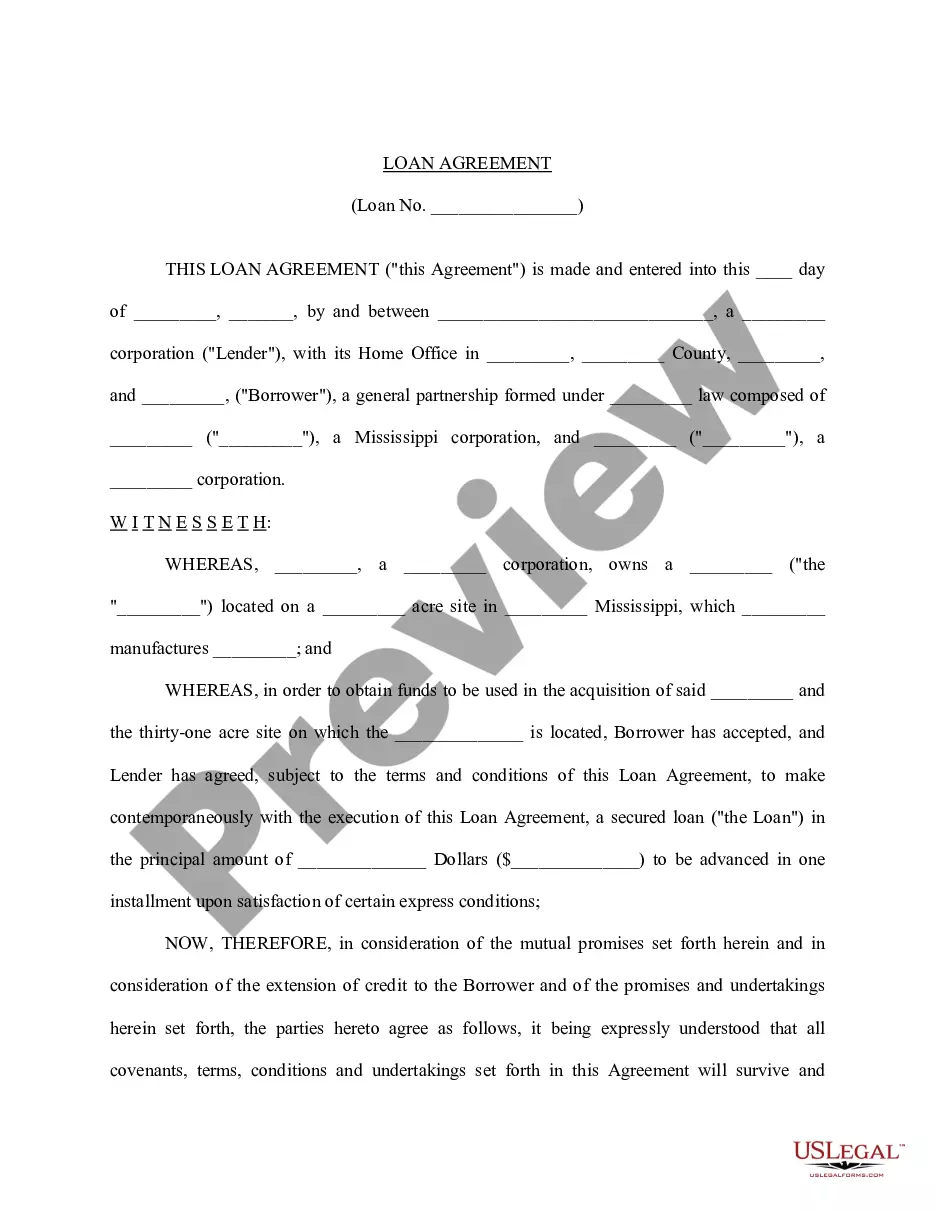

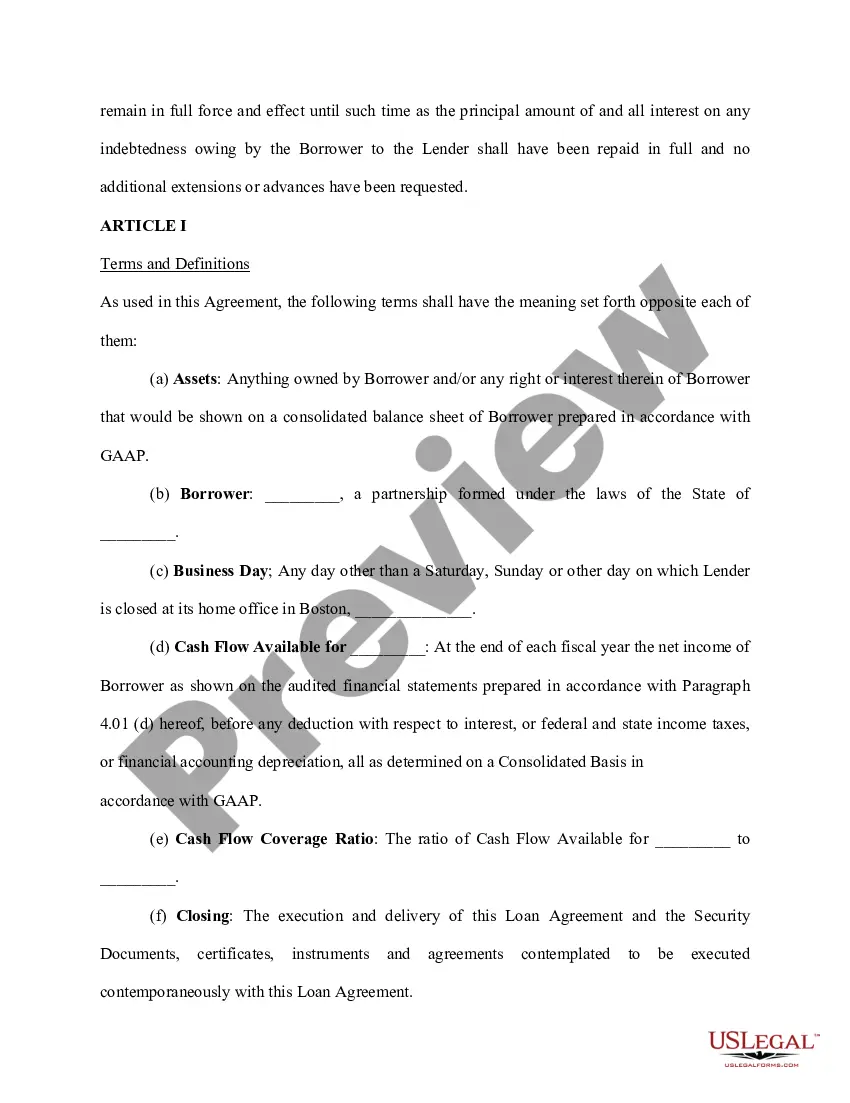

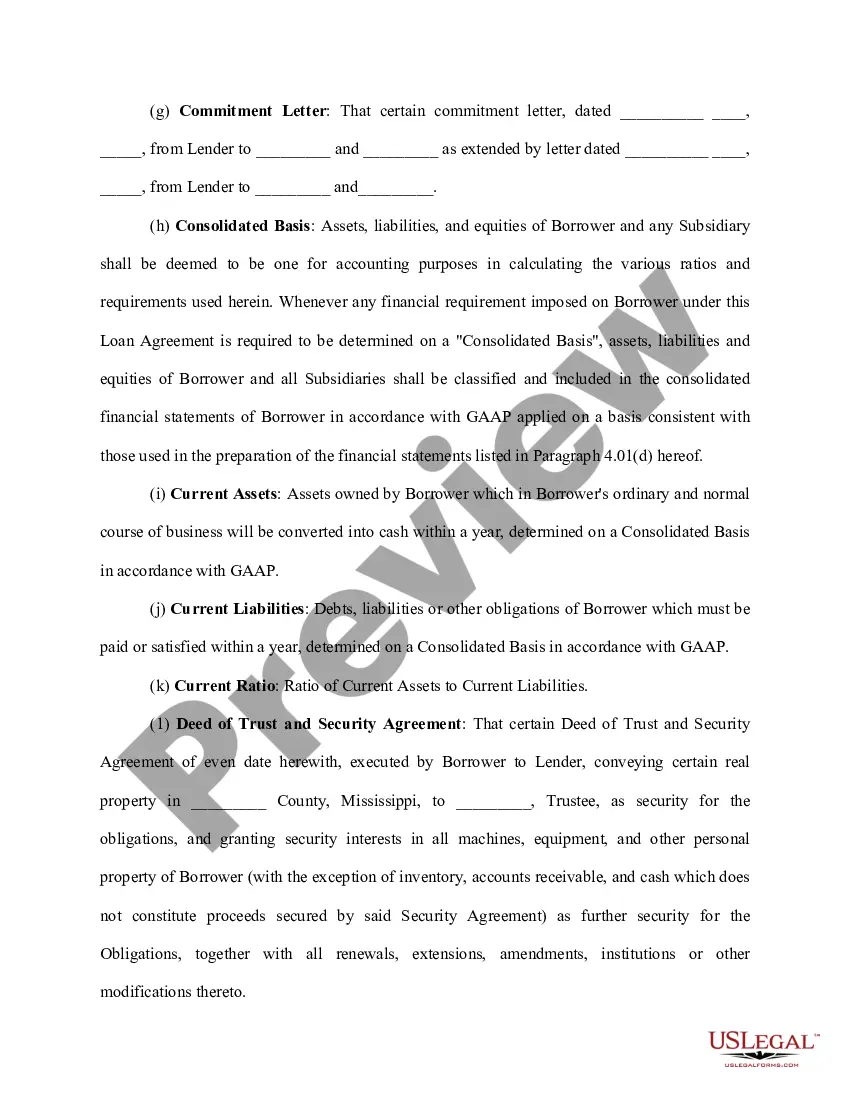

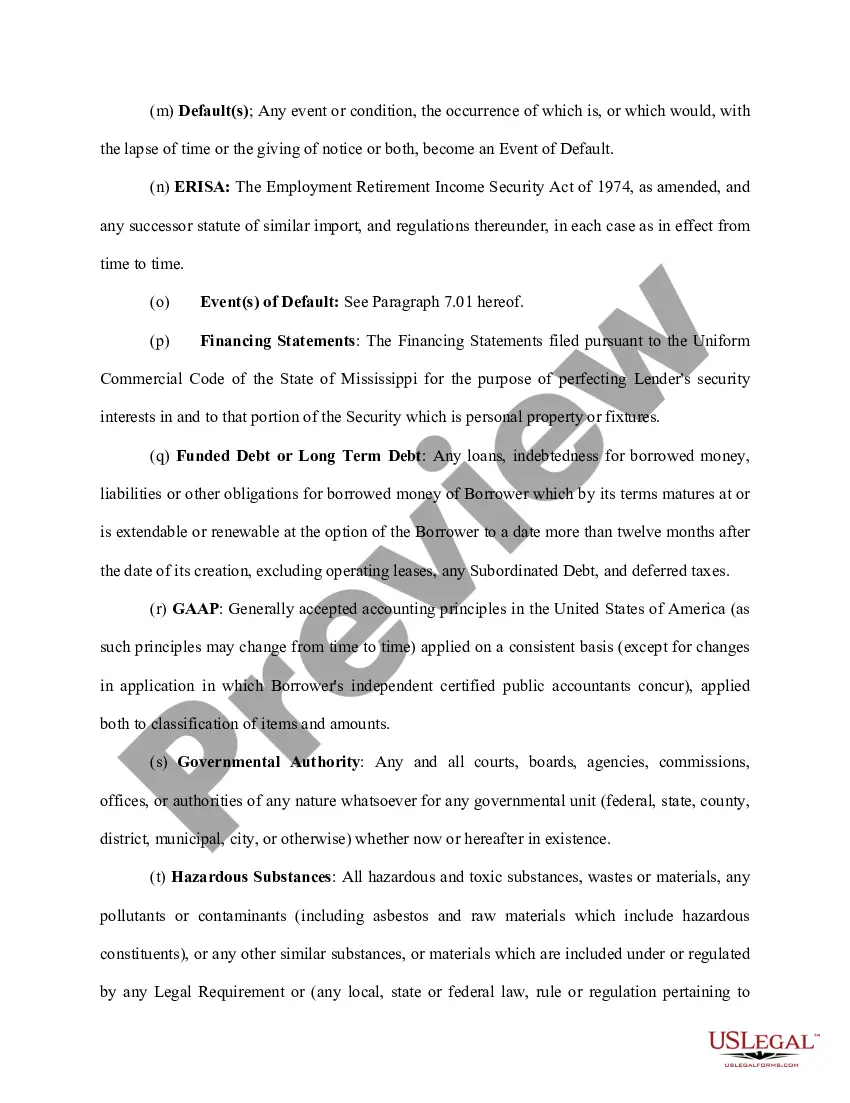

A Kentucky Loan Agreement for Horse refers to a legal contract established between a lender and a borrower involved in the horse industry. This agreement outlines the terms and conditions regarding the loan of a horse in the state of Kentucky, ensuring clarity and protection for all parties involved. One type of Kentucky Loan Agreement for Horse is the Full Lease Agreement. This arrangement allows the borrower, often referred to as the lessee, to have full possession and control of the horse for a specified period. The lessee is responsible for all expenses related to the horse's care, including boarding, veterinary costs, and competition fees, while the lender retains legal ownership. Another type is the Half-Lease Agreement, where the horse is shared between the lender and the lessee. In this case, both parties agree upon the division of responsibilities and expenses. The lessee may have access to the horse for specific days of the week, while the lender retains certain rights and involvement. The Kentucky Loan Agreement for Horse typically includes essential components such as: 1. Identification of the horse: This includes the horse's registered name, age, breed, color, markings, and any distinguishing features. 2. Purpose of the loan: The agreement describes the intended purpose of the horse's use, whether it is for personal pleasure, competition, breeding, or other specific activities. 3. Duration of the loan: The agreement specifies the start and end date of the loan, providing clarity on the length of the agreement, which could be for a specific time frame or an ongoing arrangement. 4. Rights and responsibilities: This section outlines the rights and responsibilities of both the lender and the borrower. It includes details on who will be responsible for the horse's care, feeding, veterinary expenses, transportation, insurance coverage, and registration fees. 5. Termination clauses: The agreement establishes the circumstances under which the loan can be terminated, including default on payment, breach of agreed-upon terms, or if the horse's well-being is compromised. 6. Ownership transfer: If the loan agreement includes an option to purchase the horse, it will outline the terms and conditions for transferring legal ownership, including purchase price, payment terms, and requirements for a veterinary examination. 7. Governing law: Since this is a Kentucky-specific agreement, it will also mention the applicable state laws and jurisdiction in case any legal disputes arise. In conclusion, a Kentucky Loan Agreement for Horse is a comprehensive legal contract that sets out the terms and conditions for loaning a horse in the state. It ensures the rights and responsibilities of both the lender and borrower, while providing a clear framework for the horse's care, use, and potential ownership transfer.

Kentucky Loan Agreement for Horse

Description

How to fill out Kentucky Loan Agreement For Horse?

Choosing the right lawful papers format can be a have a problem. Naturally, there are tons of themes available online, but how would you get the lawful form you will need? Use the US Legal Forms site. The service delivers thousands of themes, including the Kentucky Loan Agreement for Horse, which you can use for business and private requires. All the kinds are examined by specialists and satisfy federal and state requirements.

If you are already signed up, log in to your accounts and click on the Acquire switch to obtain the Kentucky Loan Agreement for Horse. Utilize your accounts to look from the lawful kinds you may have ordered earlier. Proceed to the My Forms tab of your respective accounts and acquire another duplicate from the papers you will need.

If you are a whole new customer of US Legal Forms, allow me to share simple directions so that you can stick to:

- First, ensure you have chosen the right form for your personal town/area. You can look over the form while using Review switch and read the form information to guarantee it will be the best for you.

- In case the form fails to satisfy your preferences, take advantage of the Seach industry to obtain the proper form.

- When you are certain that the form would work, select the Acquire now switch to obtain the form.

- Select the costs plan you want and enter in the needed information. Create your accounts and buy the order making use of your PayPal accounts or Visa or Mastercard.

- Opt for the data file format and down load the lawful papers format to your device.

- Full, change and print out and indicator the received Kentucky Loan Agreement for Horse.

US Legal Forms may be the greatest collection of lawful kinds for which you can see various papers themes. Use the company to down load professionally-made papers that stick to express requirements.