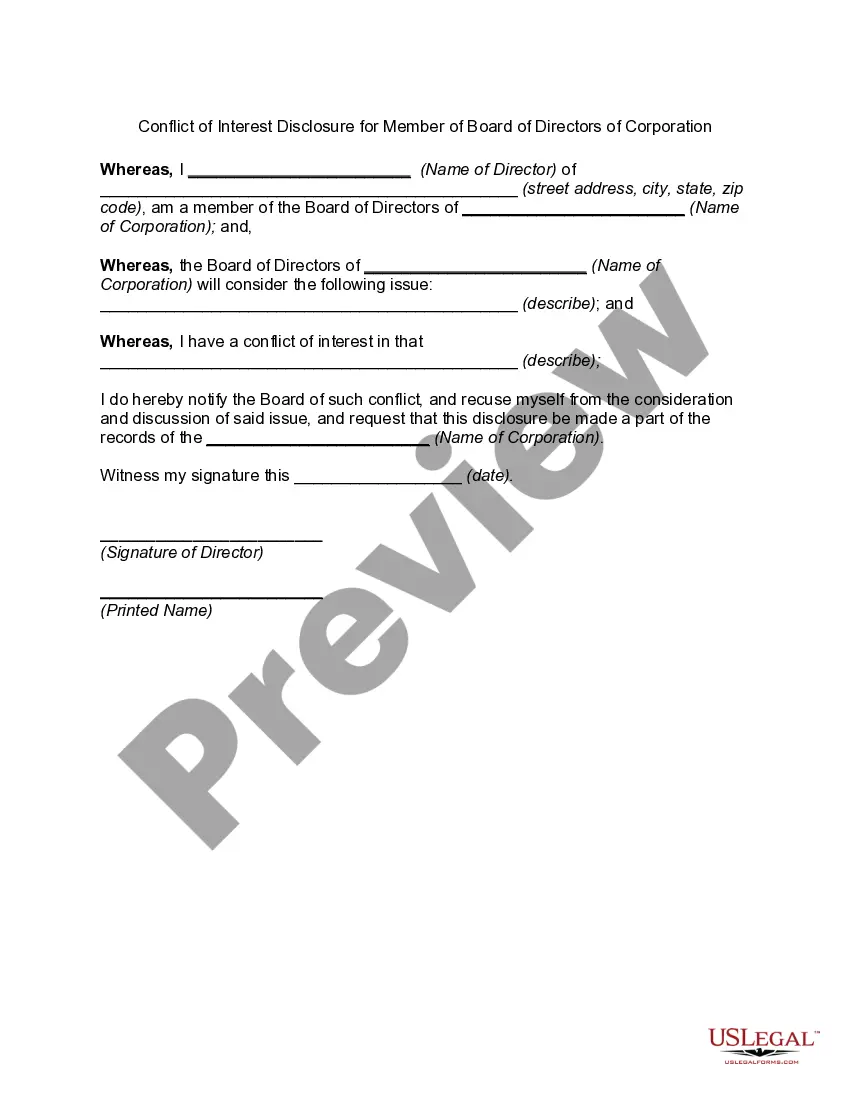

Kentucky Conflict of Interest Disclosure for Member of Board of Directors of Corporation: The Kentucky Conflict of Interest Disclosure for Members of the Board of Directors of a Corporation is a formal process that requires board members to disclose any conflicts of interest that may arise during the course of their service. In Kentucky, board members have a fiduciary duty to act in the best interest of the corporation and its shareholders. This means they must avoid any situations where their personal or financial interests could potentially conflict with the interests of the corporation. The conflict of interest disclosure process helps to ensure transparency and protect the integrity of the corporation. By requiring board members to disclose any potential conflicts, it allows the board and its shareholders to make informed decisions and mitigate the risks associated with conflicts of interest. Key elements of the Kentucky Conflict of Interest Disclosure for Members of the Board of Directors may include: 1. Written Disclosure: Board members are typically required to provide a written disclosure of any potential conflicts of interest they have or anticipate arising. This may include financial or ownership interests in competing businesses, relationships with suppliers or vendors, or any personal interests that could influence their decision-making. 2. Timely and Regular Updates: The disclosure should be made on a regular basis, such as annually or whenever a new conflict arises. This ensures that the board and its stakeholders are kept informed about any changes in circumstances that may affect the board member's ability to act objectively. 3. Review and Evaluation: Once the disclosure is made, the board and its designated committee should review and evaluate the disclosed conflicts. They should consider the potential impact of these conflicts on the board member's ability to fulfill their fiduciary duty and act in the best interest of the corporation. 4. Refusal and Mitigation Measures: In cases where a significant conflict of interest is identified, the board member may be required to recuse themselves from certain discussions or decisions. Alternatively, mitigation measures such as implementing safeguards, seeking external opinions, or assigning an independent advisor may be necessary to ensure fair and unbiased decision-making. Different types of Kentucky Conflict of Interest Disclosure for Members of the Board of Directors may include specific disclosures for: 1. Financial Interests: Board members may be required to disclose any direct or indirect financial interests they have in the corporation or any competing businesses. 2. Corporate Opportunities: Directors need to disclose any opportunities presented to them that may be beneficial to the corporation, but which they have pursued personally or with another entity. 3. Conflicts arising from Relationships: Board members must disclose any personal, professional, or familial relationships that could potentially influence their decision-making or create conflicts of interest. 4. Outside Directorships: If a board member serves on the board of another corporation or organization that has a relationship with the corporation they are serving, such as a customer or vendor, this too should be disclosed. It is important for board members to comply with the Kentucky Conflict of Interest Disclosure requirements and act in the best interest of the corporation to maintain integrity, transparency, and good governance practices.

Kentucky Conflict of Interest Disclosure for Member of Board of Directors of Corporation

Description

How to fill out Kentucky Conflict Of Interest Disclosure For Member Of Board Of Directors Of Corporation?

Discovering the right legitimate papers format could be a struggle. Of course, there are tons of themes available online, but how do you find the legitimate develop you will need? Take advantage of the US Legal Forms web site. The support delivers 1000s of themes, like the Kentucky Conflict of Interest Disclosure for Member of Board of Directors of Corporation, that can be used for company and personal requirements. Every one of the forms are inspected by experts and meet state and federal specifications.

In case you are previously registered, log in for your profile and click on the Obtain key to get the Kentucky Conflict of Interest Disclosure for Member of Board of Directors of Corporation. Make use of profile to appear through the legitimate forms you might have acquired formerly. Proceed to the My Forms tab of the profile and have an additional backup from the papers you will need.

In case you are a brand new end user of US Legal Forms, allow me to share basic guidelines that you should comply with:

- Very first, make certain you have chosen the proper develop for your personal town/area. You can look through the form using the Review key and browse the form outline to make sure it is the best for you.

- If the develop will not meet your requirements, use the Seach field to discover the proper develop.

- Once you are certain that the form is acceptable, click the Purchase now key to get the develop.

- Choose the prices program you would like and type in the required info. Build your profile and purchase your order utilizing your PayPal profile or credit card.

- Select the submit file format and download the legitimate papers format for your gadget.

- Comprehensive, change and printing and indication the received Kentucky Conflict of Interest Disclosure for Member of Board of Directors of Corporation.

US Legal Forms will be the most significant collection of legitimate forms that you can see various papers themes. Take advantage of the service to download professionally-manufactured papers that comply with condition specifications.