"Under SEC law, a company that offers its own securities must register these investments with the SEC before it can sell them unless it meets an exception. One of those exceptions is selling unregistered investments to accredited investors.

To become an accredited investor the (SEC) requires certain wealth, income or knowledge requirements. The investor must fall into one of three categories. Firms selling unregistered securities must put investors through their own screening process to determine if investors can be considered an accredited investor.

The Verifying Individual or Entity should take reasonable steps to verify and determined that an Investor is an "accredited investor" as such term is defined in Rule 501 of the Securities Act, and hereby provides written confirmation. This letter serves to help the Entity determine status."

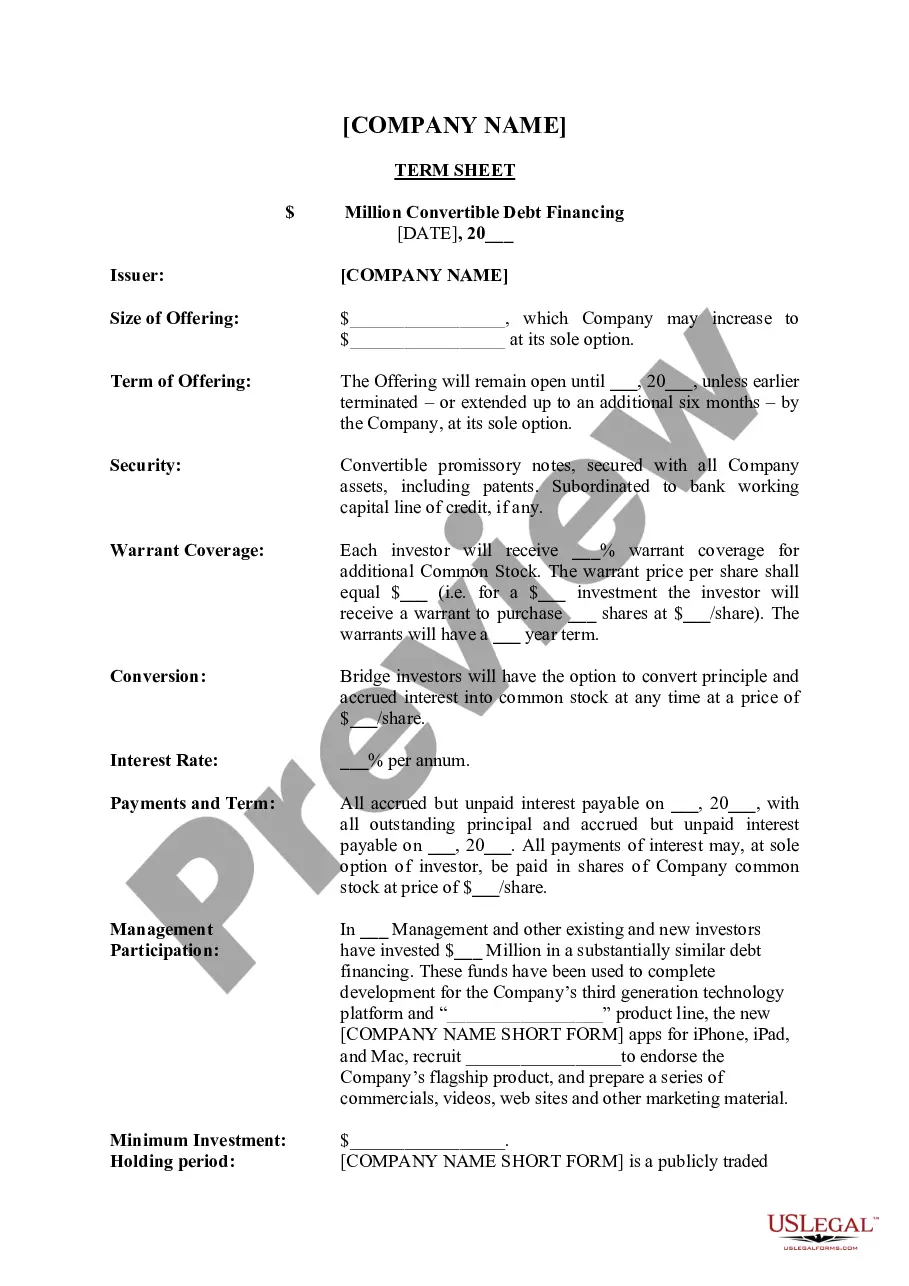

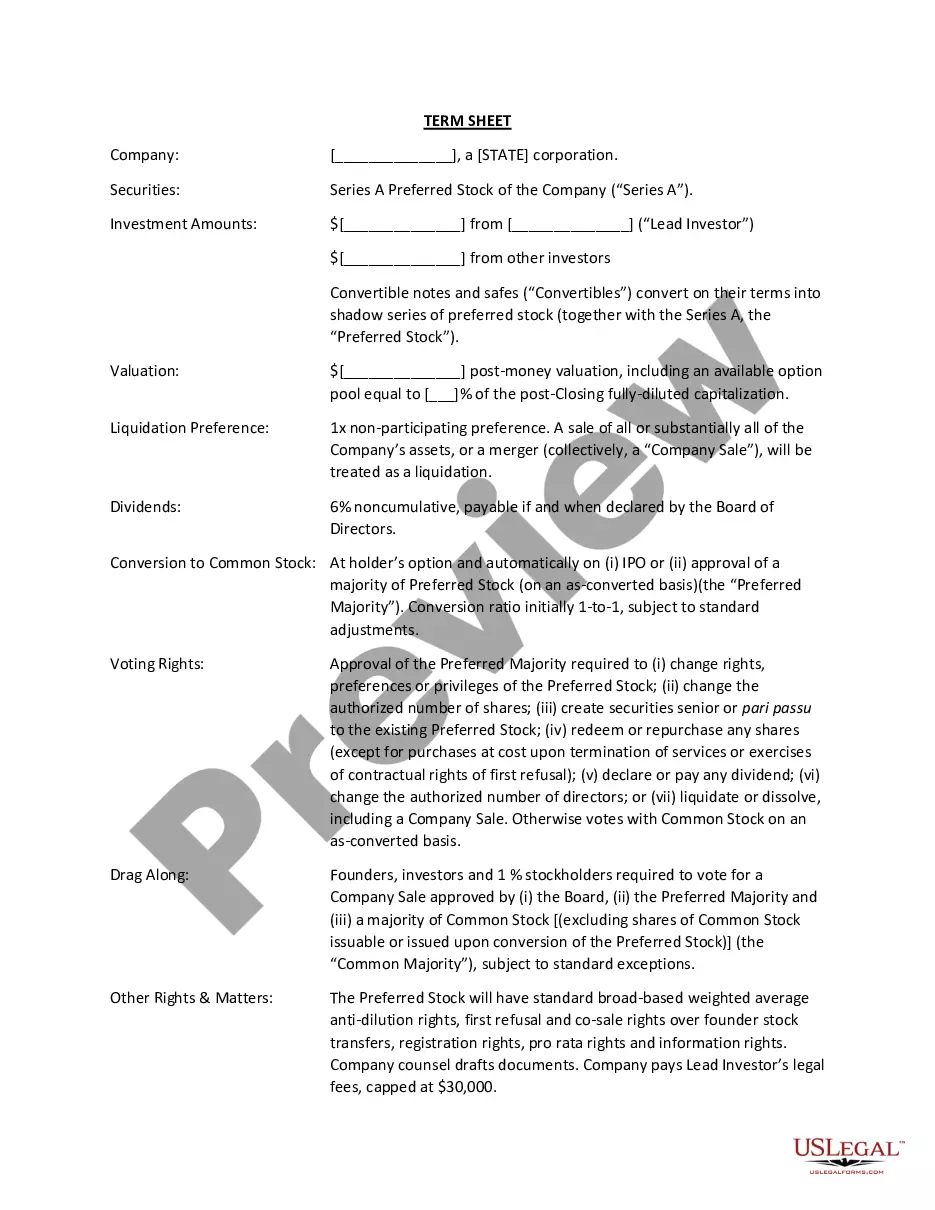

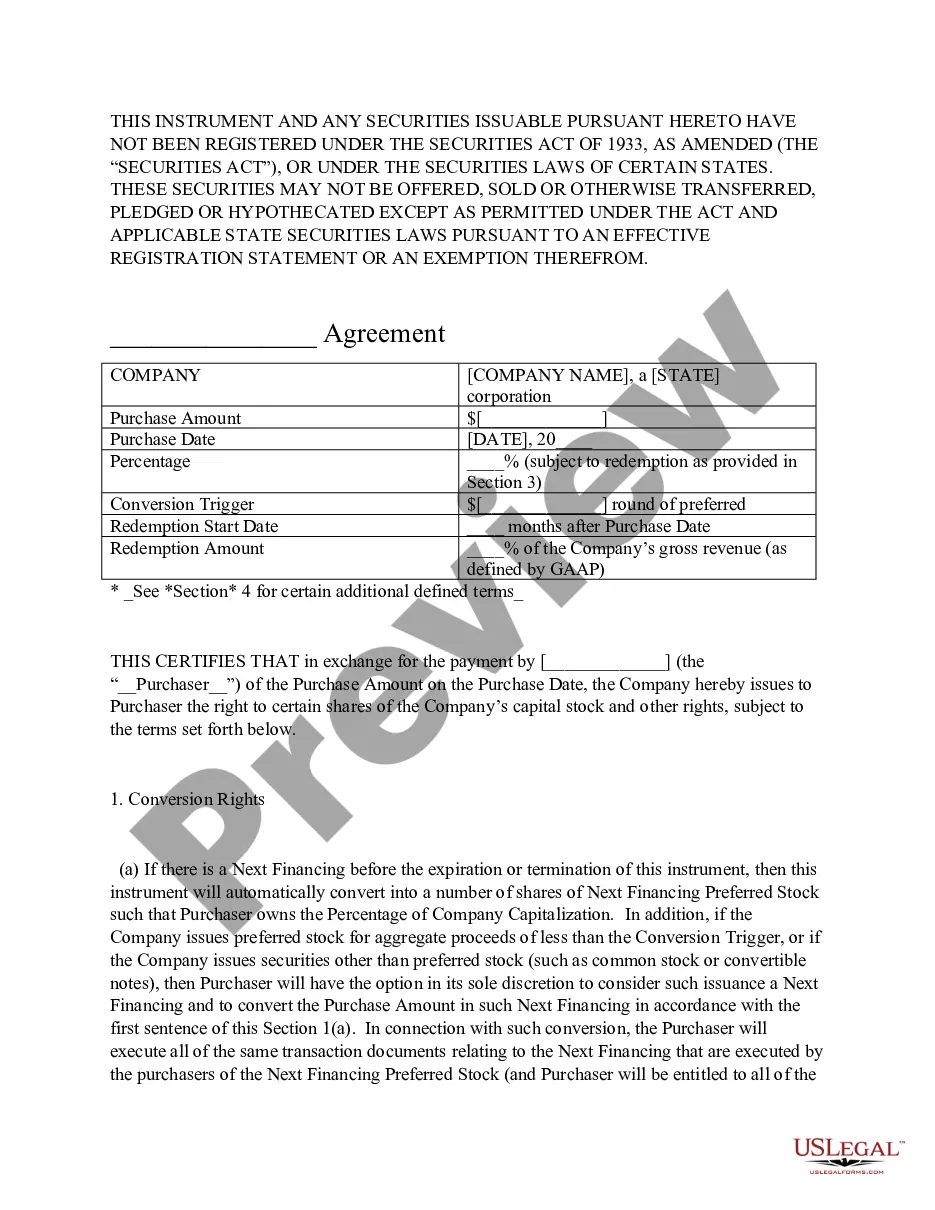

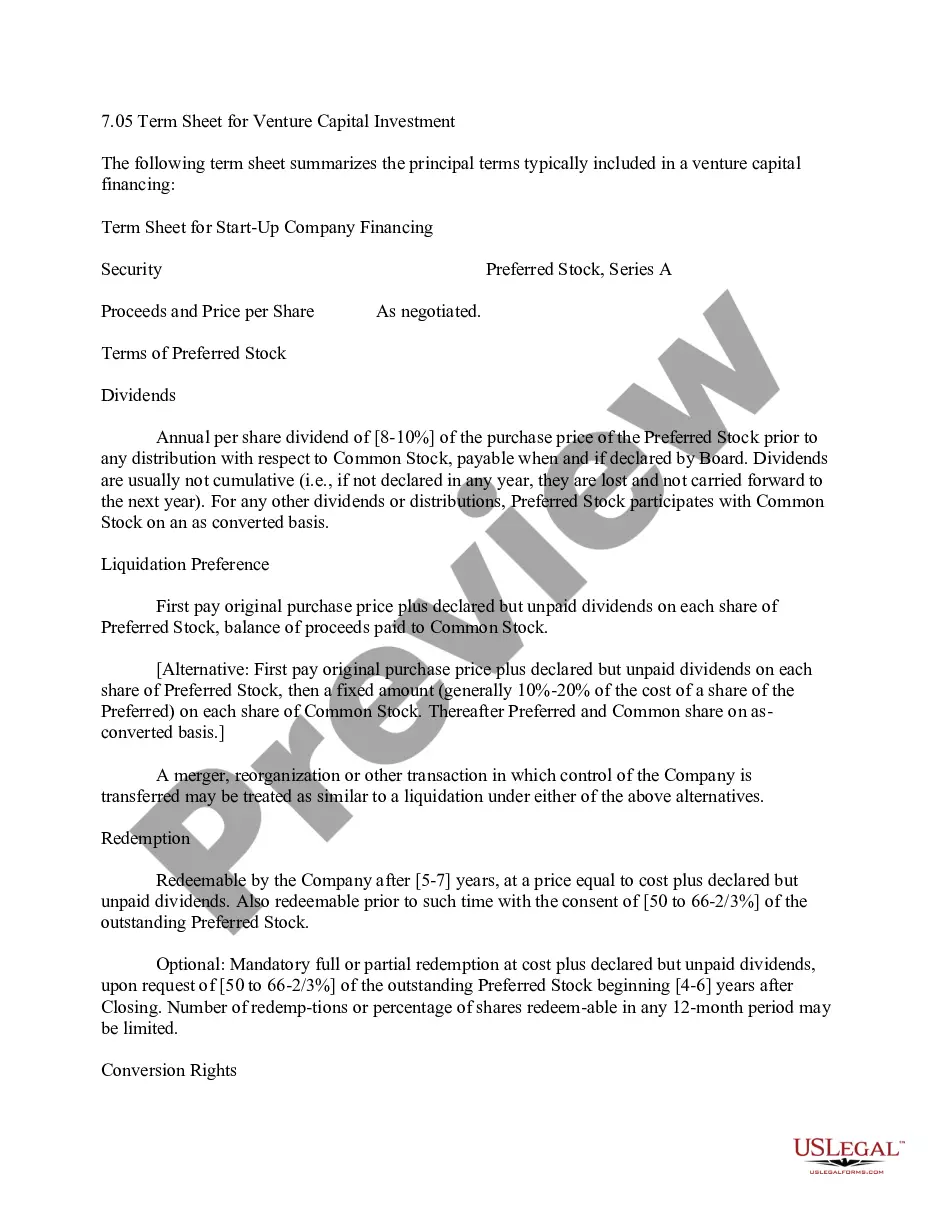

Kentucky Term Sheet - Convertible Debt Financing

State:

Multi-State

Control #:

US-ENTREP-0020-3

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Term Sheet - Convertible Debt Financing?

Discovering the right legitimate document template can be quite a have a problem. Obviously, there are a lot of templates available on the net, but how can you obtain the legitimate type you will need? Make use of the US Legal Forms web site. The services offers a huge number of templates, including the Kentucky Term Sheet - Convertible Debt Financing, which you can use for business and personal demands. Each of the kinds are checked out by specialists and meet up with state and federal specifications.

In case you are already registered, log in to your accounts and then click the Down load key to obtain the Kentucky Term Sheet - Convertible Debt Financing. Make use of accounts to check from the legitimate kinds you may have purchased in the past. Visit the My Forms tab of your accounts and acquire one more copy from the document you will need.

In case you are a new end user of US Legal Forms, allow me to share straightforward directions that you can stick to:

- Initial, be sure you have chosen the correct type for your city/region. You can examine the shape making use of the Preview key and browse the shape explanation to guarantee this is basically the best for you.

- When the type fails to meet up with your preferences, take advantage of the Seach area to discover the right type.

- When you are sure that the shape would work, click the Get now key to obtain the type.

- Select the rates prepare you would like and type in the necessary information and facts. Create your accounts and purchase the order with your PayPal accounts or bank card.

- Select the file structure and down load the legitimate document template to your product.

- Full, edit and print and signal the received Kentucky Term Sheet - Convertible Debt Financing.

US Legal Forms will be the most significant collection of legitimate kinds in which you can see numerous document templates. Make use of the company to down load skillfully-manufactured files that stick to express specifications.

Form popularity

FAQ

Although it is customary to forego a term sheet, in some cases it may be required if the parties need to negotiate certain terms. It can be advantageous to use a term sheet for the company to easily summarize the terms of the notes for potential other investors purchasing a convertible note.

The convertible debt that was listed as a non-current liability before the conversion now gets get treated as shareholder's equity.

For tax purposes, the tax basis of the convertible debt is the entire proceeds received at issuance of the debt. Thus, the book and tax bases of the convertible debt are different. ASC 740-10-55-51 addresses whether a deferred tax liability should be recognized for that basis difference.

Conversion to Equity - Accounting for Convertible Debt When the note converts, usually during a new funding round, the liability moves to the equity section of the balance sheet. At this stage, the convertible note is settled, and new equity instruments, typically preferred shares, are issued to the investor.

Typically, the result is that the amount will convert to shares. If the convertible notes convert into shares, the company will need to determine how many shares to issue to the noteholder. To do so, the company will usually divide the loan amount, plus any accrued interest, by a certain share price.

Convertible debt issued at a substantial premium could result in the instrument being treated entirely as an equity instrument for tax purposes, with no tax consequences during its term or upon redemption.

Convertible Notes are loans ? so they are recorded on the Balance Sheet of a company as a liability when they are made. Depending on the debt's maturity date, they can either be shown as a current liability (loans maturing within 12 months) or as a Long-term liability (loans maturing over 12 months).

Convertible debt is a debt hybrid product with an embedded option that allows the holder to convert the debt into equity in the future. The ratio is calculated by dividing the convertible security's par value by the conversion price of equity.