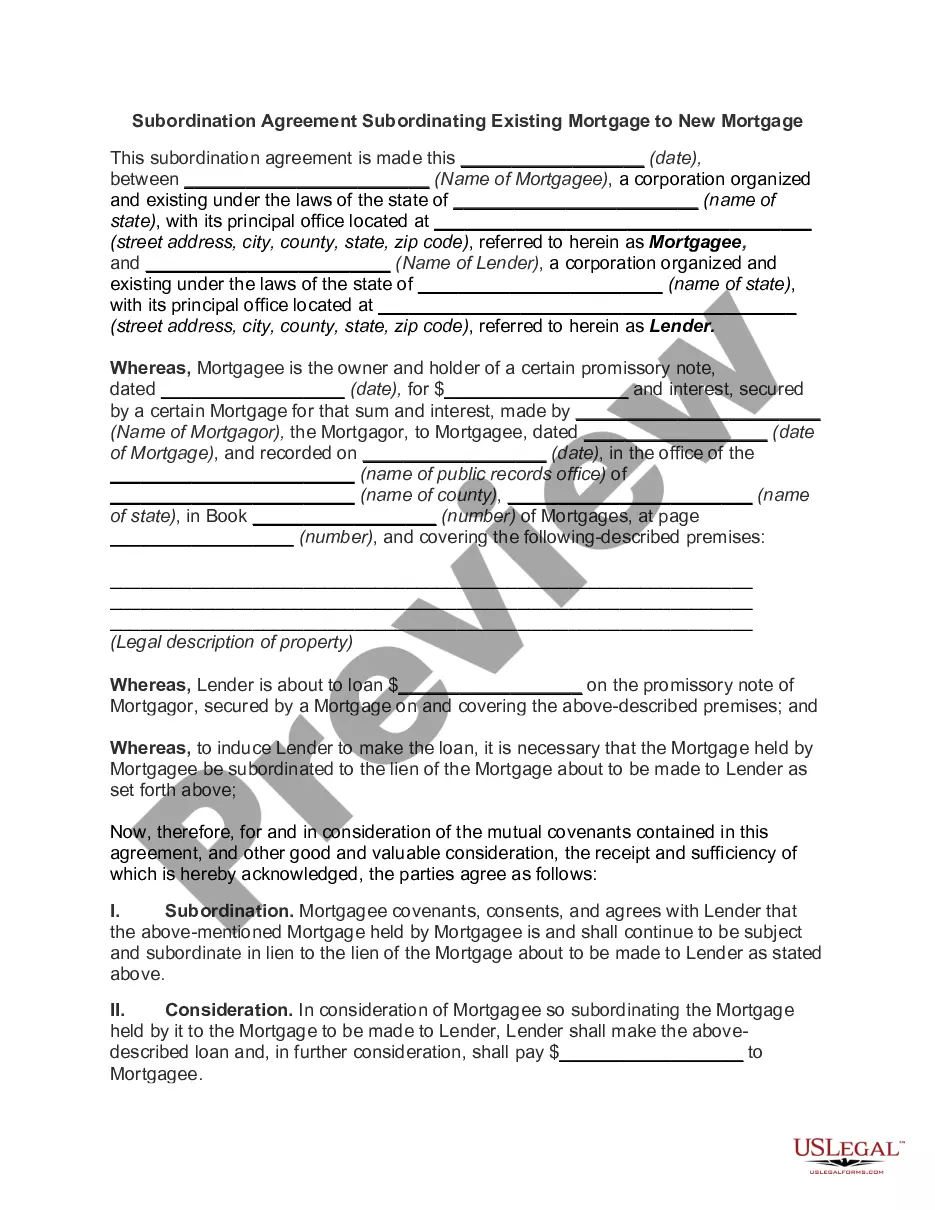

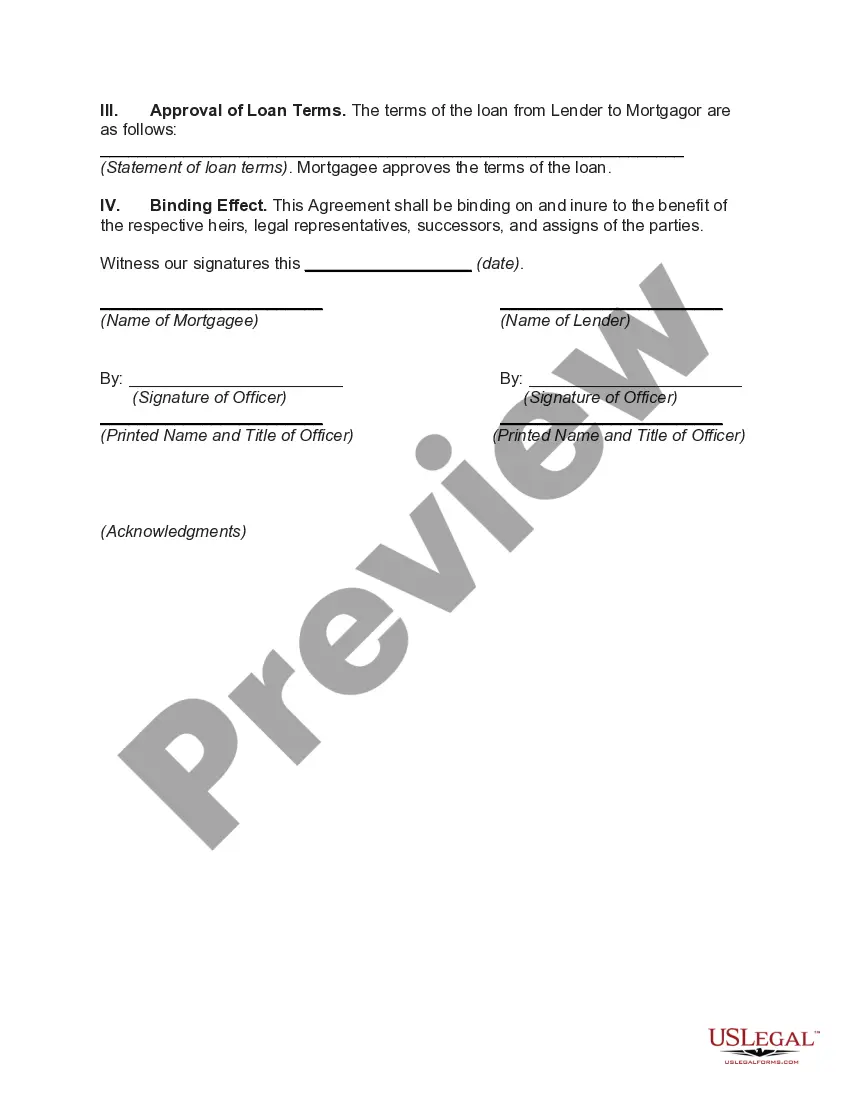

A Kentucky Subordination Agreement is a legal document that allows a property owner with an existing mortgage to obtain a new mortgage loan while retaining the priority of the original mortgage lien. By subordinating the existing mortgage to the new mortgage, the lender of the new mortgage becomes the primary lien holder, while the existing lender takes a secondary position on the property. This agreement is commonly used in situations where the property owner wants to refinance their mortgage, obtain a home equity line of credit, or finance a home improvement project. There are several types of Kentucky Subordination Agreements that can be used depending on the specific circumstances: 1. First Mortgage Subordination Agreement: In this scenario, the property owner has an existing first mortgage and wants to obtain a new first mortgage loan. The original lender agrees to subordinate their mortgage to the new lender, allowing the new lender to take the first position on the property. 2. Second Mortgage Subordination Agreement: If the property owner already has a second mortgage and wishes to obtain a new first mortgage loan, they would need a second mortgage subordination agreement. In this case, the lender of the second mortgage agrees to subordinate their lien to the new lender, allowing the new lender to become the primary lien holder. 3. Home Equity Line of Credit (HELOT) Subordination Agreement: This type of subordination agreement is used when the property owner wants to obtain a home equity line of credit while having an existing mortgage. The existing lender subordinates their lien to the HELOT lender, giving the HELOT lender priority over any future liens. 4. Construction Loan Subordination Agreement: When a property owner wants to finance a new construction project on a property with an existing mortgage, a construction loan subordination agreement is necessary. This agreement allows the construction loan lender to hold the primary lien position while the existing lender becomes subordinate during the construction period. Kentucky Subordination Agreements must be drafted carefully, taking into consideration the interests of both the existing lender and the new lender. It is important to consult with a qualified attorney or mortgage professional to ensure that all parties involved are protected and that the agreement complies with Kentucky state laws and regulations. Subordination agreements are typically recorded in the county land records to provide public notice of the lien priorities on a property.

Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Kentucky Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Choosing the right lawful record format could be a struggle. Obviously, there are a lot of layouts available online, but how can you discover the lawful kind you need? Use the US Legal Forms web site. The service offers a large number of layouts, including the Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage, that can be used for enterprise and personal requires. All of the kinds are checked out by experts and meet state and federal demands.

In case you are previously authorized, log in to your bank account and click the Acquire switch to have the Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Make use of your bank account to look through the lawful kinds you may have purchased formerly. Proceed to the My Forms tab of your bank account and acquire another copy in the record you need.

In case you are a fresh user of US Legal Forms, listed here are simple recommendations that you can stick to:

- Very first, ensure you have selected the proper kind for the city/state. You can look through the form utilizing the Preview switch and look at the form explanation to make certain it will be the right one for you.

- When the kind is not going to meet your preferences, utilize the Seach industry to get the right kind.

- When you are certain that the form is suitable, go through the Get now switch to have the kind.

- Select the costs program you need and enter in the essential information and facts. Design your bank account and pay money for the order with your PayPal bank account or credit card.

- Select the submit formatting and download the lawful record format to your product.

- Comprehensive, edit and printing and indicator the obtained Kentucky Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms will be the greatest library of lawful kinds in which you can see different record layouts. Use the company to download skillfully-manufactured paperwork that stick to express demands.