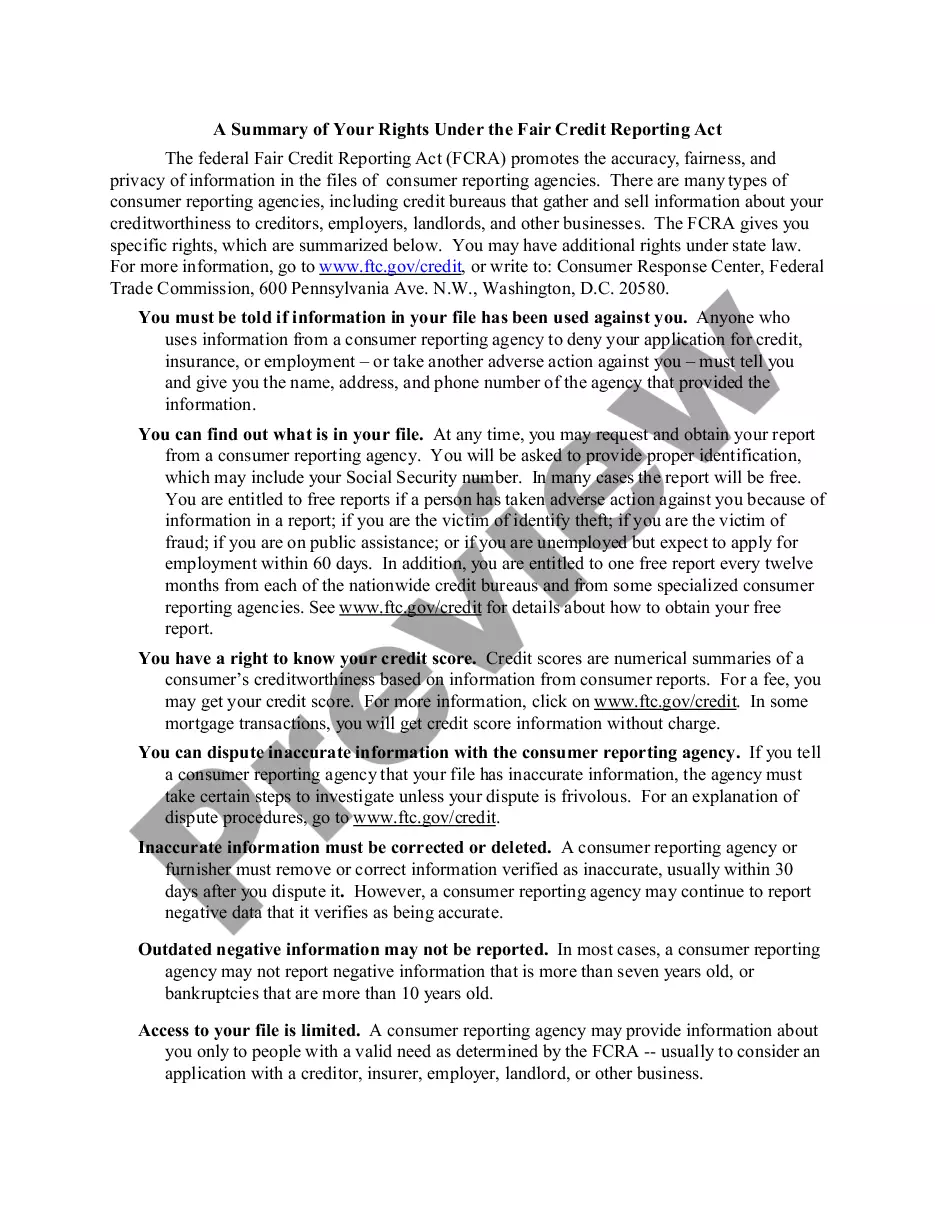

Kentucky The FACTA Red Flags Rule: A Primer

Description

How to fill out The FACTA Red Flags Rule: A Primer?

If you need to full, down load, or print out lawful papers templates, use US Legal Forms, the biggest collection of lawful forms, which can be found on-line. Use the site`s basic and convenient lookup to find the documents you will need. Various templates for organization and person functions are categorized by types and states, or search phrases. Use US Legal Forms to find the Kentucky The FACTA Red Flags Rule: A Primer in just a couple of mouse clicks.

Should you be presently a US Legal Forms customer, log in for your account and click on the Download key to obtain the Kentucky The FACTA Red Flags Rule: A Primer. You can also access forms you earlier delivered electronically in the My Forms tab of the account.

Should you use US Legal Forms initially, follow the instructions below:

- Step 1. Be sure you have selected the shape to the appropriate town/region.

- Step 2. Make use of the Preview solution to look over the form`s content. Don`t overlook to read through the explanation.

- Step 3. Should you be not happy with all the develop, use the Look for discipline towards the top of the display screen to get other models in the lawful develop design.

- Step 4. When you have identified the shape you will need, go through the Get now key. Pick the rates plan you prefer and add your references to register on an account.

- Step 5. Process the transaction. You can utilize your bank card or PayPal account to finish the transaction.

- Step 6. Choose the file format in the lawful develop and down load it on your own gadget.

- Step 7. Complete, revise and print out or indication the Kentucky The FACTA Red Flags Rule: A Primer.

Every single lawful papers design you acquire is the one you have for a long time. You possess acces to every single develop you delivered electronically within your acccount. Select the My Forms portion and decide on a develop to print out or down load once more.

Compete and down load, and print out the Kentucky The FACTA Red Flags Rule: A Primer with US Legal Forms. There are millions of specialist and express-certain forms you can utilize to your organization or person requirements.

Form popularity

FAQ

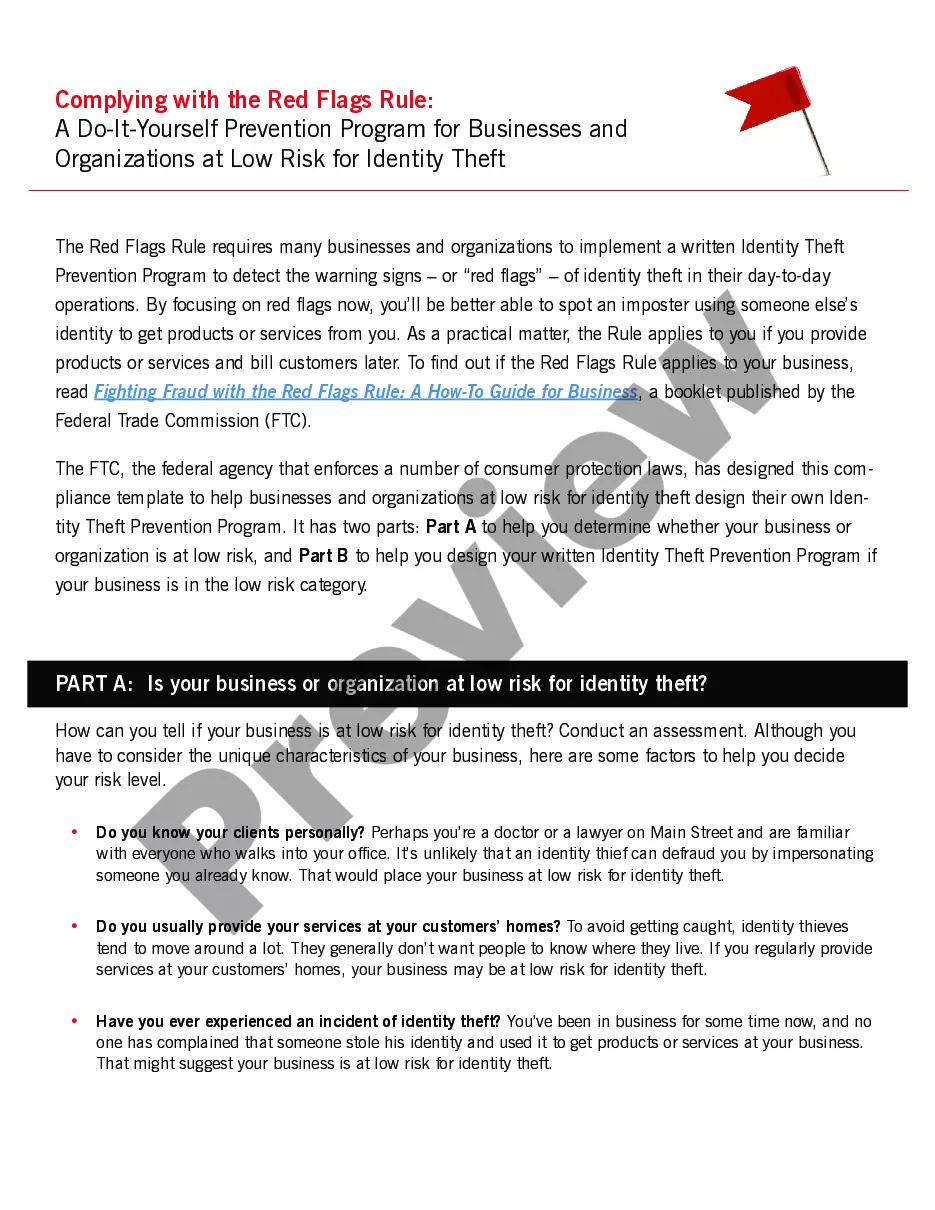

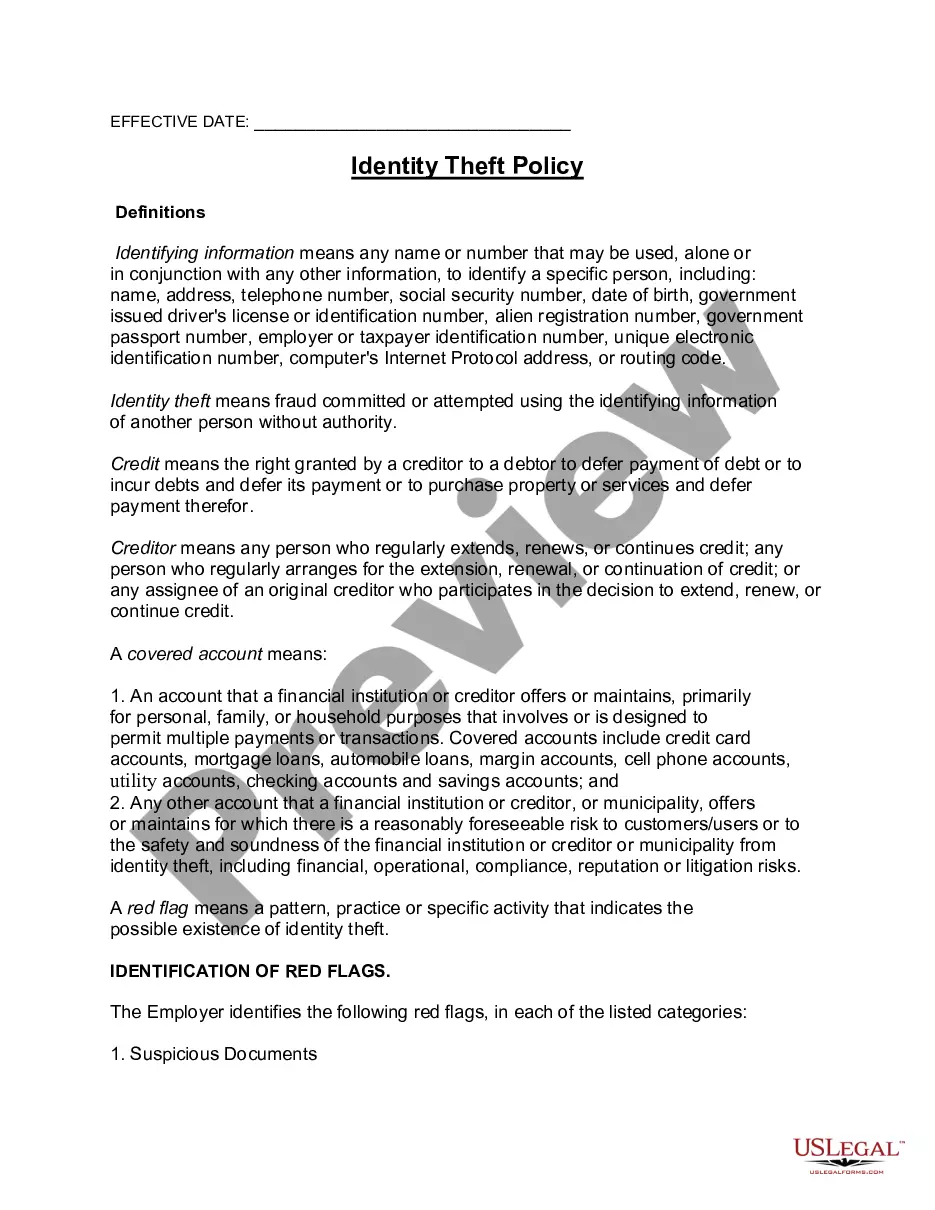

Hear this out loud PauseThe Red Flags Rule requires specified firms to create a written Identity Theft Prevention Program (ITPP) designed to identify, detect and respond to ?red flags??patterns, practices or specific activities?that could indicate identity theft. FTC FACT Act Red Flags Rule Template - finra finra ? default ? files ? Industry finra ? default ? files ? Industry PDF

The Red Flags Rule calls for financial institutions and creditors to implement red flags to detect and prevent against identity theft. Institutions are required to have a written identity theft prevention program (ITPP) to govern their organization and protect their consumers. FACTA Red Flags Rule Regulatory Compliance - Experian Experian ? business ? solutions ? red... Experian ? business ? solutions ? red...

Hear this out loud PauseThe Red Flags Rule requires that each "financial institution" or "creditor"?which includes most securities firms?implement a written program to detect, prevent and mitigate identity theft in connection with the opening or maintenance of "covered accounts." These include consumer accounts that permit multiple payments ... Red Flags Rule - Wikipedia wikipedia.org ? wiki ? Red_Flags_Rule wikipedia.org ? wiki ? Red_Flags_Rule

The Red Flags Rule requires organizations to implement a written identity theft prevention program to help them identify any of the relevant ?red flags? that indicate identity theft in daily operations. The Rule also offers steps to help prevent the crime and to mitigate its damage. What Is the FTC Red Flags Rule and Who Must Comply? I.S. Partners ? blog ? what-is-the-ftc-... I.S. Partners ? blog ? what-is-the-ftc-...

Under the Red Flags Rules, financial institutions and creditors must develop a written program that identifies and detects the relevant warning signs ? or ?red flags? ? of identity theft. Red Flag Rules - Texas Department of Savings and Mortgage Lending texas.gov ? mortgage-origination ? red-... texas.gov ? mortgage-origination ? red-...

Hear this out loud PauseInstitutions are required to have a written identity theft prevention program (ITPP) to govern their organization and protect their consumers. What's a red flag? The FTC defines a red flag as a pattern, practice or specific activity that indicates the possible existence of identity theft. FACTA Red Flags Rule Regulatory Compliance - Experian Experian ? business ? solutions ? red... Experian ? business ? solutions ? red...