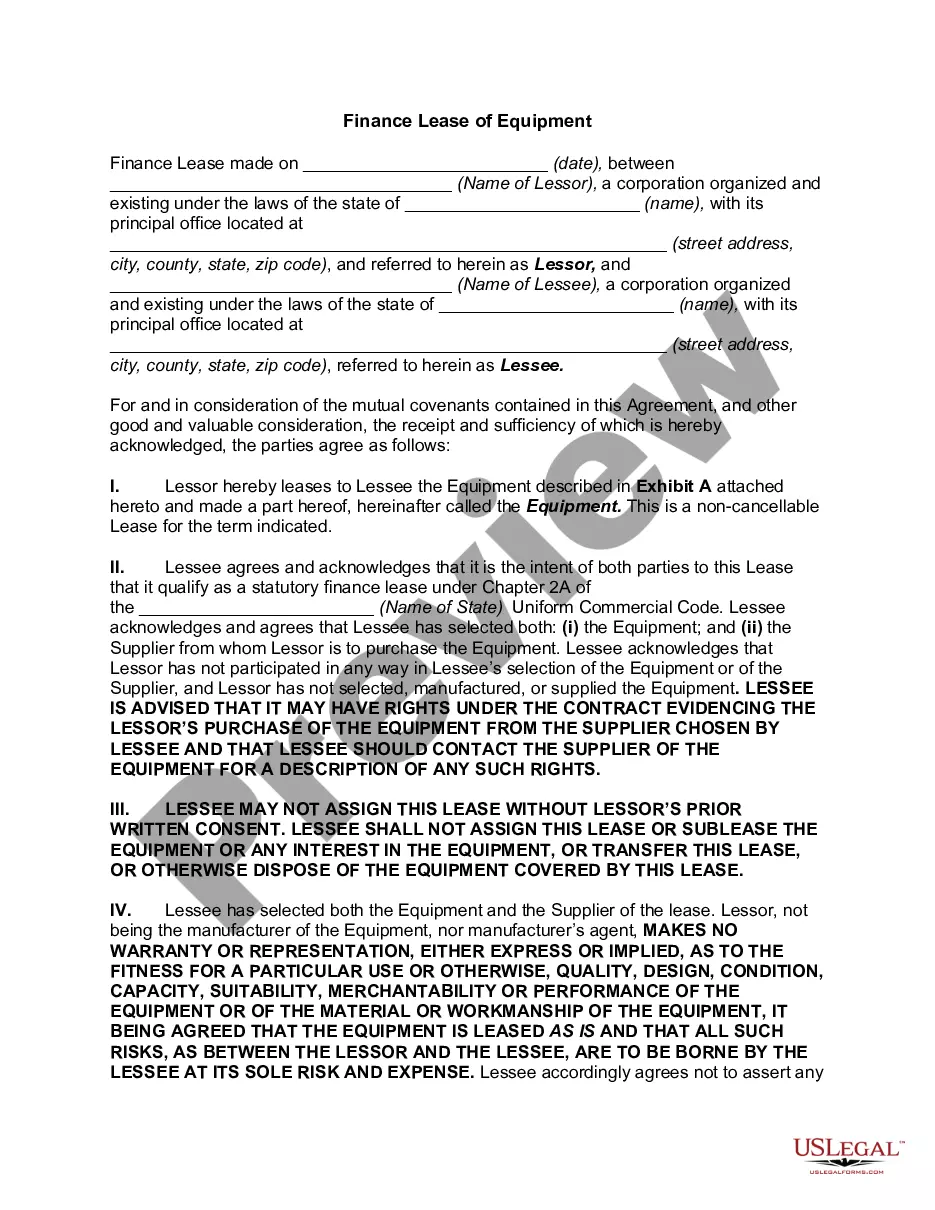

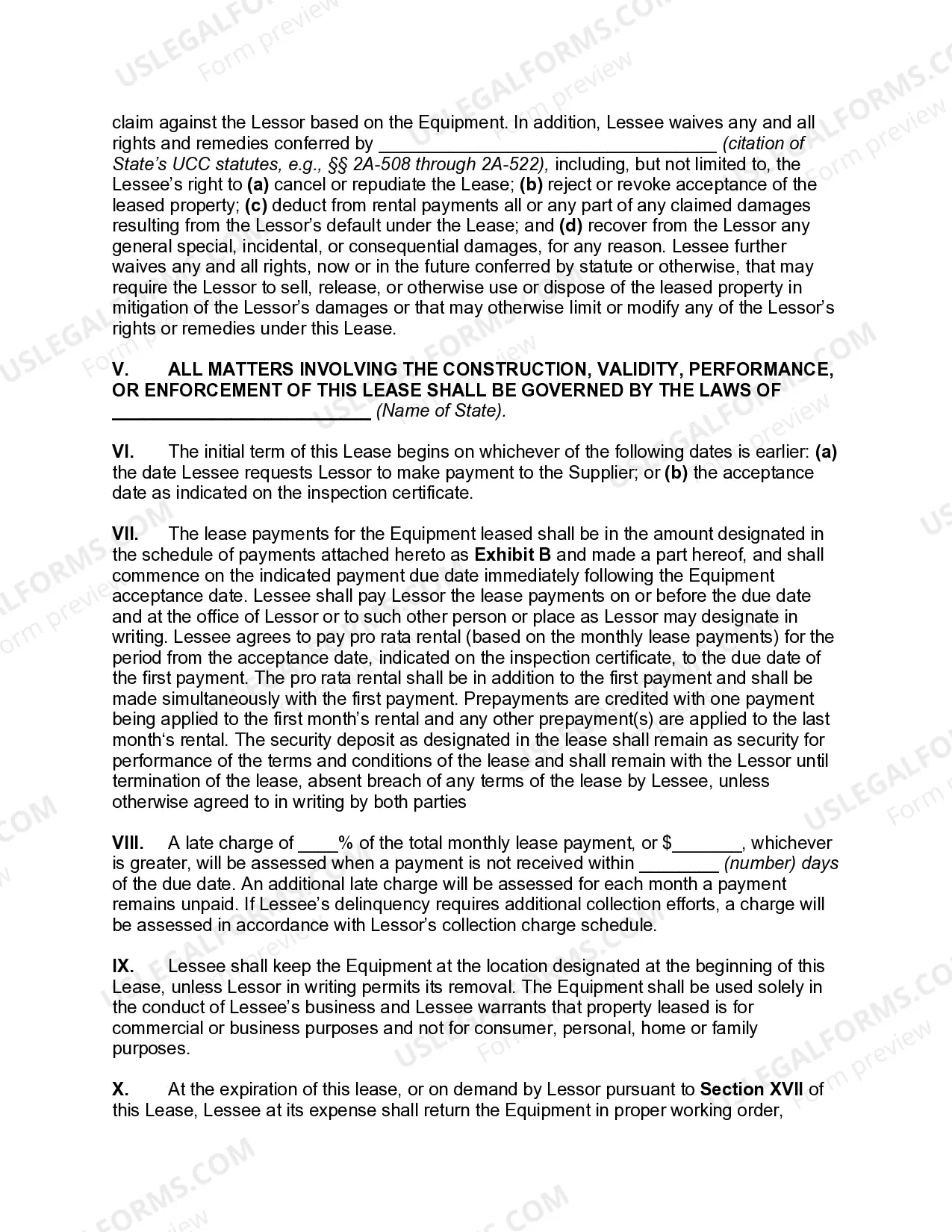

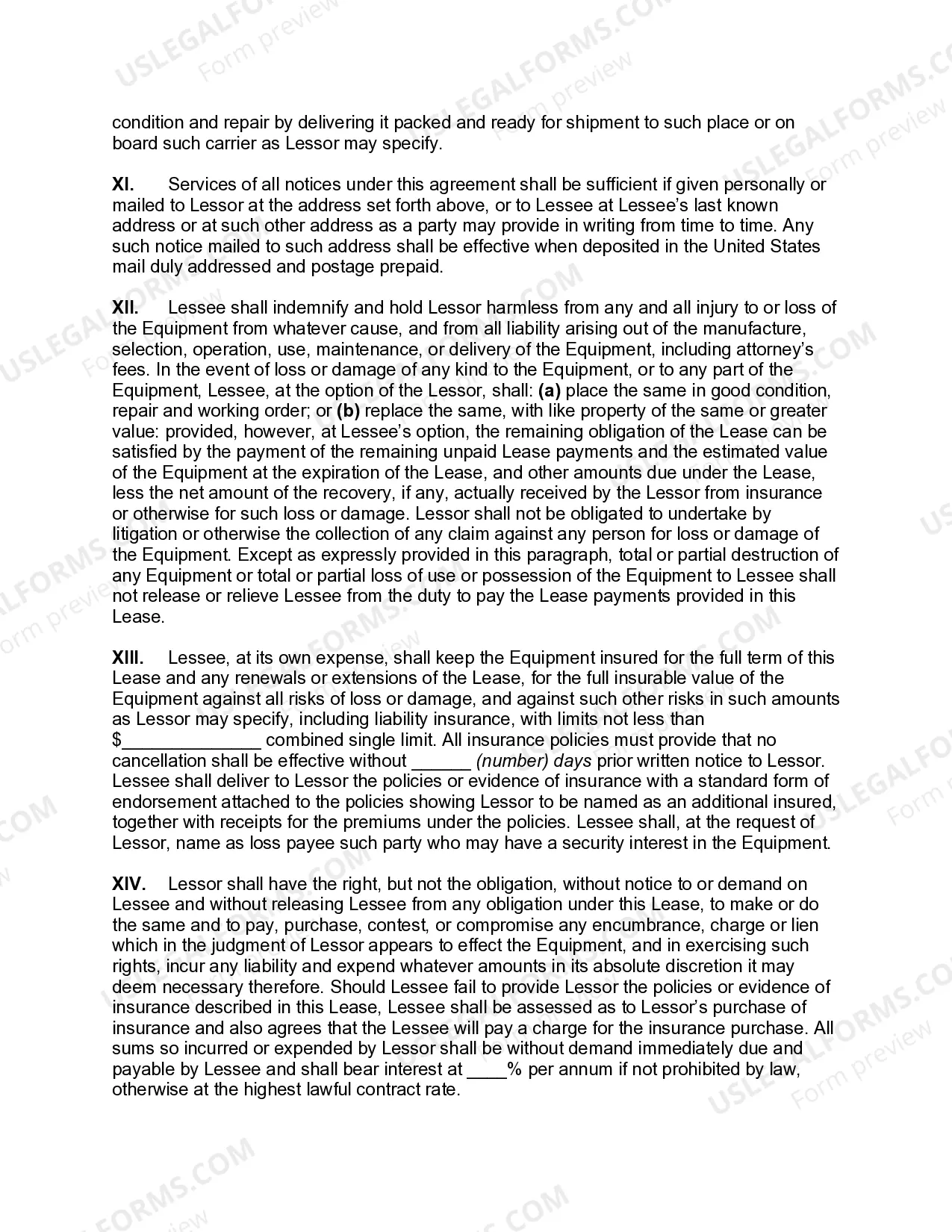

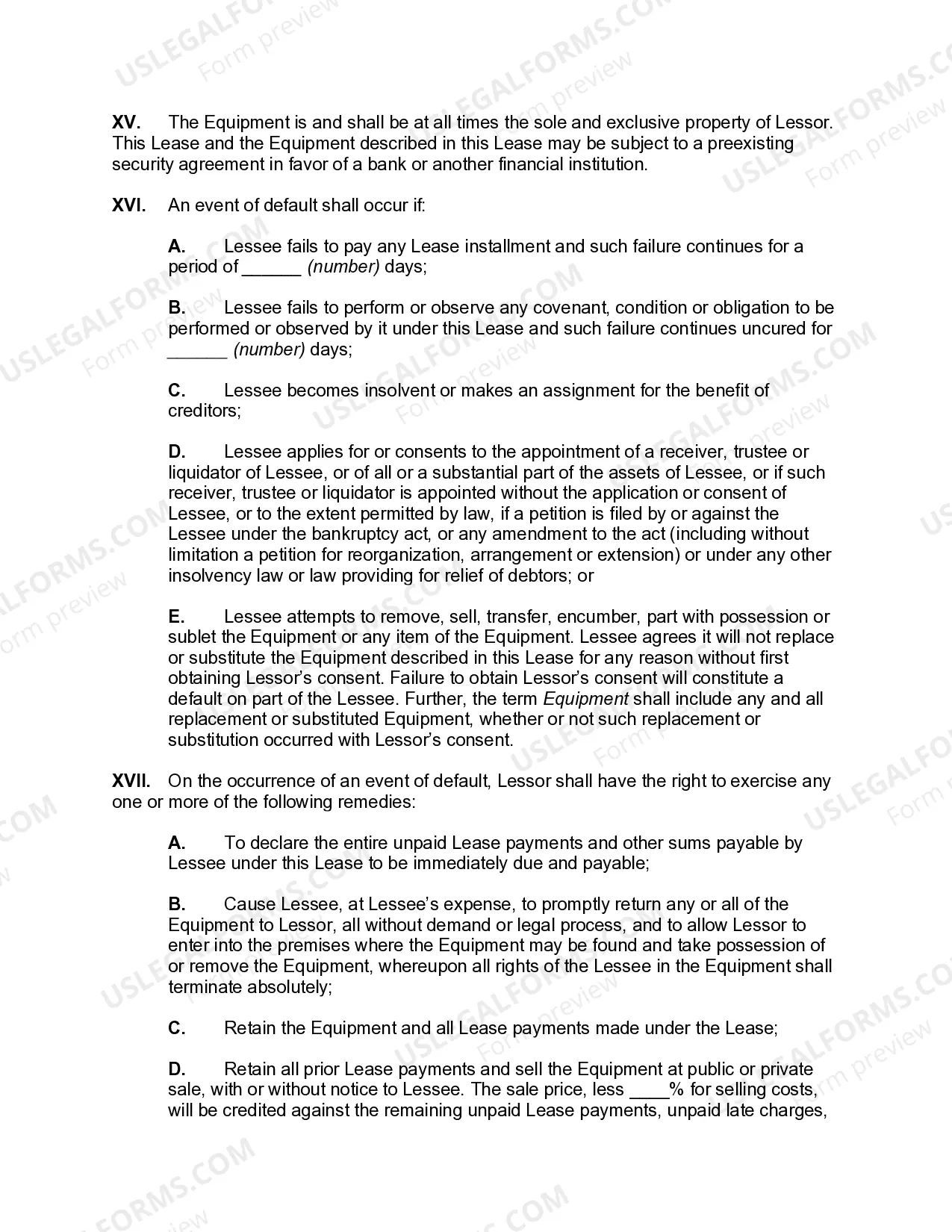

Kentucky Finance Lease of Equipment refers to a financial agreement wherein a business entity within the state of Kentucky leases equipment from a financial institution or leasing company. This type of lease allows businesses to acquire essential equipment without incurring the higher costs associated with purchasing it outright. The lessor, which can be a bank, finance company, or independent leasing company, purchases the equipment and leases it to the lessee (business) for a fixed period, generally ranging from one to five years. The Kentucky Finance Lease of Equipment provides several benefits for businesses. Firstly, it allows businesses to conserve their working capital as they are not required to make a significant upfront investment in purchasing the equipment. Instead, they make regular lease payments according to the terms of the lease agreement. This allows businesses to allocate their funds towards other critical operational expenses, such as payroll, inventory, and marketing. Moreover, the lease term is usually structured to match the equipment's expected useful life, ensuring that the lessee can fully utilize it without the burden of ownership. At the end of the lease term, businesses may have the option to renew the lease, upgrade to newer equipment models, or return the equipment to the lessor. There are various types of Kentucky Finance Lease of Equipment available to businesses, depending on their specific needs and industry requirements. These types may include: 1. Capital Lease: This type of lease is used when the lessee intends to acquire ownership of the equipment at the end of the lease term or wishes to finance a substantial portion of the equipment's cost. In a capital lease, the equipment is considered an asset on the lessee's balance sheet. 2. Operating Lease: An operating lease is suitable when the lessee intends to use the equipment for a short-term period or does not want to take ownership of the equipment. In this case, the lease payments are treated as operational expenses and the equipment does not appear on the lessee's balance sheet. 3. Sale and Leaseback: This arrangement allows businesses to sell their owned equipment to a lessor and then lease it back. It provides immediate cash flow to the business while still retaining the use of the equipment. 4. Municipal Lease: This type of lease is specific to government entities or municipalities within Kentucky. It allows them to lease equipment for their public service needs, such as police vehicles or fire trucks, without bearing the financial burden of outright purchases. In summary, Kentucky Finance Lease of Equipment offers businesses within the state a flexible and cost-effective solution to acquire necessary equipment. By utilizing various lease types, businesses can optimize their financing strategy and efficiently manage their equipment needs, irrespective of whether they prefer ownership or want to focus on operational utilization.

Kentucky Finance Lease of Equipment

Description

How to fill out Kentucky Finance Lease Of Equipment?

You may spend hours on-line trying to find the lawful papers design that suits the state and federal requirements you need. US Legal Forms offers a large number of lawful varieties that happen to be reviewed by professionals. You can actually acquire or print the Kentucky Finance Lease of Equipment from your service.

If you already possess a US Legal Forms account, you may log in and click on the Down load key. Next, you may total, modify, print, or sign the Kentucky Finance Lease of Equipment. Each lawful papers design you get is your own property permanently. To have another duplicate of the obtained develop, visit the My Forms tab and click on the corresponding key.

Should you use the US Legal Forms internet site initially, stick to the easy instructions beneath:

- Initial, make certain you have chosen the correct papers design for the state/town of your choosing. Read the develop outline to make sure you have picked the appropriate develop. If available, make use of the Review key to appear through the papers design too.

- If you want to get another variation from the develop, make use of the Search area to find the design that meets your requirements and requirements.

- After you have discovered the design you need, just click Purchase now to proceed.

- Select the prices program you need, enter your references, and register for a merchant account on US Legal Forms.

- Total the financial transaction. You can use your charge card or PayPal account to pay for the lawful develop.

- Select the file format from the papers and acquire it to the device.

- Make adjustments to the papers if required. You may total, modify and sign and print Kentucky Finance Lease of Equipment.

Down load and print a large number of papers themes using the US Legal Forms web site, which offers the greatest collection of lawful varieties. Use specialist and express-particular themes to tackle your business or specific requires.

Form popularity

FAQ

Standard rates come in around 7%-9% for good credit on leases under $100,000. Rates between 9%-13% are common from less competitive lessors, or if you are dealing with bad credit.

Interest expense for a finance lease. In the context of lease accounting, interest is paid by a lessee to a lessor for the right to use a particular leased asset and pay for it over time. Conversely, interest will be received by a lessor from the lessee for the use of the same asset.

A capital lease (or finance lease) is an agreement where the lessor has agreed that the ownership of the asset will be transferred to the lessee when the lease period is over. It allows the lessee the choice of buying the asset at a bargain price that is lower than the market value at the end of the lease period.

When you lease equipment, the lessor is effectively putting up a lump sum of money on your behalf, which you will pay off with interest over time. The effective interest rate on a lease can be anywhere from the low single digits to more than 30%, with the average is around 6% to16%.

Leasing works like a rental agreement. You pay the equipment's owner a set fee every agreed period and you can use the asset as though it was your own. Under a lease, nobody else can use the equipment without your permission and for all intents and purposes, it's as though you own the piece of equipment.

A lease will always have at least two parties: the lessor and the lessee. The lessor is the person or business that owns the equipment. The lessee is the person or business renting the equipment. The lessee will make payments to the lessor throughout the contract.

A finance lease (also known as a capital lease or a sales lease) is a type of lease in which a finance company is typically the legal owner of the asset for the duration of the lease, while the lessee not only has operating control over the asset, but also some share of the economic risks and returns from the change in

Equipment leasing is a type of financing in which you rent equipment rather than purchase it outright. You can lease expensive equipment for your business, such as machinery, vehicles or computers.

A finance lease is a contract between a lessor (a funder or finance company) and a lessee (your business), where the lessee requires the use of business equipment, vehicles, or machinery. The lessor provides the use of such equipment in exchange for pre-agreed regular payments.

With an equipment lease, the equipment isn't yours to keep once the leasing term is over. As with a business loan, you pay interest and fees when leasing equipment and they're usually added into the monthly payment.