Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

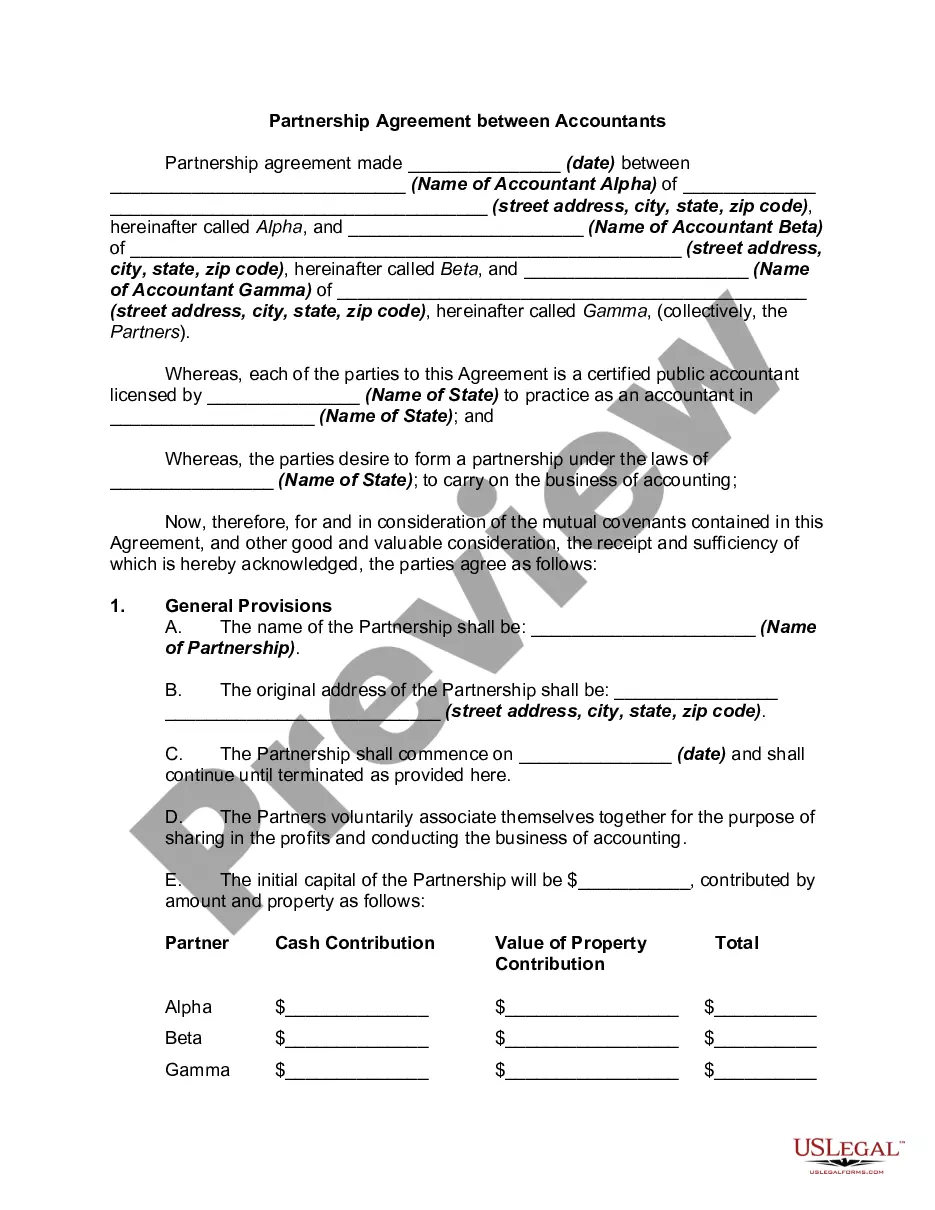

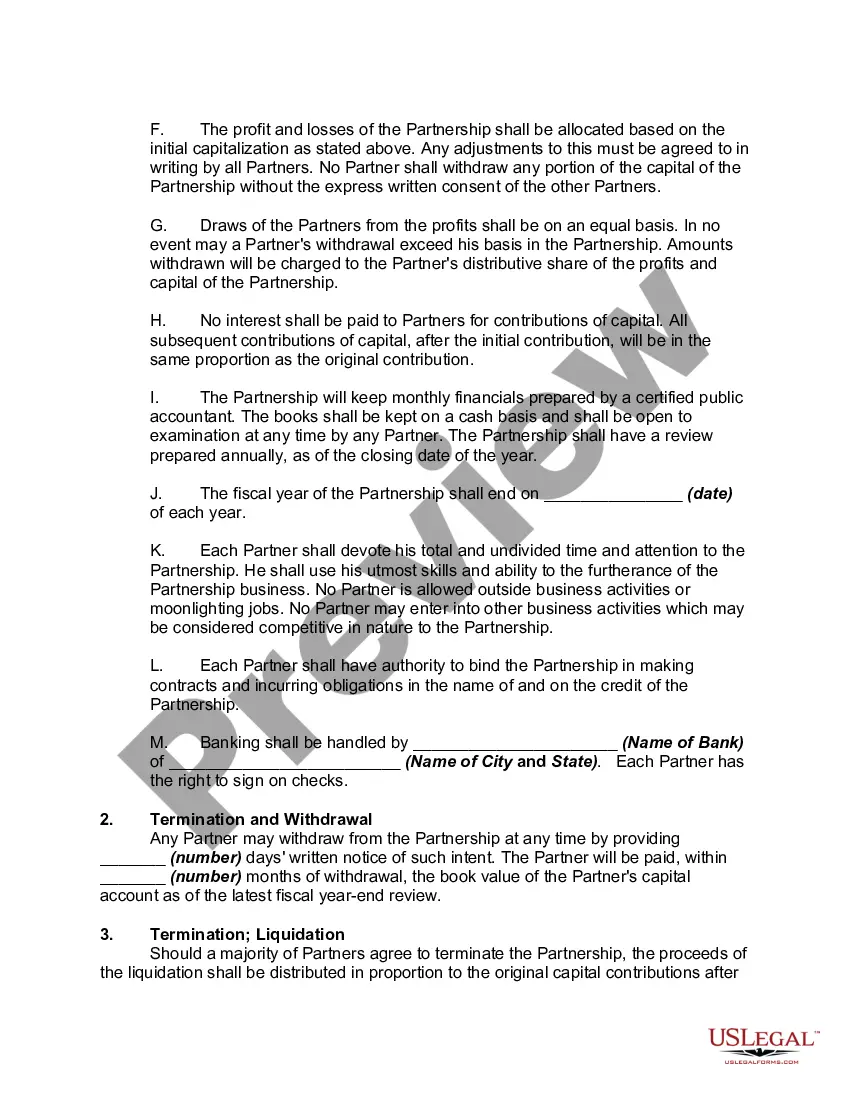

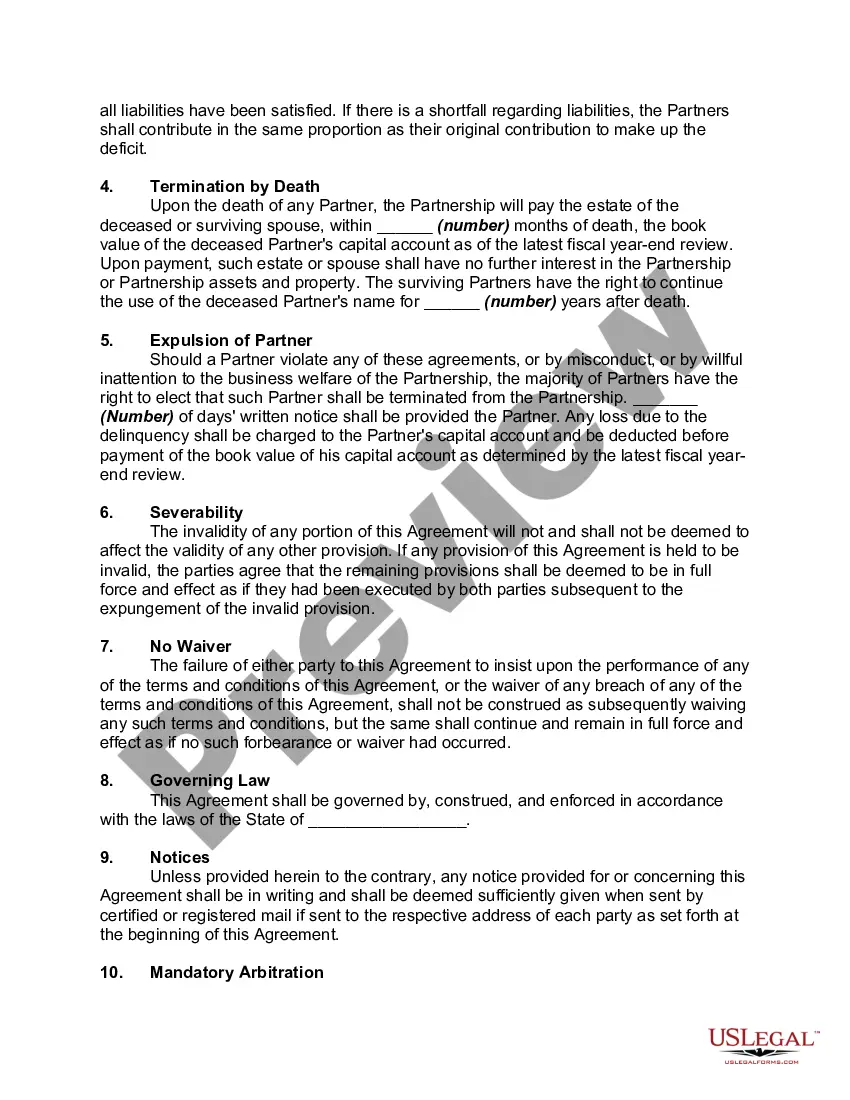

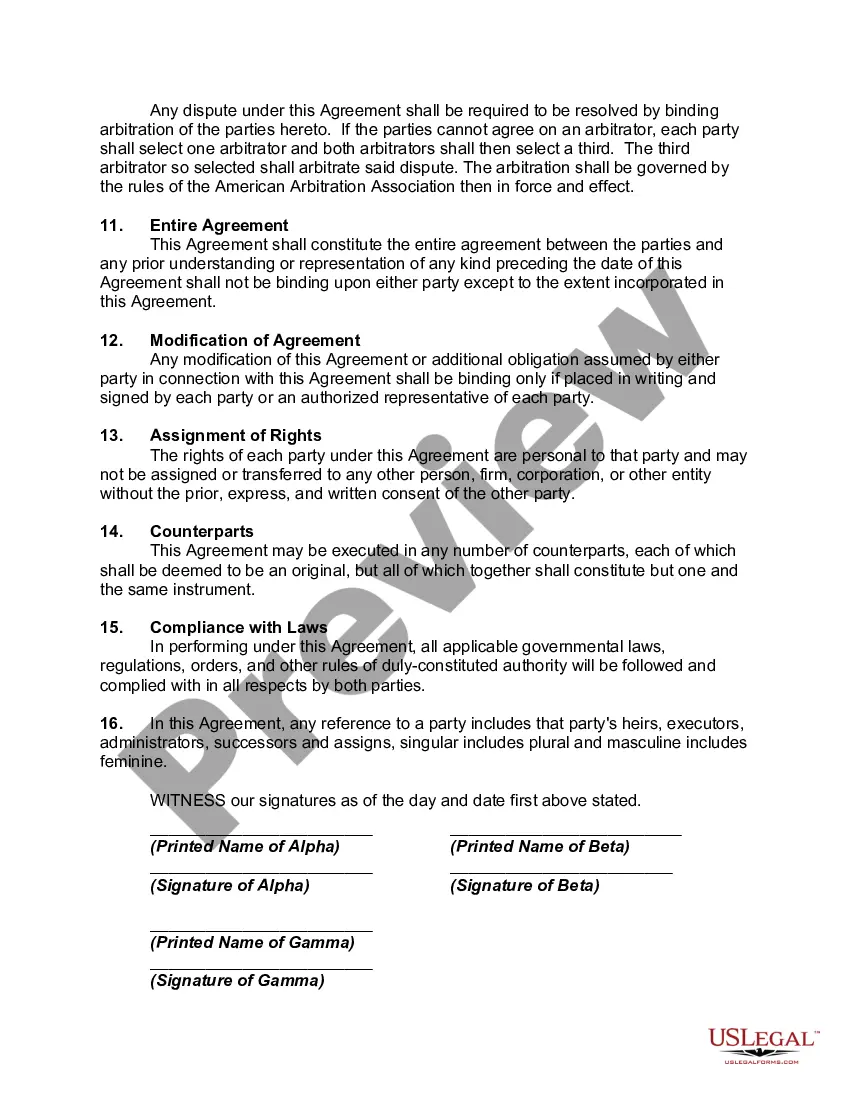

A Kentucky Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions agreed upon by accountants who wish to form a partnership in the state of Kentucky. This agreement serves as the foundation for their business relationship and provides clarity on various aspects of the partnership, such as decision-making, profit-sharing, liabilities, and dissolution. In Kentucky, there are two main types of partnership agreements that accountants may consider: 1. General Partnership Agreement: This type of partnership agreement is commonly chosen by accountants who want to form a traditional general partnership. In this arrangement, all partners have equal rights and responsibilities, share profits and losses equally, and have unlimited personal liability for the partnership's debts and obligations. The partnership operates under a single business name, and each partner can actively participate in the management and decision-making process. 2. Limited Liability Partnership (LLP) Agreement: Some accountants may prefer the protection offered by an LLP agreement. In an LLP, partners have limited personal liability for the partnership's debts and liabilities beyond their initial investment. This form of partnership protects individual partners from being held personally responsible for the actions or misconduct of other partners. However, Laps are subject to certain statutory requirements and restrictions outlined by Kentucky law. The Kentucky Partnership Agreement Between Accountants typically covers the following key areas: 1. Name and Purpose: The agreement begins by specifying the partnership's legal name and its primary purpose or business focus. 2. Contributions: It outlines the contributions each partner will make to the partnership, which can include capital, assets, or services. 3. Profits and Losses: The agreement details how profits and losses will be shared among the partners, whether equally or based on a predetermined ratio or formula. 4. Decision-Making: It establishes the decision-making process within the partnership, including voting rights, decision thresholds, and procedures for resolving disputes. 5. Authority and Responsibilities: This section defines the authority and responsibilities of each partner, highlighting their areas of expertise, roles in management, and obligations towards the partnership. 6. Liabilities and Indemnification: It clarifies the personal liability of each partner, whether they have unlimited liability (as in a general partnership) or limited liability (as in an LLP). It may also outline indemnification provisions to protect partners against certain liabilities. 7. Dissolution and Termination: It outlines the procedures for dissolving the partnership, including the distribution of assets, settling liabilities, and notifying relevant parties. 8. Admission of New Partners: If the partners intend to allow new members to join the partnership in the future, the agreement may define the criteria, process, and terms for admitting new partners. It is imperative for accountants in Kentucky to consult with a legal professional who specializes in partnership agreements to ensure their document complies with state laws and effectively protects their rights and interests. Additionally, specific keywords to consider while describing this topic in content may include: Kentucky partnership agreement, accountants, business relationship, terms and conditions, decision-making, profit-sharing, liabilities, dissolution, general partnership agreement, limited liability partnership, personal liability, unlimited liability, LLP agreement, contributions, profits, losses, decision-making process, voting rights, authority, responsibilities, indemnification, dissolution procedures, admission of new partners, legal professional, and state laws.A Kentucky Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions agreed upon by accountants who wish to form a partnership in the state of Kentucky. This agreement serves as the foundation for their business relationship and provides clarity on various aspects of the partnership, such as decision-making, profit-sharing, liabilities, and dissolution. In Kentucky, there are two main types of partnership agreements that accountants may consider: 1. General Partnership Agreement: This type of partnership agreement is commonly chosen by accountants who want to form a traditional general partnership. In this arrangement, all partners have equal rights and responsibilities, share profits and losses equally, and have unlimited personal liability for the partnership's debts and obligations. The partnership operates under a single business name, and each partner can actively participate in the management and decision-making process. 2. Limited Liability Partnership (LLP) Agreement: Some accountants may prefer the protection offered by an LLP agreement. In an LLP, partners have limited personal liability for the partnership's debts and liabilities beyond their initial investment. This form of partnership protects individual partners from being held personally responsible for the actions or misconduct of other partners. However, Laps are subject to certain statutory requirements and restrictions outlined by Kentucky law. The Kentucky Partnership Agreement Between Accountants typically covers the following key areas: 1. Name and Purpose: The agreement begins by specifying the partnership's legal name and its primary purpose or business focus. 2. Contributions: It outlines the contributions each partner will make to the partnership, which can include capital, assets, or services. 3. Profits and Losses: The agreement details how profits and losses will be shared among the partners, whether equally or based on a predetermined ratio or formula. 4. Decision-Making: It establishes the decision-making process within the partnership, including voting rights, decision thresholds, and procedures for resolving disputes. 5. Authority and Responsibilities: This section defines the authority and responsibilities of each partner, highlighting their areas of expertise, roles in management, and obligations towards the partnership. 6. Liabilities and Indemnification: It clarifies the personal liability of each partner, whether they have unlimited liability (as in a general partnership) or limited liability (as in an LLP). It may also outline indemnification provisions to protect partners against certain liabilities. 7. Dissolution and Termination: It outlines the procedures for dissolving the partnership, including the distribution of assets, settling liabilities, and notifying relevant parties. 8. Admission of New Partners: If the partners intend to allow new members to join the partnership in the future, the agreement may define the criteria, process, and terms for admitting new partners. It is imperative for accountants in Kentucky to consult with a legal professional who specializes in partnership agreements to ensure their document complies with state laws and effectively protects their rights and interests. Additionally, specific keywords to consider while describing this topic in content may include: Kentucky partnership agreement, accountants, business relationship, terms and conditions, decision-making, profit-sharing, liabilities, dissolution, general partnership agreement, limited liability partnership, personal liability, unlimited liability, LLP agreement, contributions, profits, losses, decision-making process, voting rights, authority, responsibilities, indemnification, dissolution procedures, admission of new partners, legal professional, and state laws.