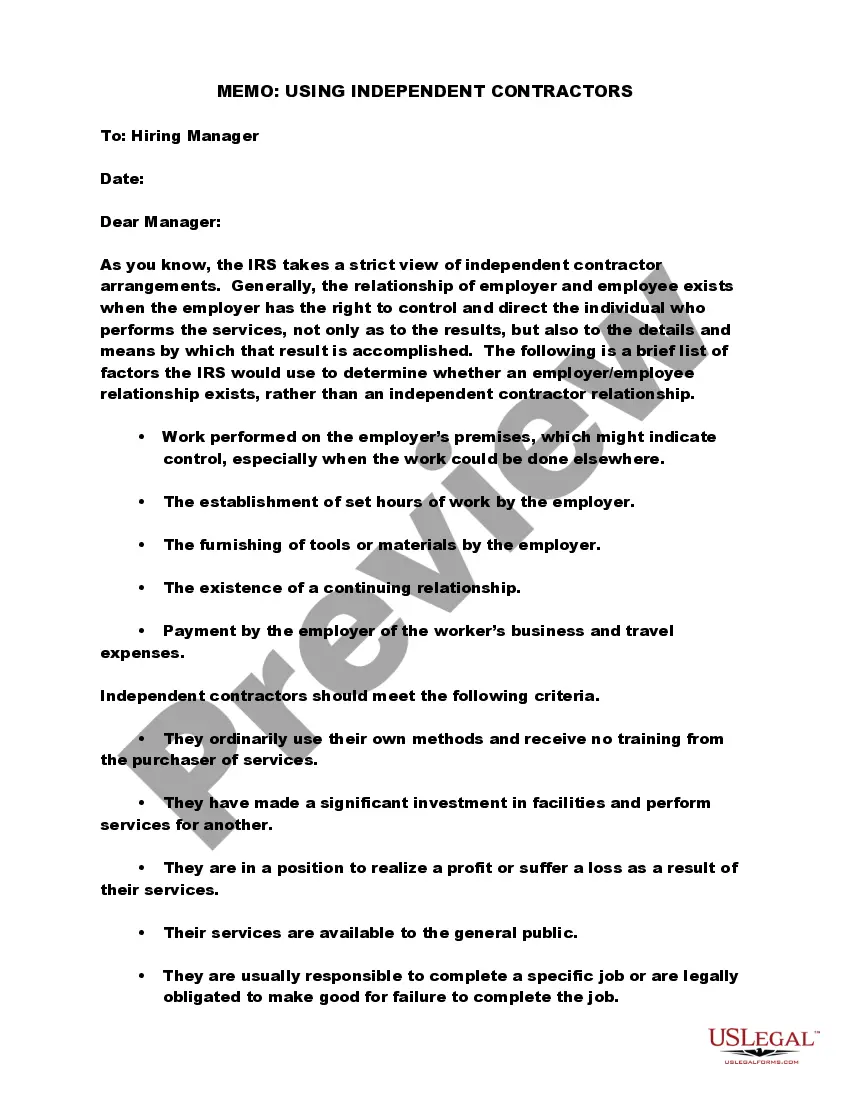

Title: Understanding Kentucky Memo — Using Self-Employed Independent Contractors Introduction: Kentucky Memo — Using Self-Employed Independent Contractors is a set of guidelines issued by the Kentucky Department of Revenue to help individuals and businesses navigate the tax laws and regulations related to engaging self-employed independent contractors. This memo provides key insights into the classification of independent contractors, tax obligations, and reporting requirements, ensuring compliance and reducing potential legal risks. This article aims to provide a detailed description of the Kentucky Memo, its importance, and its various types if applicable. Keywords: Kentucky, Memo, Self-Employed Independent Contractors, tax laws, regulations, classification, obligations, reporting requirements, compliance, legal risks. 1. Understanding the Kentucky Memo's Purpose: The Kentucky Memo on Using Self-Employed Independent Contractors serves as a comprehensive guide to help businesses determine whether a worker qualifies as an independent contractor or an employee. By following these guidelines, businesses can ensure accurate tax withholding, avoid misclassification penalties, and maintain legal compliance. 2. Key Factors for Determining Independent Contractor Status: The Kentucky Memo outlines several factors that help determine whether a worker is an independent contractor or an employee. These factors include control, financial arrangement, and the presence or absence of certain employer-employee relationships. Understanding these factors is crucial to correctly categorize workers and fulfill associated tax obligations. 3. Tax Obligations for Engaging Independent Contractors: The Kentucky Memo provides clarity on the tax obligations that businesses must fulfill when engaging self-employed independent contractors. It outlines the responsibility for reporting income, withholding taxes, and paying applicable state taxes. Understanding these obligations is vital to ensure accurate and timely tax compliance. 4. Reporting Requirements and Forms: The Kentucky Memo elaborates on the reporting requirements and forms necessary for engaging independent contractors. It explains what forms need to be filed, such as the IRS Form 1099-MISC, which reports the income paid to independent contractors. By following these guidelines, businesses can avoid penalties associated with incorrect or late filings. 5. Penalties and Legal Risks for Non-Compliance: The Kentucky Department of Revenue enforces strict penalties for businesses that fail to comply with the regulations outlined in the memo. These penalties can include fines, interest, and potential legal consequences. Adhering to the Kentucky Memo reduces the risk of penalties, lawsuits, and reputational damage. Types of Kentucky Memo — Using Self-Employed Independent Contractors (if applicable): 1. Initial Guidance Memo: This type provides general information on the classification and tax obligations related to self-employed independent contractors in Kentucky. 2. Update Memo: These memos are issued periodically to address changes in tax laws, regulations, or any updated guidelines related to self-employed independent contractors. 3. Industry-Specific Memo: In certain cases, Kentucky may issue targeted memos providing industry-specific guidance for utilizing self-employed independent contractors, considering unique requirements or practices within specific sectors. Conclusion: Understanding and adhering to the guidelines outlined in the Kentucky Memo — Using Self-Employed Independent Contractors is crucial for businesses and individuals engaging self-employed workers. By correctly categorizing independent contractors and fulfilling tax obligations, organizations can maintain compliance with Kentucky law, avoid penalties, and operate with confidence. Regularly consulting the Kentucky Department of Revenue's official website and any updates made to the memo will ensure up-to-date information and compliance with current regulations.

Title: Understanding Kentucky Memo — Using Self-Employed Independent Contractors Introduction: Kentucky Memo — Using Self-Employed Independent Contractors is a set of guidelines issued by the Kentucky Department of Revenue to help individuals and businesses navigate the tax laws and regulations related to engaging self-employed independent contractors. This memo provides key insights into the classification of independent contractors, tax obligations, and reporting requirements, ensuring compliance and reducing potential legal risks. This article aims to provide a detailed description of the Kentucky Memo, its importance, and its various types if applicable. Keywords: Kentucky, Memo, Self-Employed Independent Contractors, tax laws, regulations, classification, obligations, reporting requirements, compliance, legal risks. 1. Understanding the Kentucky Memo's Purpose: The Kentucky Memo on Using Self-Employed Independent Contractors serves as a comprehensive guide to help businesses determine whether a worker qualifies as an independent contractor or an employee. By following these guidelines, businesses can ensure accurate tax withholding, avoid misclassification penalties, and maintain legal compliance. 2. Key Factors for Determining Independent Contractor Status: The Kentucky Memo outlines several factors that help determine whether a worker is an independent contractor or an employee. These factors include control, financial arrangement, and the presence or absence of certain employer-employee relationships. Understanding these factors is crucial to correctly categorize workers and fulfill associated tax obligations. 3. Tax Obligations for Engaging Independent Contractors: The Kentucky Memo provides clarity on the tax obligations that businesses must fulfill when engaging self-employed independent contractors. It outlines the responsibility for reporting income, withholding taxes, and paying applicable state taxes. Understanding these obligations is vital to ensure accurate and timely tax compliance. 4. Reporting Requirements and Forms: The Kentucky Memo elaborates on the reporting requirements and forms necessary for engaging independent contractors. It explains what forms need to be filed, such as the IRS Form 1099-MISC, which reports the income paid to independent contractors. By following these guidelines, businesses can avoid penalties associated with incorrect or late filings. 5. Penalties and Legal Risks for Non-Compliance: The Kentucky Department of Revenue enforces strict penalties for businesses that fail to comply with the regulations outlined in the memo. These penalties can include fines, interest, and potential legal consequences. Adhering to the Kentucky Memo reduces the risk of penalties, lawsuits, and reputational damage. Types of Kentucky Memo — Using Self-Employed Independent Contractors (if applicable): 1. Initial Guidance Memo: This type provides general information on the classification and tax obligations related to self-employed independent contractors in Kentucky. 2. Update Memo: These memos are issued periodically to address changes in tax laws, regulations, or any updated guidelines related to self-employed independent contractors. 3. Industry-Specific Memo: In certain cases, Kentucky may issue targeted memos providing industry-specific guidance for utilizing self-employed independent contractors, considering unique requirements or practices within specific sectors. Conclusion: Understanding and adhering to the guidelines outlined in the Kentucky Memo — Using Self-Employed Independent Contractors is crucial for businesses and individuals engaging self-employed workers. By correctly categorizing independent contractors and fulfilling tax obligations, organizations can maintain compliance with Kentucky law, avoid penalties, and operate with confidence. Regularly consulting the Kentucky Department of Revenue's official website and any updates made to the memo will ensure up-to-date information and compliance with current regulations.