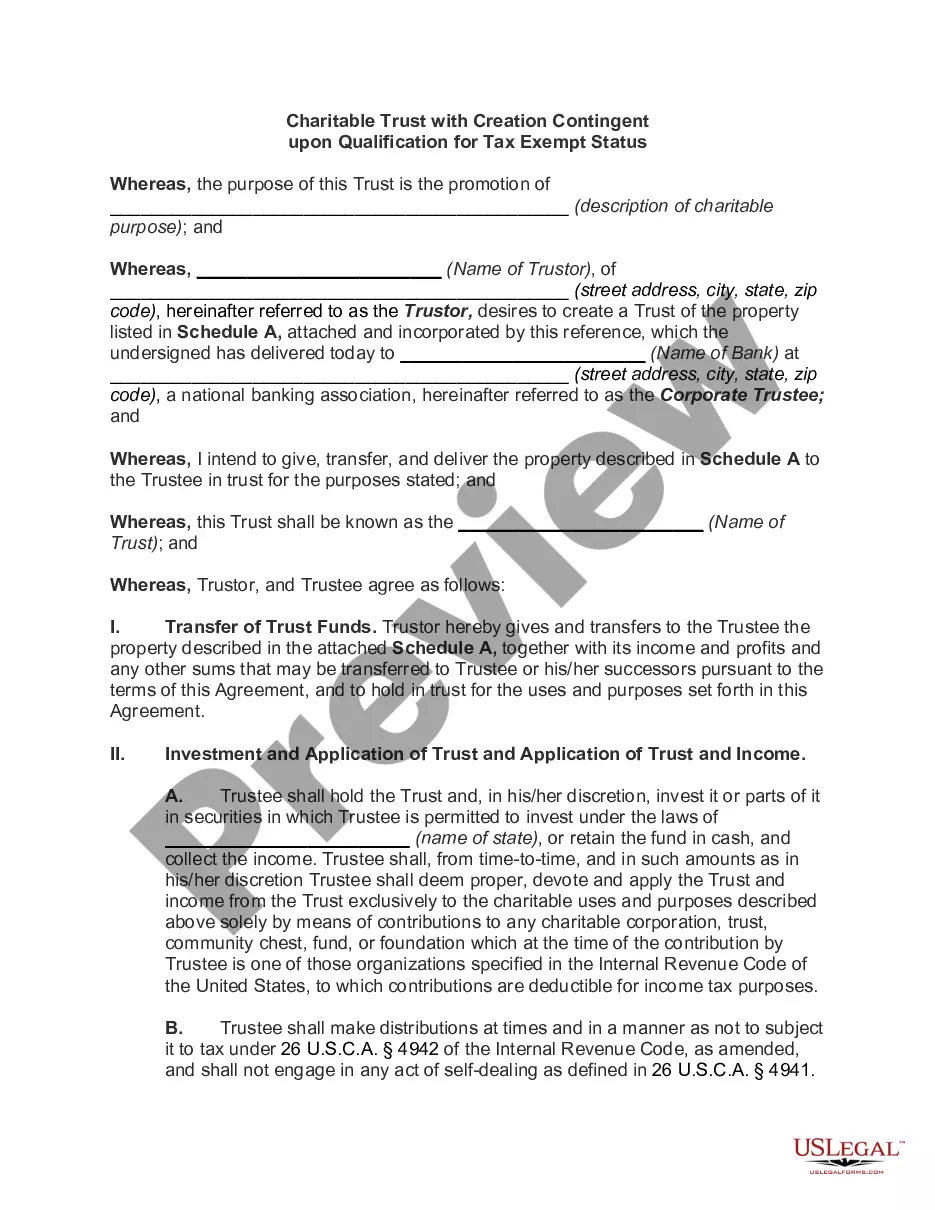

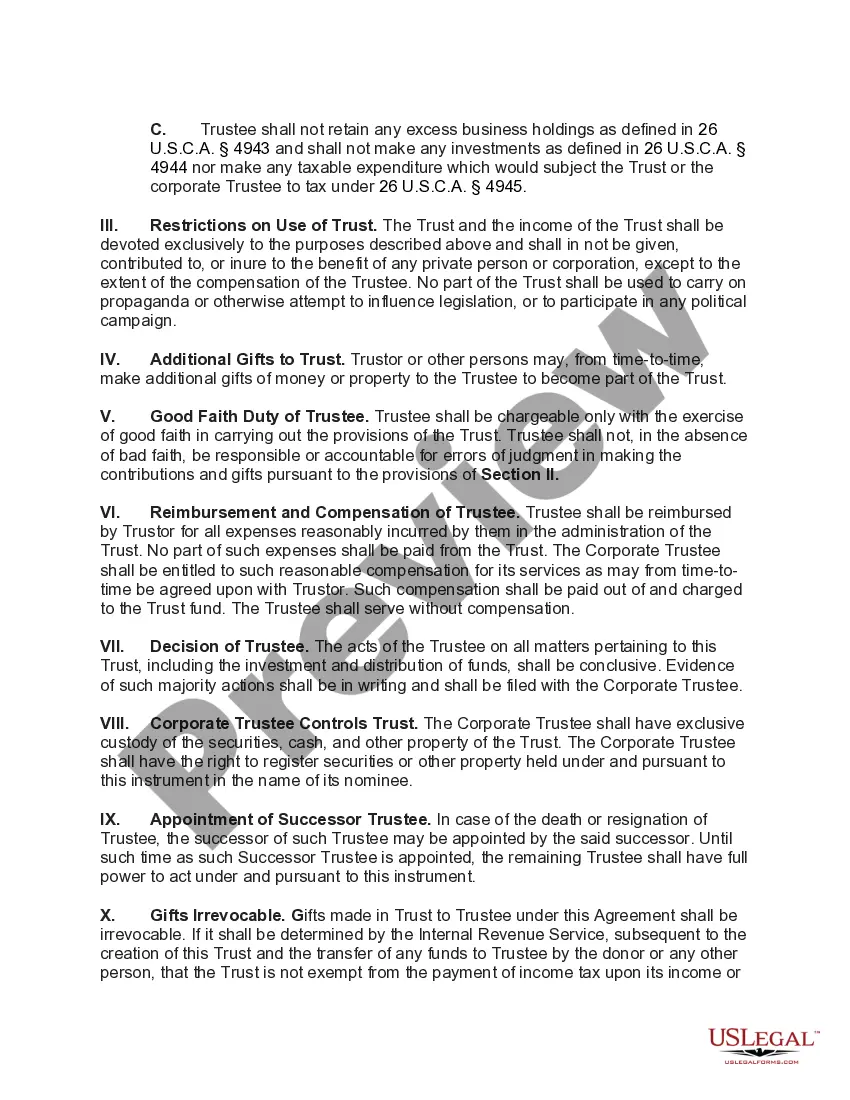

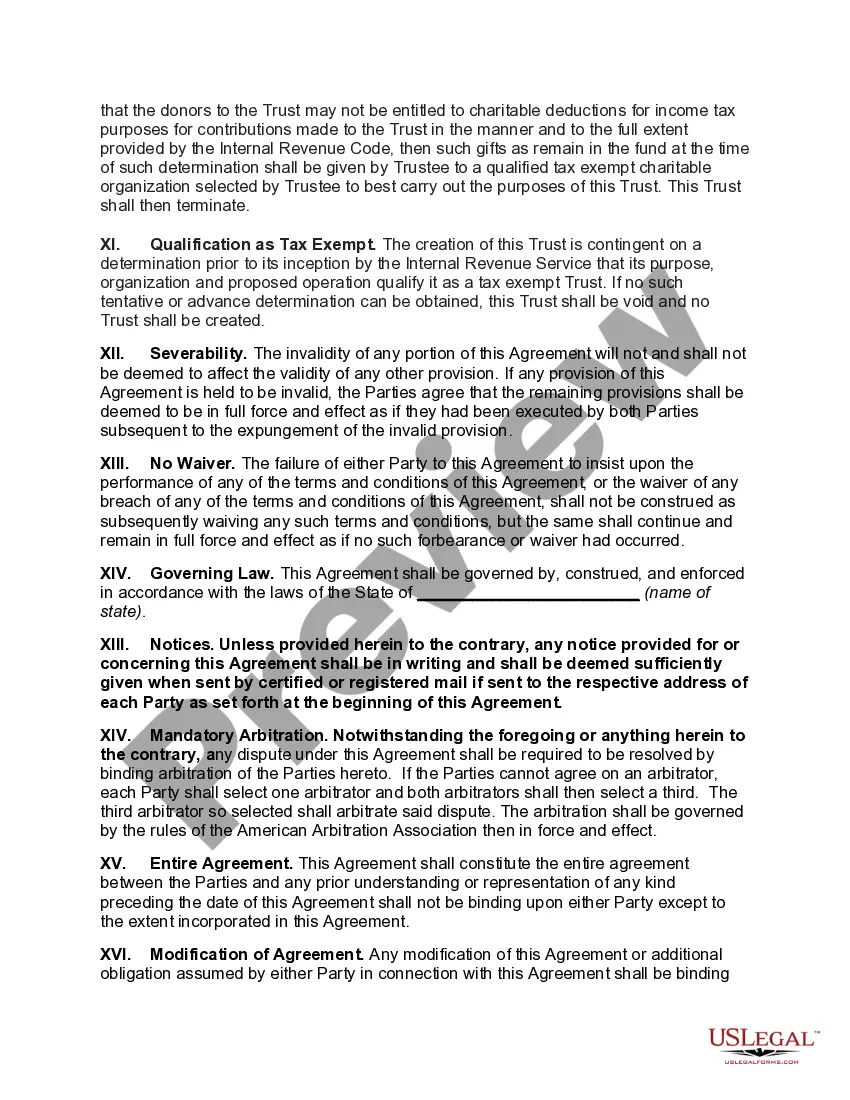

Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status refers to a specific type of trust established in the state of Kentucky that is dependent on obtaining tax-exempt status from the Internal Revenue Service (IRS). This trust is designed to support charitable causes and organizations while providing potential tax benefits to the trust creator or beneficiaries. By qualifying for tax-exempt status, the trust can enjoy certain tax advantages, such as exemption from income tax on trust earnings and potential deductions for charitable contributions. The Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status can be established in various forms, including: 1. Inter vivos Charitable Trust: This type of trust is created during the lifetime of the trust or and can become tax-exempt upon qualification by meeting the necessary criteria set forth by the IRS. 2. Testamentary Charitable Trust: Established through a will or testament, this trust takes effect after the trust or's death. Similar to an inter vivos trust, it must qualify for tax-exempt status to enjoy the associated tax benefits. 3. Charitable Remainder Trust: This trust allows the trust or to retain an income stream from the assets placed into the trust while also providing for the eventual distribution of remaining assets to a charitable organization. To be eligible for tax-exempt status, specific requirements must be met. 4. Charitable Lead Trust: In this type of trust, the income generated from the trust assets is initially directed to a charitable cause or organization, with the remaining assets eventually passing to non-charitable beneficiaries. Qualifying for tax-exempt status is crucial to optimize tax benefits. It's important for individuals or entities considering the establishment of a Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status to consult with an experienced attorney or tax professional. This ensures compliance with relevant laws, proper qualification for tax-exempt status, and the effective administration of the trust in alignment with their charitable objectives.

Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status

Description

How to fill out Kentucky Charitable Trust With Creation Contingent Upon Qualification For Tax Exempt Status?

US Legal Forms - among the biggest libraries of legal varieties in the USA - gives a wide range of legal record templates you can acquire or print out. Using the web site, you may get a large number of varieties for company and individual reasons, categorized by groups, claims, or key phrases.You can get the newest versions of varieties just like the Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status within minutes.

If you currently have a registration, log in and acquire Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status through the US Legal Forms local library. The Acquire key will appear on every single kind you see. You get access to all previously saved varieties inside the My Forms tab of your respective profile.

If you wish to use US Legal Forms initially, listed below are basic directions to obtain started out:

- Make sure you have selected the correct kind for your metropolis/area. Select the Preview key to examine the form`s information. Browse the kind outline to ensure that you have selected the proper kind.

- If the kind does not match your demands, use the Lookup discipline on top of the monitor to get the one which does.

- In case you are satisfied with the shape, validate your choice by clicking on the Get now key. Then, pick the costs plan you prefer and supply your accreditations to sign up for the profile.

- Approach the financial transaction. Use your Visa or Mastercard or PayPal profile to complete the financial transaction.

- Select the structure and acquire the shape on your gadget.

- Make modifications. Fill up, change and print out and indication the saved Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status.

Each and every format you put into your bank account does not have an expiry date and is your own property forever. So, if you want to acquire or print out yet another backup, just visit the My Forms section and click on on the kind you want.

Obtain access to the Kentucky Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status with US Legal Forms, probably the most comprehensive local library of legal record templates. Use a large number of professional and state-certain templates that satisfy your business or individual demands and demands.