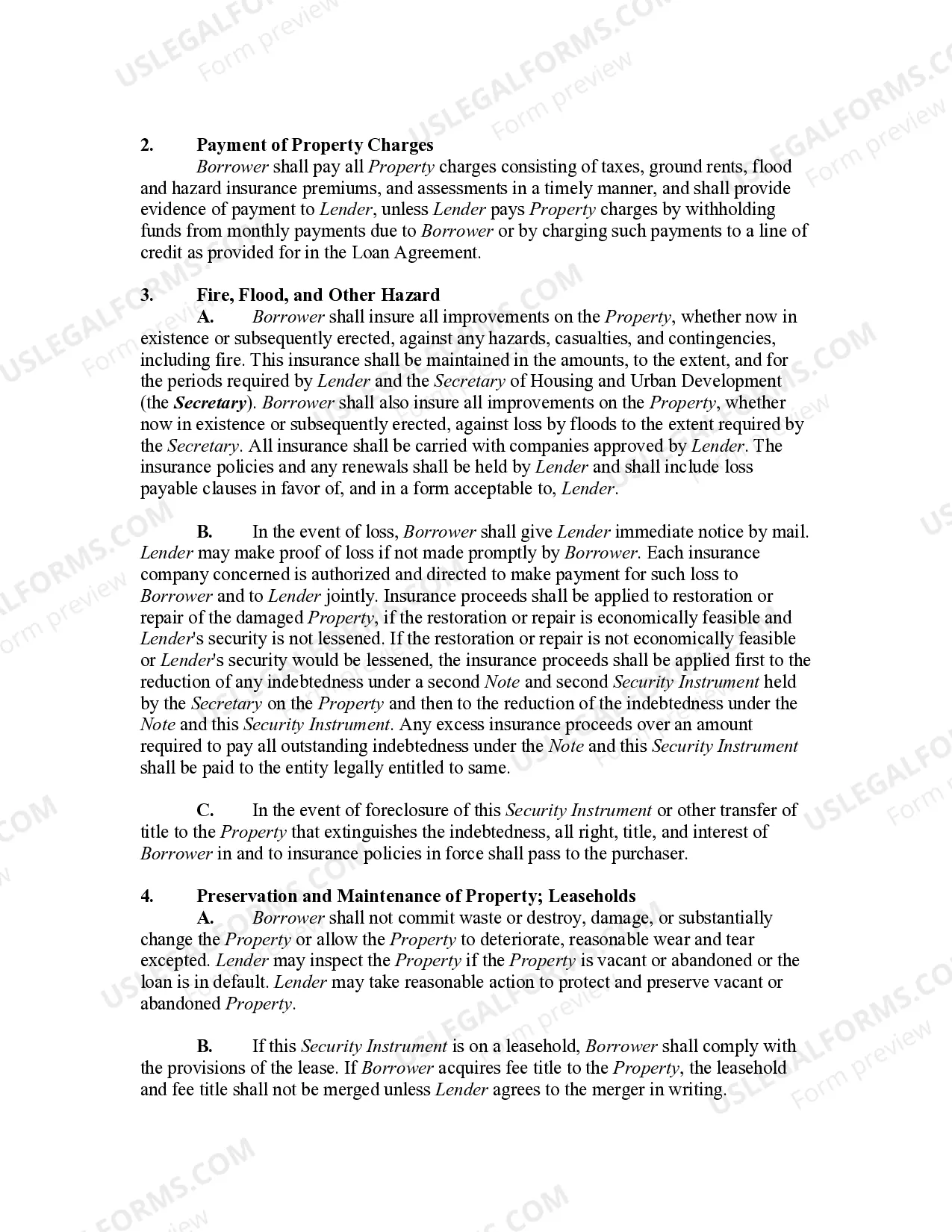

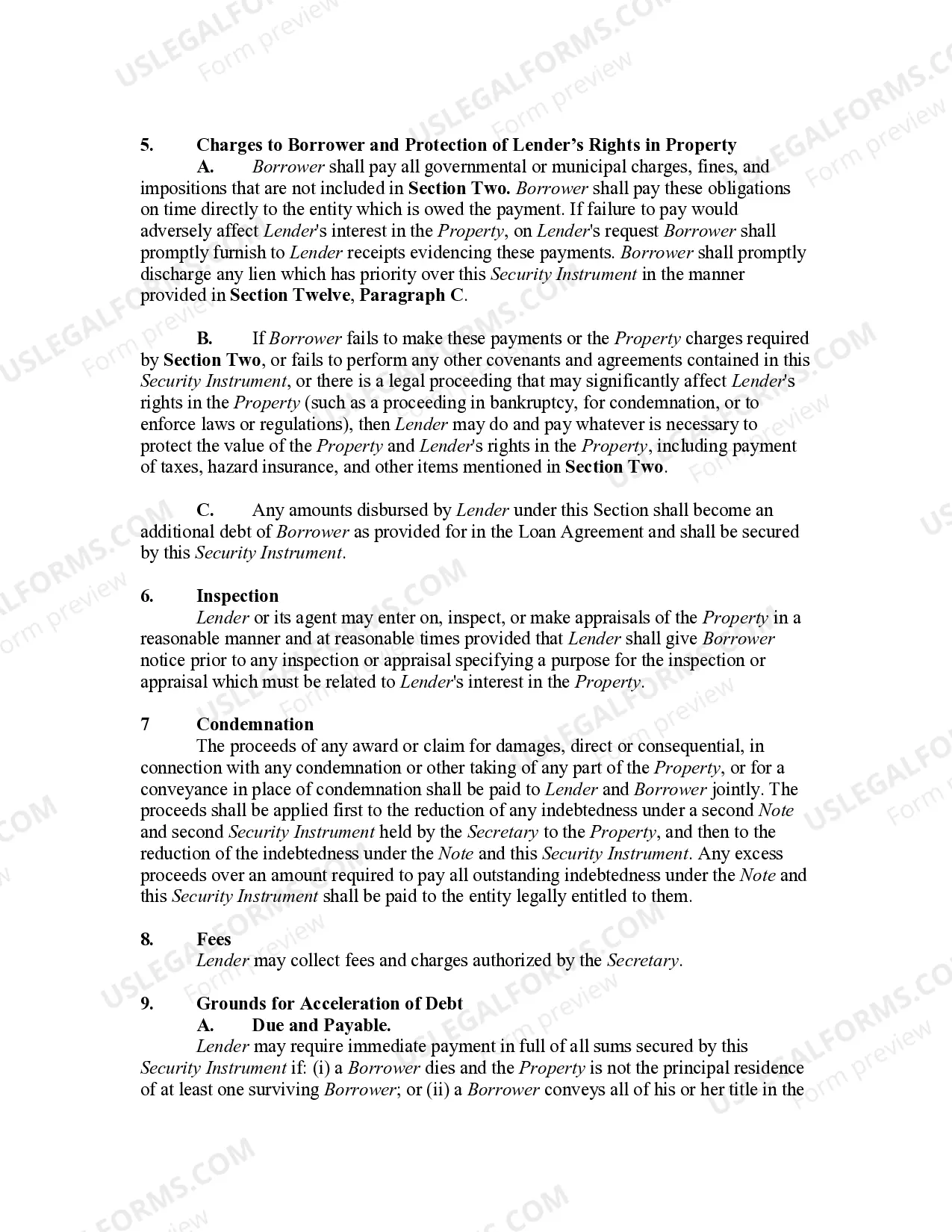

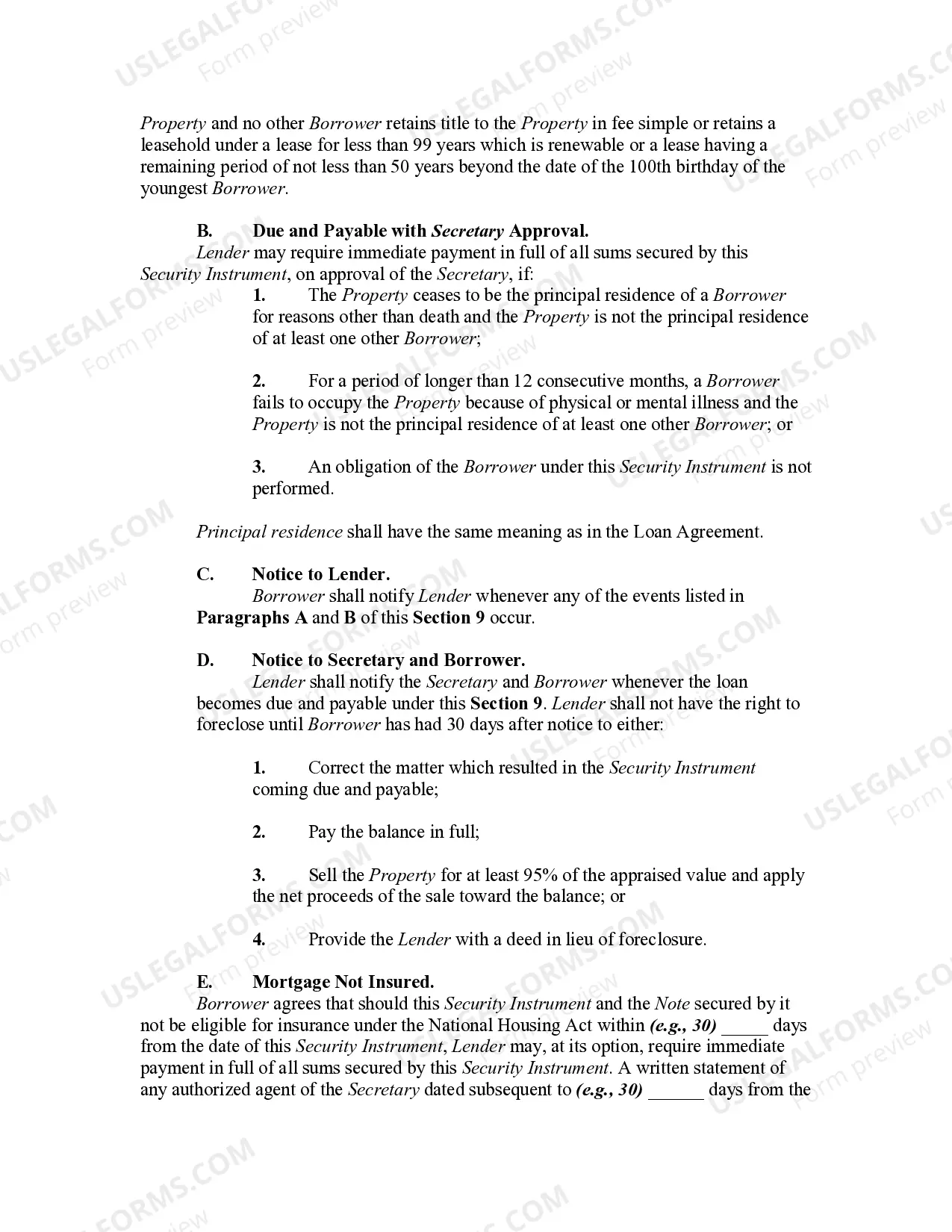

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

A Kentucky Home Equity Conversion Mortgage (HELM) — Reverse Mortgage is a financial product that allows homeowners who are at least 62 years old to access a portion of their home's equity while still living in the property. By converting their home equity into cash, Kentucky residents can supplement their retirement income, cover medical expenses, or finance home renovations, among other purposes. The Kentucky HELM — Reverse Mortgage program is regulated by the federal government and insured by the Federal Housing Administration (FHA). It provides a unique opportunity for seniors to eliminate monthly mortgage payments and receive loan funds in various ways, offering financial flexibility and stability during retirement years. Unlike traditional mortgages, a Kentucky HELM — Reverse Mortgage does not require borrowers to make monthly repayments. Instead, the loan is repaid when the last borrower permanently moves out of the home, passes away, or sells the property. The loan amount is primarily determined based on the homeowner's age, value of the home, and current interest rates. To be eligible for a Kentucky HELM — Reverse Mortgage, homeowners must meet certain requirements, including being at least 62 years old, owning their home outright or having a low remaining mortgage balance, and demonstrating the ability to pay property taxes, insurance, and other property-related expenses. There are different forms of Kentucky HELM — Reverse Mortgages available to residents of the state, depending on their specific needs: 1. Single-Purpose Reverse Mortgage: Offered by local government agencies and nonprofit organizations, this type of reverse mortgage is used for a single, approved purpose, such as home repairs or property taxes. 2. Federally Insured Reverse Mortgage: Most common among Kentucky homeowners, this type is insured by the FHA and allows borrowers to access a larger portion of their home's equity. 3. Proprietary Reverse Mortgage: This reverse mortgage variant is offered by private companies and is suitable for individuals with higher-valued homes, allowing access to more substantial loan amounts. Kentucky's seniors considering a Home Equity Conversion Mortgage — Reverse Mortgage should seek guidance from qualified reverse mortgage counselors or financial advisors. They can assist in understanding the specific terms, benefits, and repayment requirements of each type of reverse mortgage and determine the best option for their unique circumstances.