the remaining partners of a business partnership.

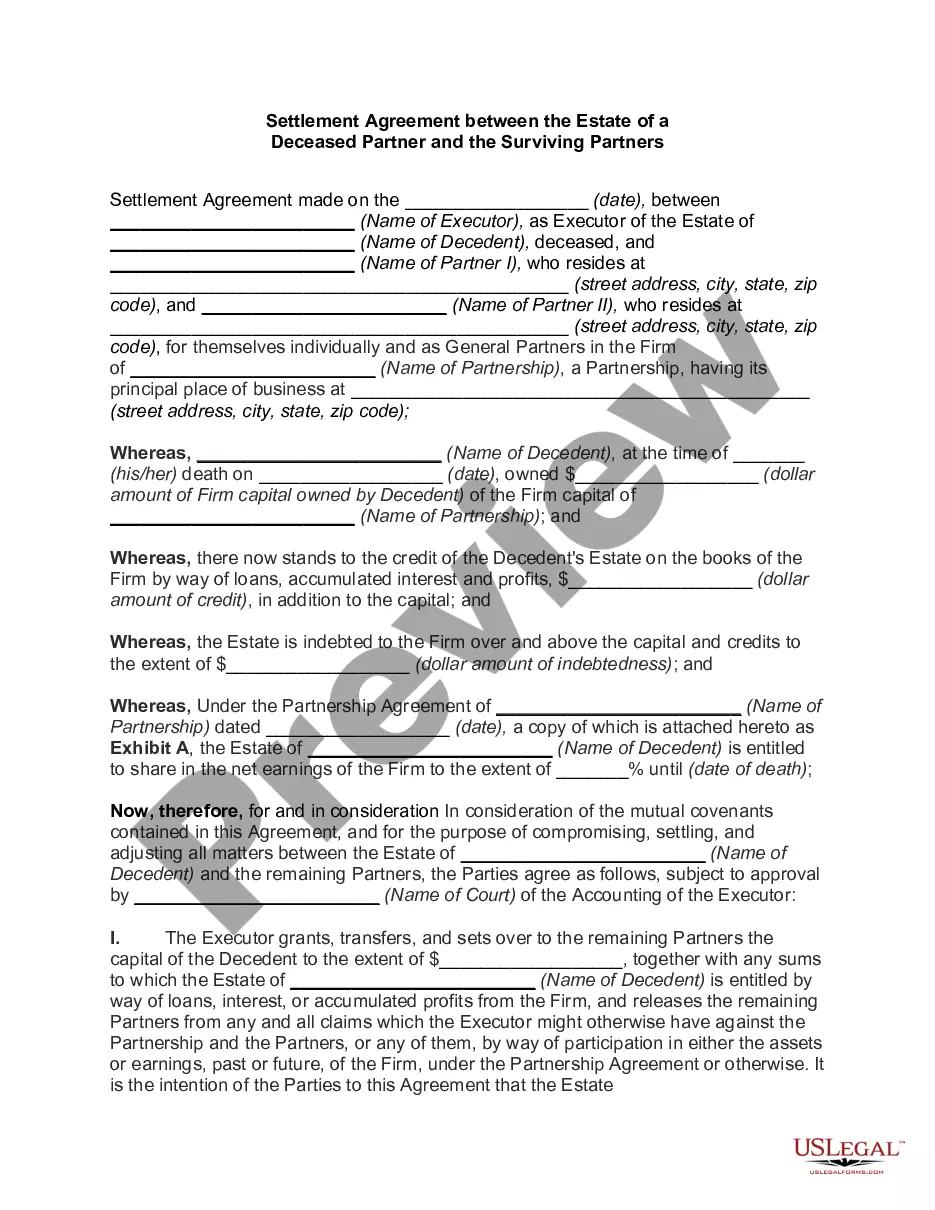

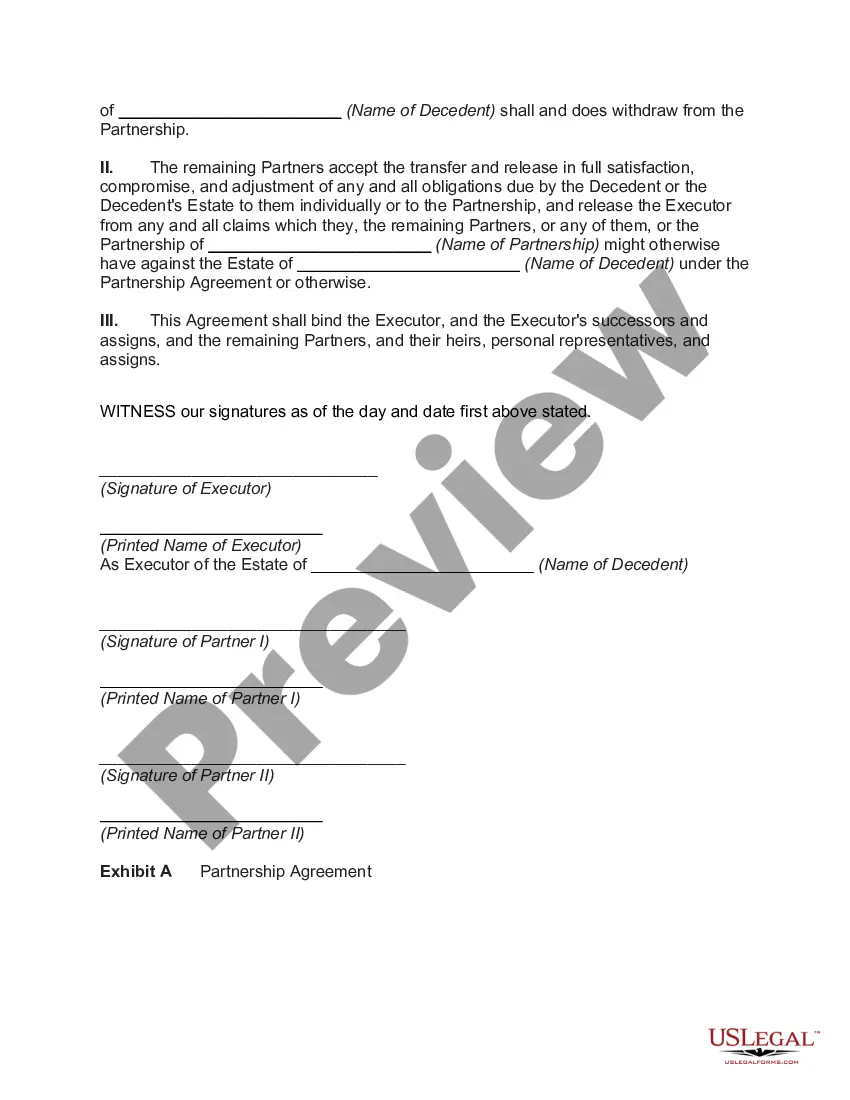

A Kentucky Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners is a legal contract that seeks to resolve the various issues and obligations arising from the death of a partner in a business or partnership. This agreement outlines the terms and conditions under which the deceased partner's estate will be handled, including the distribution of assets, liabilities, and the continuation or dissolution of the partnership. The Estate Settlement Agreement is crucial in providing a clear framework for the estate administration process and the smooth transition of the deceased partner's interests. It aims to ensure fairness, protect the rights of both the estate and the surviving partners, and prevent potential disputes or conflicts that may arise in such circumstances. Some of the key elements that should be addressed in a Kentucky Settlement Agreement include: 1. Asset Distribution: The agreement should outline how the deceased partner's assets will be distributed, including business interests, real estate, investments, and any personal belongings. It may specify that the estate's assets will be distributed in accordance with a will, trust, or state laws of intestacy if the deceased partner did not leave a valid will. 2. Business Valuation: In cases where the partnership will continue operating, the settlement agreement should include provisions for valuing the business interests of the deceased partner. This process ensures that the surviving partners compensate the estate fairly for the deceased partner's ownership stake. 3. Buyout or Continuation of Partnership: The agreement may provide for the surviving partners to buy out the deceased partner's share in the business. Alternatively, it can outline the terms and conditions under which the partnership will continue, such as admitting a representative of the estate as a replacement partner or transferring the deceased partner's shares to a designated heir. 4. Liability Allocation: The settlement agreement should address how the liabilities of the partnership will be allocated, ensuring that the estate is not unduly burdened with outstanding debts or obligations. It may specify that the estate only assumes liabilities up to the value of assets received or that the surviving partners assume all outstanding obligations. 5. Insurance and Benefits: If the partnership had insurance policies or benefits that covered the deceased partner, the agreement should detail the process of receiving insurance proceeds and other entitled benefits, ensuring they are appropriately directed to the estate or other designated beneficiaries. 6. Confidentiality and Non-Disclosure: Confidentiality provisions can be included to prevent the disclosure of sensitive business information or personal details of the partners during or after the settlement process. Types of Kentucky Settlement Agreements between the Estate of a Deceased Partner and the Surviving Partners can vary based on the specific circumstances and intentions of the parties involved. Some common types may include a Buy-Sell Agreement, Partnership Dissolution Agreement, or an Agreement for Partnership Continuation with a designated representative of the estate. In conclusion, a Kentucky Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners plays a critical role in managing the legal, financial, and operational aspects following the death of a partner. It ensures a fair distribution of assets and liabilities and provides a roadmap for the continuation or dissolution of the partnership to ensure a smooth transition and minimize potential conflicts.