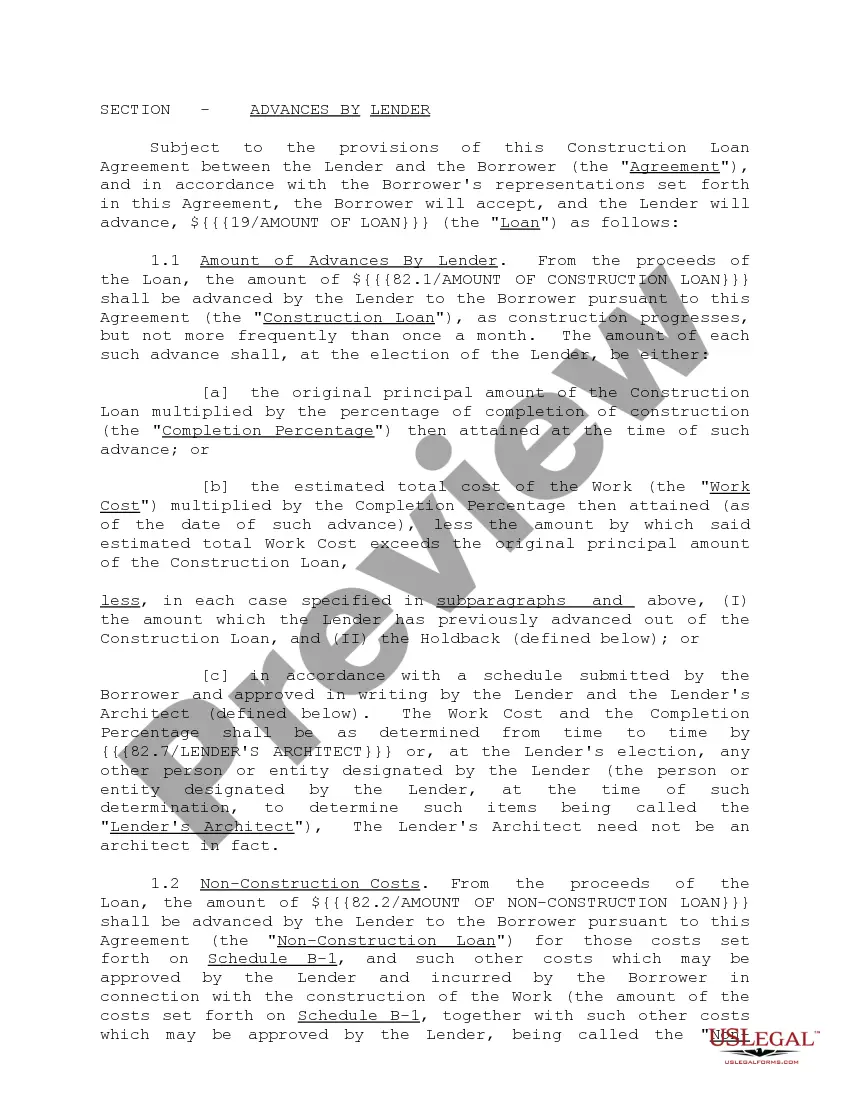

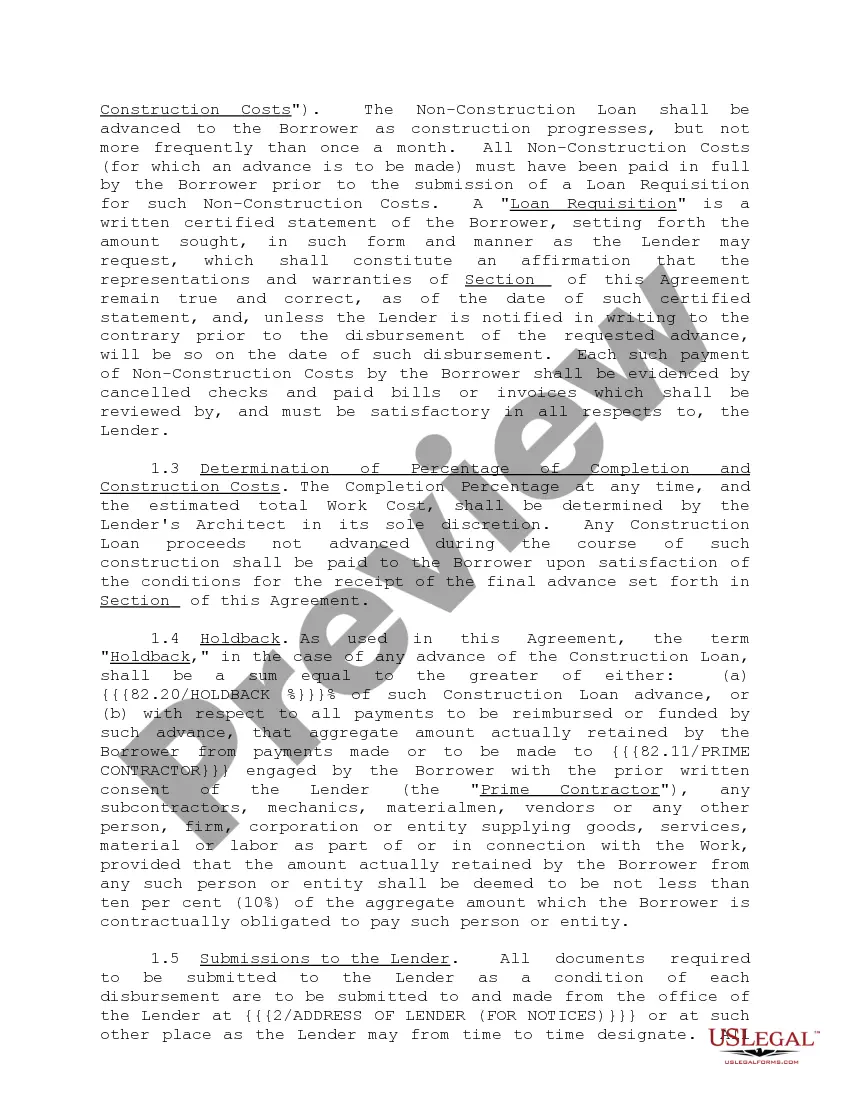

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Kentucky Construction Loan Agreements and Variations: Explained Kentucky construction loan agreements refer to legally binding contracts between lenders and borrowers involved in construction projects within the state of Kentucky. These agreements outline the terms and conditions under which the borrower can access funds for the construction project and the repayment terms that the borrower must adhere to. In Kentucky, there are various types of construction loan agreements and variations, each serving a different purpose and catering to the specific needs and circumstances of the borrowers. Some notable types of construction loan agreements in Kentucky include: 1. Construction-to-Permanent Loan Agreement: Also known as a "one-time close" loan agreement, this type of agreement provides financing for both the construction of the project and the permanent mortgage once construction is completed. It eliminates the need for separate financing and closing costs, streamlining the process for the borrower. 2. Stand-Alone Construction Loan Agreement: This type of agreement provides financing solely for the construction phase of the project. Once construction is completed, the borrower will need to secure separate permanent financing, typically through a mortgage or refinancing option. 3. Renovation and Rehabilitation Loan Agreement: This type of agreement is designed for projects involving the renovation or rehabilitation of existing properties. These loans help cover the costs of construction, including repairs, upgrades, and improvements, allowing borrowers to enhance the value and functionality of their properties. 4. Bridge/Interim Construction Loan Agreement: Bridge loans are short-term agreements that provide financing to bridge the funding gap during the construction phase until the borrower secures permanent financing. These loans help cover construction costs, enabling timely project completion. 5. Owner-Builder Construction Loan Agreement: This agreement is specifically tailored for individuals or entities intending to act as their own general contractor or oversee the construction process themselves. It allows owner-builders to secure financing for their projects while assuming responsibility for the construction management. Kentucky's construction loan agreements typically include details such as loan amount, interest rates, repayment terms, construction timelines, disbursement schedules, inspection requirements, and documents needed for loan approval, among other crucial provisions. It is important for both lenders and borrowers involved in Kentucky construction projects to carefully review and negotiate the terms and conditions outlined in these agreements. Seeking legal advice from professionals familiar with construction law in Kentucky can help ensure compliance with relevant regulations and protect the interests of all parties involved. By understanding the various types of Kentucky construction loan agreements and their variations, borrowers can make informed decisions that align with their specific construction needs and financial goals. Likewise, lenders can offer tailored financing solutions that cater to the unique requirements of each construction project in Kentucky.Kentucky Construction Loan Agreements and Variations: Explained Kentucky construction loan agreements refer to legally binding contracts between lenders and borrowers involved in construction projects within the state of Kentucky. These agreements outline the terms and conditions under which the borrower can access funds for the construction project and the repayment terms that the borrower must adhere to. In Kentucky, there are various types of construction loan agreements and variations, each serving a different purpose and catering to the specific needs and circumstances of the borrowers. Some notable types of construction loan agreements in Kentucky include: 1. Construction-to-Permanent Loan Agreement: Also known as a "one-time close" loan agreement, this type of agreement provides financing for both the construction of the project and the permanent mortgage once construction is completed. It eliminates the need for separate financing and closing costs, streamlining the process for the borrower. 2. Stand-Alone Construction Loan Agreement: This type of agreement provides financing solely for the construction phase of the project. Once construction is completed, the borrower will need to secure separate permanent financing, typically through a mortgage or refinancing option. 3. Renovation and Rehabilitation Loan Agreement: This type of agreement is designed for projects involving the renovation or rehabilitation of existing properties. These loans help cover the costs of construction, including repairs, upgrades, and improvements, allowing borrowers to enhance the value and functionality of their properties. 4. Bridge/Interim Construction Loan Agreement: Bridge loans are short-term agreements that provide financing to bridge the funding gap during the construction phase until the borrower secures permanent financing. These loans help cover construction costs, enabling timely project completion. 5. Owner-Builder Construction Loan Agreement: This agreement is specifically tailored for individuals or entities intending to act as their own general contractor or oversee the construction process themselves. It allows owner-builders to secure financing for their projects while assuming responsibility for the construction management. Kentucky's construction loan agreements typically include details such as loan amount, interest rates, repayment terms, construction timelines, disbursement schedules, inspection requirements, and documents needed for loan approval, among other crucial provisions. It is important for both lenders and borrowers involved in Kentucky construction projects to carefully review and negotiate the terms and conditions outlined in these agreements. Seeking legal advice from professionals familiar with construction law in Kentucky can help ensure compliance with relevant regulations and protect the interests of all parties involved. By understanding the various types of Kentucky construction loan agreements and their variations, borrowers can make informed decisions that align with their specific construction needs and financial goals. Likewise, lenders can offer tailored financing solutions that cater to the unique requirements of each construction project in Kentucky.