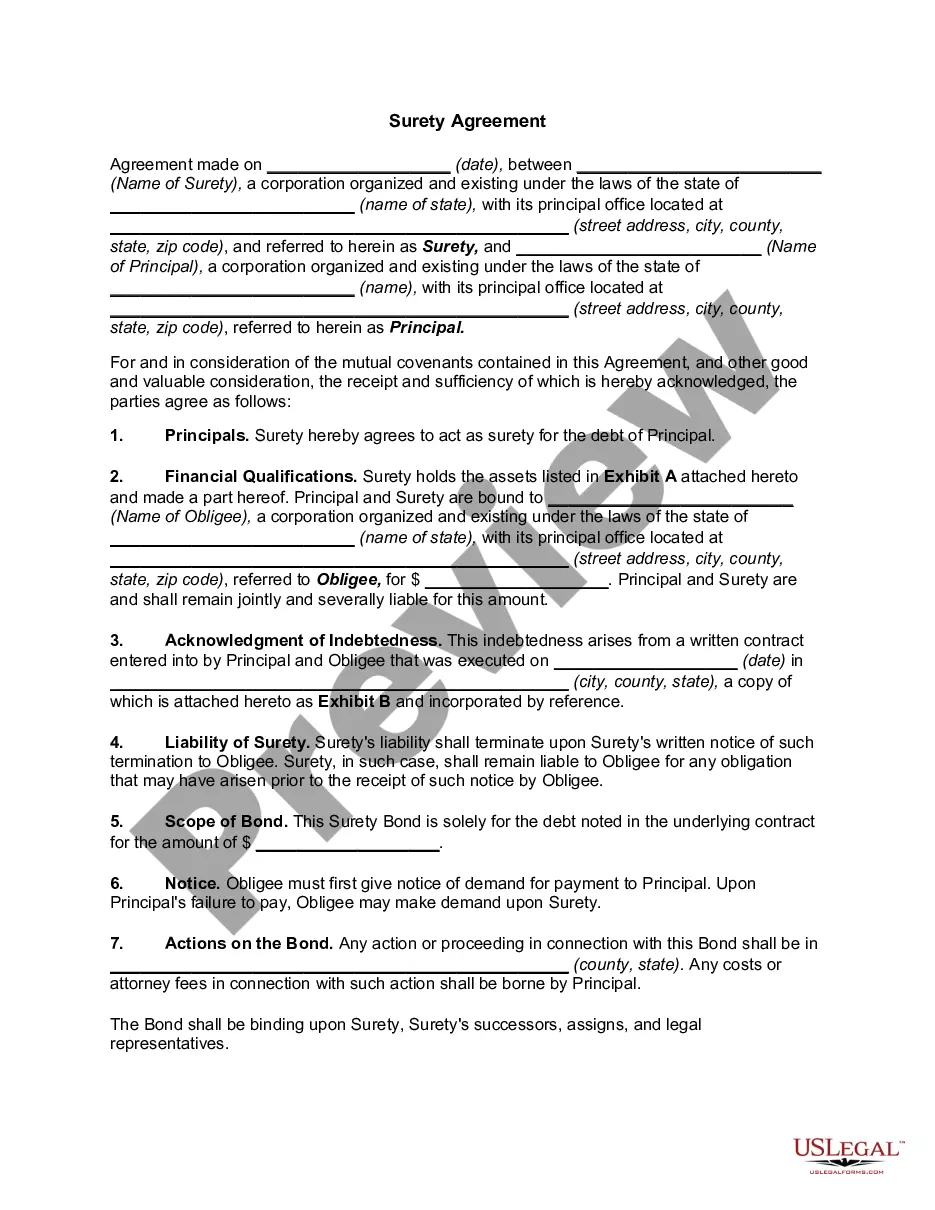

A Kentucky Surety Agreement is a legally binding contract that is commonly used in the state of Kentucky to guarantee the performance of a specific obligation. It is an agreement between three parties: the principal, the surety, and the obliged. The principal is the party who is responsible for fulfilling the obligation specified in the agreement. The surety is a third party who agrees to take responsibility for the principal's obligations if they fail to perform. The obliged is the party who is owed the performance of the obligation and who can make a claim against the surety if the principal fails to fulfill their obligations. There are several types of Kentucky Surety Agreements that can be utilized depending on the specific circumstances. Some common types include: 1. Performance Surety Agreement: This type of agreement ensures that the principal will complete a specific project or provide a particular service as per the terms outlined in a contract. It protects the obliged from financial loss in case the principal fails to perform. 2. Payment Surety Agreement: This agreement guarantees that the principal will make timely payments to subcontractors, suppliers, or vendors involved in a construction project. In the event of non-payment, the surety steps in to ensure that the payments are made. 3. Bid Bond Surety Agreement: Before a construction project begins, contractors may be required to submit a bid bond that guarantees their intent and ability to fulfill the project if awarded the contract. If they fail to do so, the surety becomes liable for any additional costs incurred in selecting another contractor. 4. License and Permit Surety Agreement: Some professions or industries in Kentucky require individuals or businesses to obtain licenses or permits. This type of surety agreement guarantees compliance with the state's laws and regulations associated with these licenses or permits. 5. Court Surety Agreement: In legal cases, a court may require a party to post a surety bond to ensure compliance with court orders or to ensure payment in cases where monetary damages are involved. This agreement protects the obliged if the party fails to meet the court's requirements. Kentucky Surety Agreements are crucial in providing financial security, ensuring contractual performance, and protecting the interests of all parties involved. It is essential to carefully review and understand the terms and conditions of the agreement before entering into one, either as a principal, surety, or obliged.

Kentucky Surety Agreement

Description

How to fill out Kentucky Surety Agreement?

You are able to invest hrs on-line attempting to find the legal document design which fits the state and federal needs you will need. US Legal Forms provides thousands of legal kinds that are analyzed by specialists. It is simple to down load or produce the Kentucky Surety Agreement from your assistance.

If you currently have a US Legal Forms accounts, you can log in and then click the Download option. Afterward, you can total, modify, produce, or signal the Kentucky Surety Agreement. Every single legal document design you purchase is the one you have eternally. To obtain an additional copy associated with a acquired form, go to the My Forms tab and then click the corresponding option.

If you work with the US Legal Forms site the first time, keep to the simple guidelines below:

- Initially, make certain you have selected the right document design to the state/town that you pick. See the form information to make sure you have picked out the right form. If readily available, use the Preview option to search through the document design at the same time.

- If you would like find an additional edition from the form, use the Research industry to find the design that suits you and needs.

- When you have discovered the design you want, just click Get now to carry on.

- Choose the rates strategy you want, type your references, and sign up for a free account on US Legal Forms.

- Complete the financial transaction. You may use your Visa or Mastercard or PayPal accounts to pay for the legal form.

- Choose the formatting from the document and down load it to the gadget.

- Make alterations to the document if needed. You are able to total, modify and signal and produce Kentucky Surety Agreement.

Download and produce thousands of document web templates while using US Legal Forms website, which provides the largest selection of legal kinds. Use skilled and status-distinct web templates to tackle your small business or person needs.

Form popularity

FAQ

Public Adjuster Surety Bond To work within the Commonwealth of Kentucky as a public adjuster, you must post a $20,000 bond as required by the KY Department of Insurance. By posting this bond, you agree to comply with applicable state law.

Someone who assumes direct liability for another's obligation. Financial creditors may require the debtor to find a surety, who then signs the loan agreement along with the debtor.

Surety Explained in Detail A surety bond is a legal binding agreement signed between three partiesthe lender, the trustee, and the guarantor. The obligee, generally a government agency, allows the principal to receive a security bond as a protection against future work output, normally a business owner or contractor.

A $50,000 surety bond is required by the Kentucky Department of Financial Institutions for all mortgage brokers doing business in the state. It gives consumers a measure of protection from fraudulent and illegal acts by compensating them in the event of wrongdoing by the broker.

The surety is the guarantee of the debts of one party by another. A surety is an organization or person that assumes the responsibility of paying the debt in case the debtor policy defaults or is unable to make the payments. The party that guarantees the debt is referred to as the surety, or as the guarantor.

A surety bond is a loan you receive to post bail. In the case of surety bond the contractor is a bail bondsman. The bail bondsman meets with you and agrees to post bail for you. The bail bondsman then contacts the surety company they work with to borrow the cash to post your bail.

A $1,000 notary bond in Kentucky can be purchased online instantly for $40 and remains in effect for 4 years. While it is not required by the state, Suretybonds.com also offers errors & omissions insurance which protects you from being held personally liable for mistakes made while notarizing documents.

These bond types are also referred to as commercial bonds" or business bonds." Examples of license and permit surety bonds include auto dealer bonds, mortgage broker bonds, and collection agency bonds.