This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

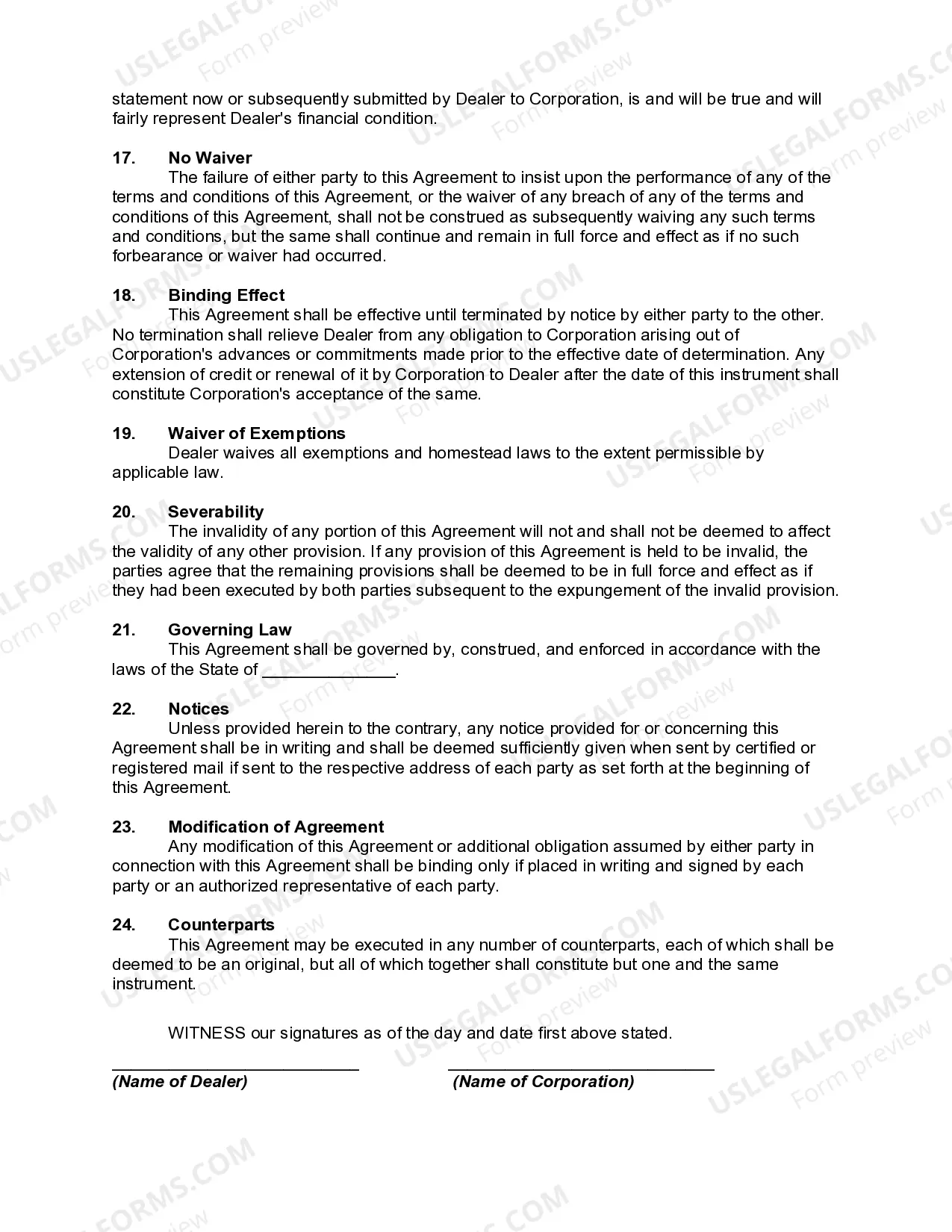

A Kentucky Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles is a legal contract that outlines the terms and conditions of a financing arrangement between a dealer and a credit corporation. This agreement allows the dealer to obtain wholesale financing to purchase inventory, while also granting the credit corporation a security interest in the dealer's accounts and general intangible assets. In this type of financing agreement, the dealer typically approaches a credit corporation to secure funds for purchasing inventory in bulk. The credit corporation may have different types of financing agreements available to suit the specific needs of the dealer. These agreements may include: 1. Traditional Wholesale Financing Agreement: This is the most common type of financing agreement wherein the credit corporation extends a line of credit to the dealer based on the creditworthiness and financial stability of the dealer. The dealer can then use this line of credit to purchase inventory for resale. 2. Floor Plan Financing Agreement: This type of agreement specifically caters to dealers in the automotive, RV, boat, or power sports industry. The credit corporation provides funding to the dealer to acquire vehicles or equipment for their showroom or lot. The credit corporation then holds a security interest in these assets, allowing them to repossess and sell them in case of default. 3. Inventory Financing Agreement: This agreement focuses on providing funds to cover the cost of the dealer's existing inventory. It allows the dealer to free up working capital tied up in inventory by using their inventory as collateral. The credit corporation takes a security interest in the dealer's inventory and can seize and liquidate it in case of default. 4. Accounts Receivable Financing Agreement: In this type of agreement, the dealer can obtain financing based on their accounts receivable. The credit corporation advances funds to the dealer against their outstanding invoices, enabling them to meet immediate financial obligations. The credit corporation retains a security interest in the dealer's accounts and has the right to collect on them if necessary. The Kentucky Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security Interest in Accounts and General Intangibles is a legally binding document that protects the rights and interests of both parties involved. It specifies the loan amount, interest rate, repayment terms, default provisions, and the process for enforcing the security interest. It is crucial for both parties to thoroughly review and understand the terms and conditions outlined in the agreement before signing. Consulting with legal professionals experienced in financing and commercial law is advisable to ensure compliance with Kentucky laws and regulations.