A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

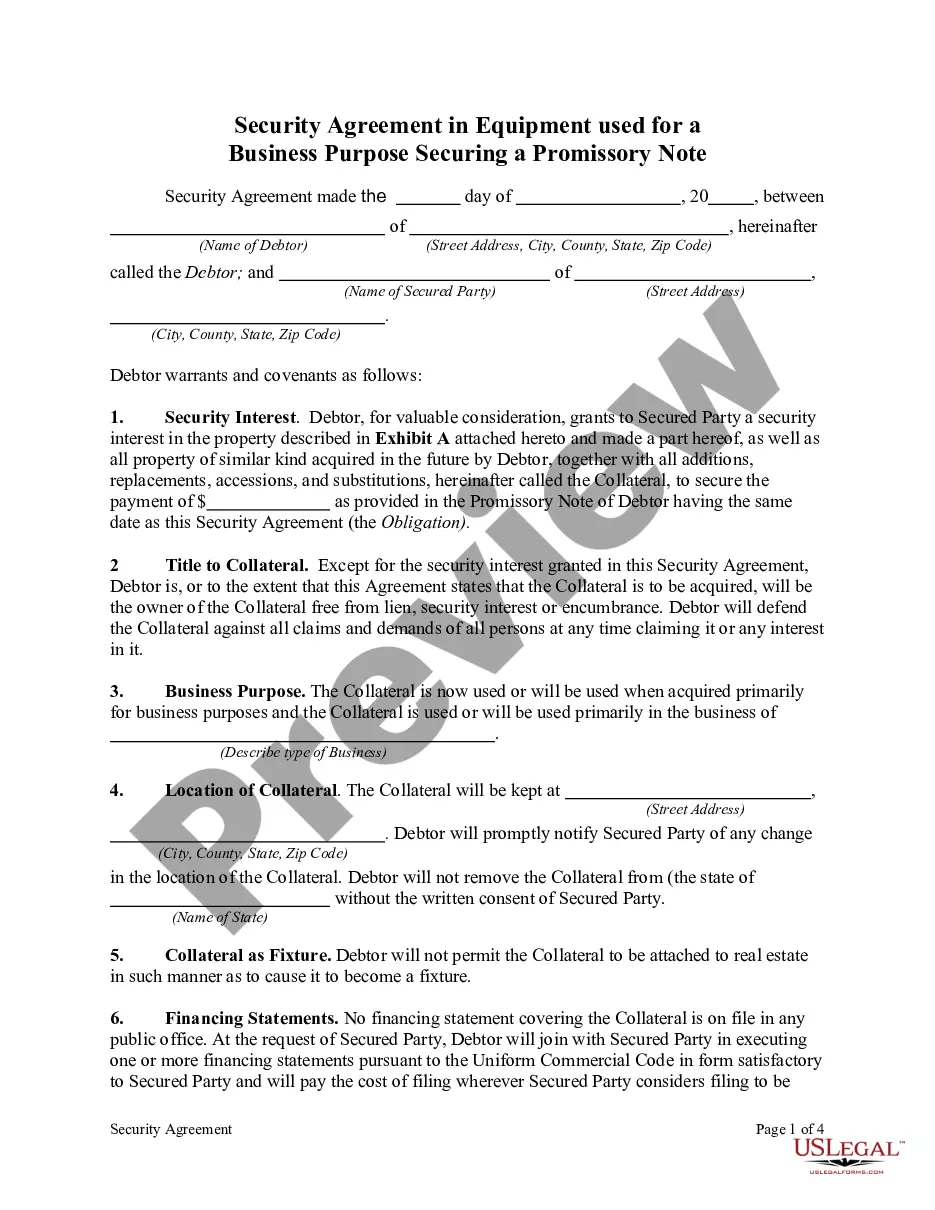

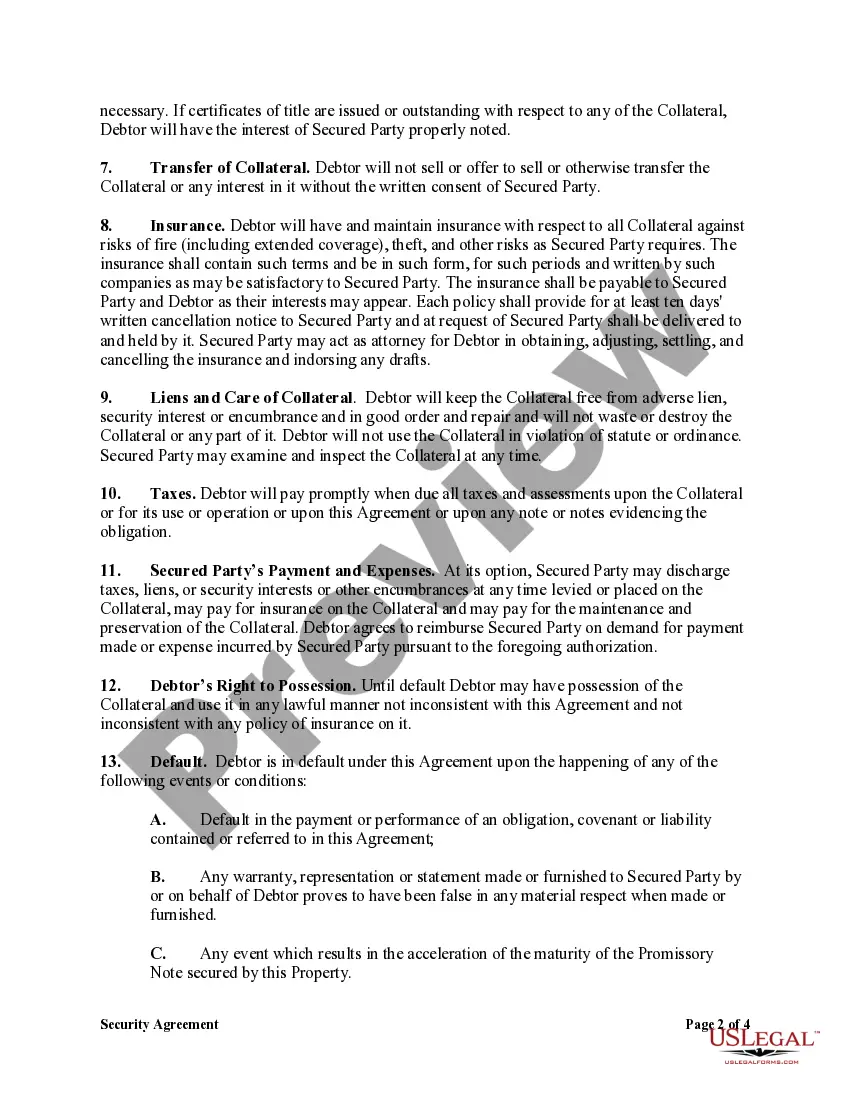

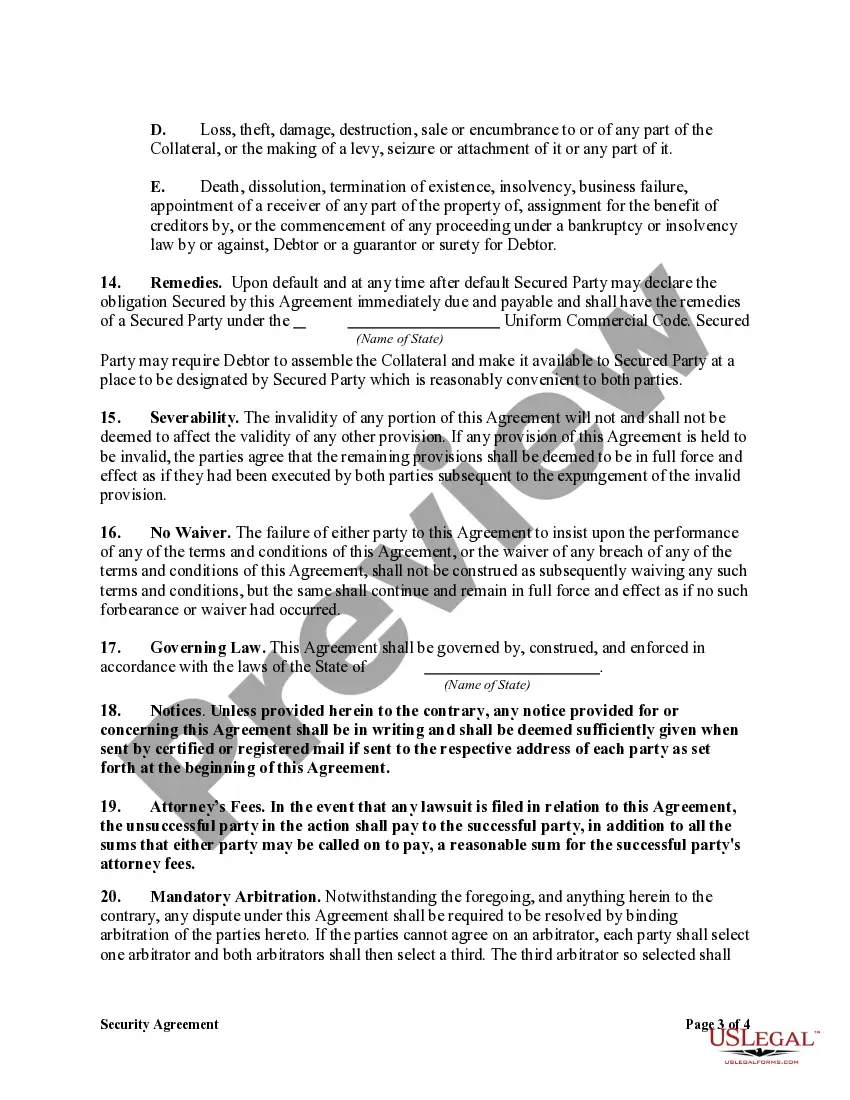

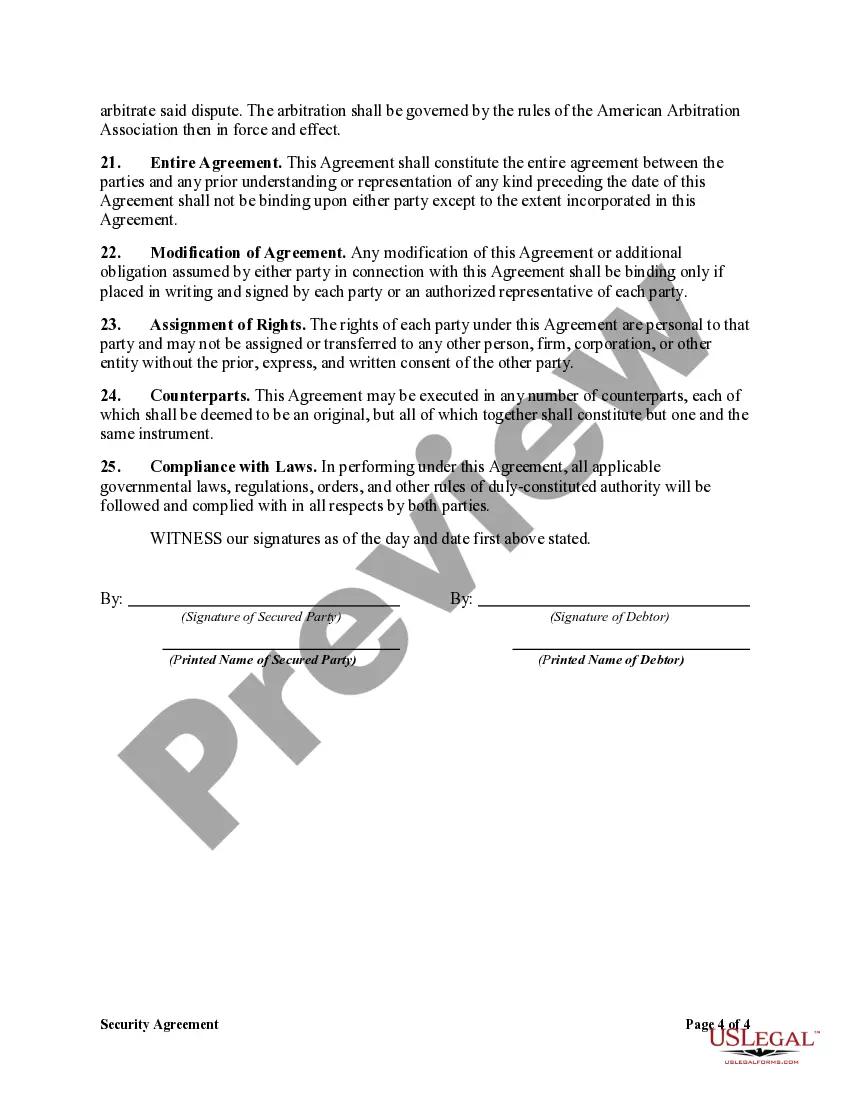

A Kentucky Security Agreement in Equipment for Business Purposes, also known as a security agreement or equipment security agreement, is a legal document used to secure a promissory note in Kentucky. This agreement establishes a lien on specific equipment owned by a business entity as collateral for a loan or financing arrangement. In Kentucky, there are different types of Security Agreements in Equipment for Business Purposes, each with their own characteristics and application: 1. General Security Agreement: This type of agreement is the most common and provides a broad range of security for various types of business equipment. It covers all present and future equipment owned by the business entity, including machinery, vehicles, computers, and other tangible assets. 2. Specific Equipment Security Agreement: This agreement is more specific, targeting individual pieces of equipment. It allows the lender to secure its interest in particular assets owned by the borrower. This type of agreement is often used when a business seeks financing for a specific piece of costly equipment. 3. Floating Lien Security Agreement: A floating lien agreement allows the lender to secure equipment that may change or fluctuate over time. It covers a group or class of assets, rather than specifying particular equipment. The lien "floats" and attaches to new equipment that the business entity acquires, ensuring continuous security for the lender. The content of a Kentucky Security Agreement in Equipment for Business Purposes generally includes the following key elements: 1. Parties: It identifies the borrower (debtor) and the lender (secured party) involved in the agreement. Their legal names, addresses, and contact details are included. 2. Description of Equipment: The agreement provides a comprehensive list or description of the equipment involved, including make, model, serial numbers, and any other relevant identifying information. 3. Grant of Security Interest: The debtor grants a security interest to the lender, allowing them to secure the loan against the specified equipment assets. This section outlines the rights and obligations of both parties. 4. Perfection of Security Interest: The agreement states the necessary steps for perfecting the security interest, such as filing a financing statement with the Kentucky Secretary of State's office or other relevant authority. 5. Default and Remedies: This section outlines the borrower's obligations regarding loan repayment. It specifies the consequences of defaulting on the promissory note and the remedies available to the lender, such as repossession and sale of the equipment. 6. Governing Law and Jurisdiction: The agreement identifies that Kentucky law governs the validity, interpretation, and enforcement of the agreement and provides the jurisdiction for resolving disputes. 7. Additional Clauses: Depending on the specific agreement type and the terms negotiated by the parties, additional clauses may be included addressing topics such as insurance requirements, maintenance and repairs, lease agreements, and subordination agreements. It is essential to consult with a legal professional when drafting or entering into a Kentucky Security Agreement in Equipment for Business Purposes to ensure compliance with local laws and to protect the rights and interests of all parties involved.A Kentucky Security Agreement in Equipment for Business Purposes, also known as a security agreement or equipment security agreement, is a legal document used to secure a promissory note in Kentucky. This agreement establishes a lien on specific equipment owned by a business entity as collateral for a loan or financing arrangement. In Kentucky, there are different types of Security Agreements in Equipment for Business Purposes, each with their own characteristics and application: 1. General Security Agreement: This type of agreement is the most common and provides a broad range of security for various types of business equipment. It covers all present and future equipment owned by the business entity, including machinery, vehicles, computers, and other tangible assets. 2. Specific Equipment Security Agreement: This agreement is more specific, targeting individual pieces of equipment. It allows the lender to secure its interest in particular assets owned by the borrower. This type of agreement is often used when a business seeks financing for a specific piece of costly equipment. 3. Floating Lien Security Agreement: A floating lien agreement allows the lender to secure equipment that may change or fluctuate over time. It covers a group or class of assets, rather than specifying particular equipment. The lien "floats" and attaches to new equipment that the business entity acquires, ensuring continuous security for the lender. The content of a Kentucky Security Agreement in Equipment for Business Purposes generally includes the following key elements: 1. Parties: It identifies the borrower (debtor) and the lender (secured party) involved in the agreement. Their legal names, addresses, and contact details are included. 2. Description of Equipment: The agreement provides a comprehensive list or description of the equipment involved, including make, model, serial numbers, and any other relevant identifying information. 3. Grant of Security Interest: The debtor grants a security interest to the lender, allowing them to secure the loan against the specified equipment assets. This section outlines the rights and obligations of both parties. 4. Perfection of Security Interest: The agreement states the necessary steps for perfecting the security interest, such as filing a financing statement with the Kentucky Secretary of State's office or other relevant authority. 5. Default and Remedies: This section outlines the borrower's obligations regarding loan repayment. It specifies the consequences of defaulting on the promissory note and the remedies available to the lender, such as repossession and sale of the equipment. 6. Governing Law and Jurisdiction: The agreement identifies that Kentucky law governs the validity, interpretation, and enforcement of the agreement and provides the jurisdiction for resolving disputes. 7. Additional Clauses: Depending on the specific agreement type and the terms negotiated by the parties, additional clauses may be included addressing topics such as insurance requirements, maintenance and repairs, lease agreements, and subordination agreements. It is essential to consult with a legal professional when drafting or entering into a Kentucky Security Agreement in Equipment for Business Purposes to ensure compliance with local laws and to protect the rights and interests of all parties involved.