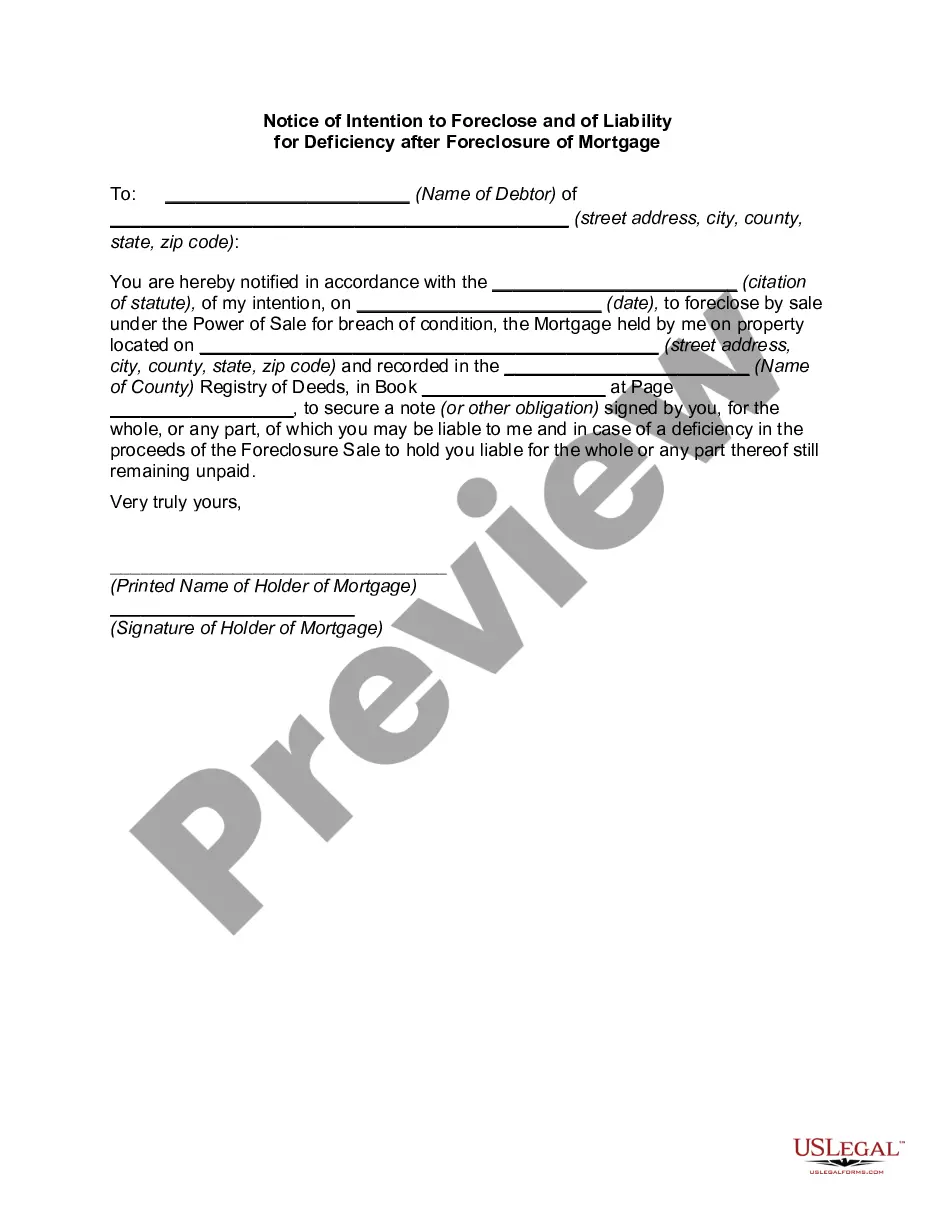

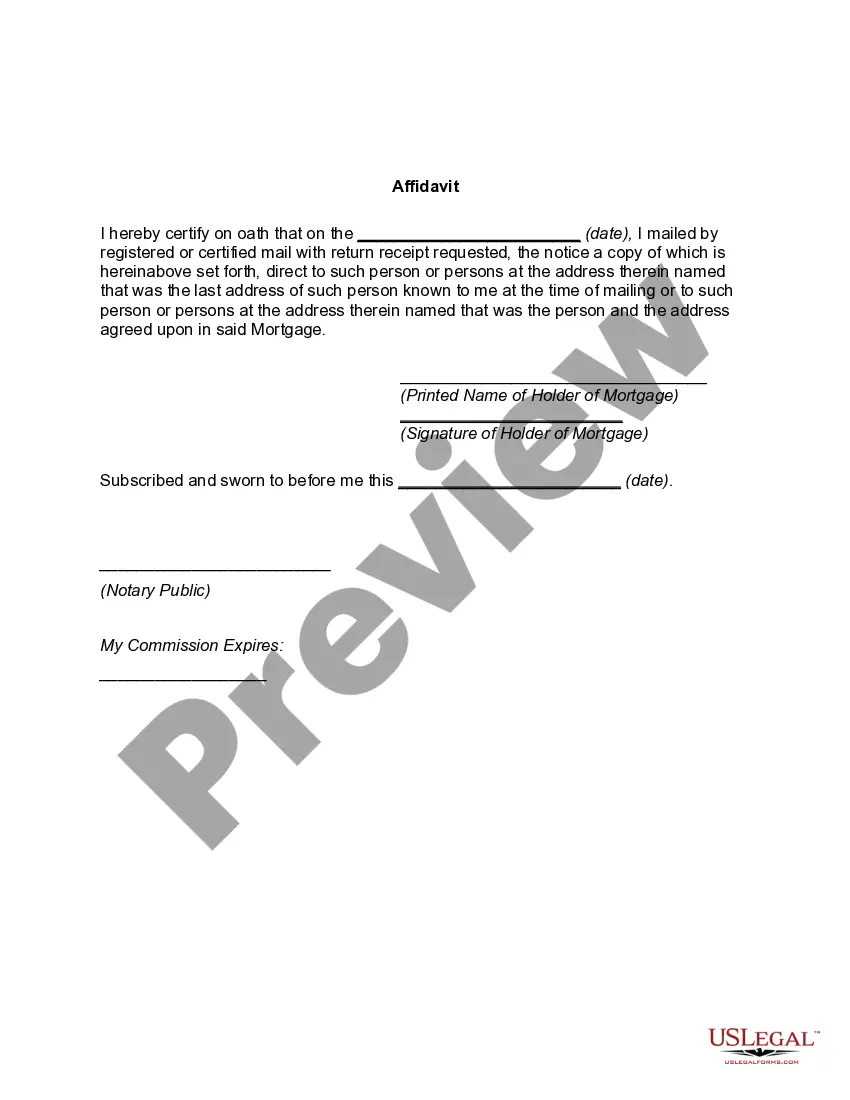

The Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is a legal document that serves as a formal notice to inform borrowers of an impending foreclosure on their property. It outlines the lender's intention to initiate foreclosure proceedings and provides information regarding the borrower's liability for any deficiency after the foreclosure process is complete. One type of Kentucky Notice of Intention to Foreclose is the "Pre-Foreclosure Notice," which is typically sent to the borrower prior to initiating any legal action against them. This notice serves as a warning and gives borrowers an opportunity to rectify the default or negotiate alternative solutions to avoid foreclosure. Another type of Kentucky Notice of Liability for Deficiency after Foreclosure is the "Deficiency Letter." This notice is sent to borrowers after the foreclosure process has been completed and details the remaining balance on the mortgage loan that remains unpaid after the sale of the property. It informs the borrower of their potential liability for the deficiency and may provide instructions for repayment or resolve any disputes related to the amount owed. The Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is an important legal document that outlines the rights and responsibilities of both the lender and the borrower throughout the foreclosure process. It is crucial for borrowers to carefully read and understand the contents of these notices, seek legal advice if necessary, and take appropriate actions to protect their interests. Failure to respond or address the outstanding issues can result in severe consequences, including legal actions, property loss, and damaged credit history. If you receive a Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, it is essential to review it thoroughly and ensure that all necessary steps are taken to address the situation promptly. Seeking professional help, such as consulting with an attorney or a housing counselor, can provide valuable guidance and support in navigating the foreclosure process and protecting your rights as a borrower.

Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Kentucky Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

US Legal Forms - one of several greatest libraries of legitimate varieties in the United States - gives a variety of legitimate record web templates you can acquire or print. Making use of the internet site, you can find a huge number of varieties for enterprise and person reasons, categorized by categories, claims, or keywords.You can find the most recent versions of varieties just like the Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage in seconds.

If you already possess a subscription, log in and acquire Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage from your US Legal Forms catalogue. The Down load button can look on each and every type you perspective. You have accessibility to all in the past saved varieties inside the My Forms tab of your own bank account.

If you would like use US Legal Forms initially, listed below are straightforward guidelines to get you started out:

- Be sure you have picked the correct type for the metropolis/region. Go through the Preview button to analyze the form`s articles. See the type explanation to ensure that you have selected the proper type.

- In case the type does not fit your requirements, take advantage of the Search industry at the top of the monitor to obtain the one which does.

- Should you be content with the shape, validate your decision by simply clicking the Purchase now button. Then, select the prices strategy you want and supply your qualifications to register on an bank account.

- Approach the financial transaction. Make use of credit card or PayPal bank account to accomplish the financial transaction.

- Pick the format and acquire the shape in your system.

- Make modifications. Complete, change and print and sign the saved Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

Every single template you included in your money does not have an expiration particular date and is your own property forever. So, in order to acquire or print another backup, just proceed to the My Forms segment and click on about the type you will need.

Get access to the Kentucky Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage with US Legal Forms, the most extensive catalogue of legitimate record web templates. Use a huge number of skilled and state-distinct web templates that meet your small business or person demands and requirements.