Kentucky Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

If you wish to comprehensive, obtain, or produce authorized file layouts, use US Legal Forms, the most important assortment of authorized types, which can be found on the web. Take advantage of the site`s simple and handy research to find the documents you require. Numerous layouts for company and specific functions are sorted by types and claims, or search phrases. Use US Legal Forms to find the Kentucky Assignment of Life Insurance as Collateral in a few click throughs.

In case you are presently a US Legal Forms buyer, log in to your bank account and then click the Download button to obtain the Kentucky Assignment of Life Insurance as Collateral. You can also access types you in the past downloaded in the My Forms tab of the bank account.

If you work with US Legal Forms the first time, follow the instructions beneath:

- Step 1. Be sure you have chosen the shape for the appropriate area/land.

- Step 2. Make use of the Preview method to check out the form`s articles. Never forget about to read the explanation.

- Step 3. In case you are unsatisfied together with the kind, make use of the Lookup industry near the top of the monitor to find other variations of the authorized kind template.

- Step 4. After you have located the shape you require, go through the Purchase now button. Choose the costs prepare you like and add your references to sign up on an bank account.

- Step 5. Approach the transaction. You may use your credit card or PayPal bank account to complete the transaction.

- Step 6. Choose the formatting of the authorized kind and obtain it on your own gadget.

- Step 7. Complete, change and produce or sign the Kentucky Assignment of Life Insurance as Collateral.

Every authorized file template you get is your own property for a long time. You possess acces to every kind you downloaded with your acccount. Select the My Forms area and decide on a kind to produce or obtain yet again.

Be competitive and obtain, and produce the Kentucky Assignment of Life Insurance as Collateral with US Legal Forms. There are thousands of professional and condition-specific types you may use for your personal company or specific needs.

Form popularity

FAQ

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment.

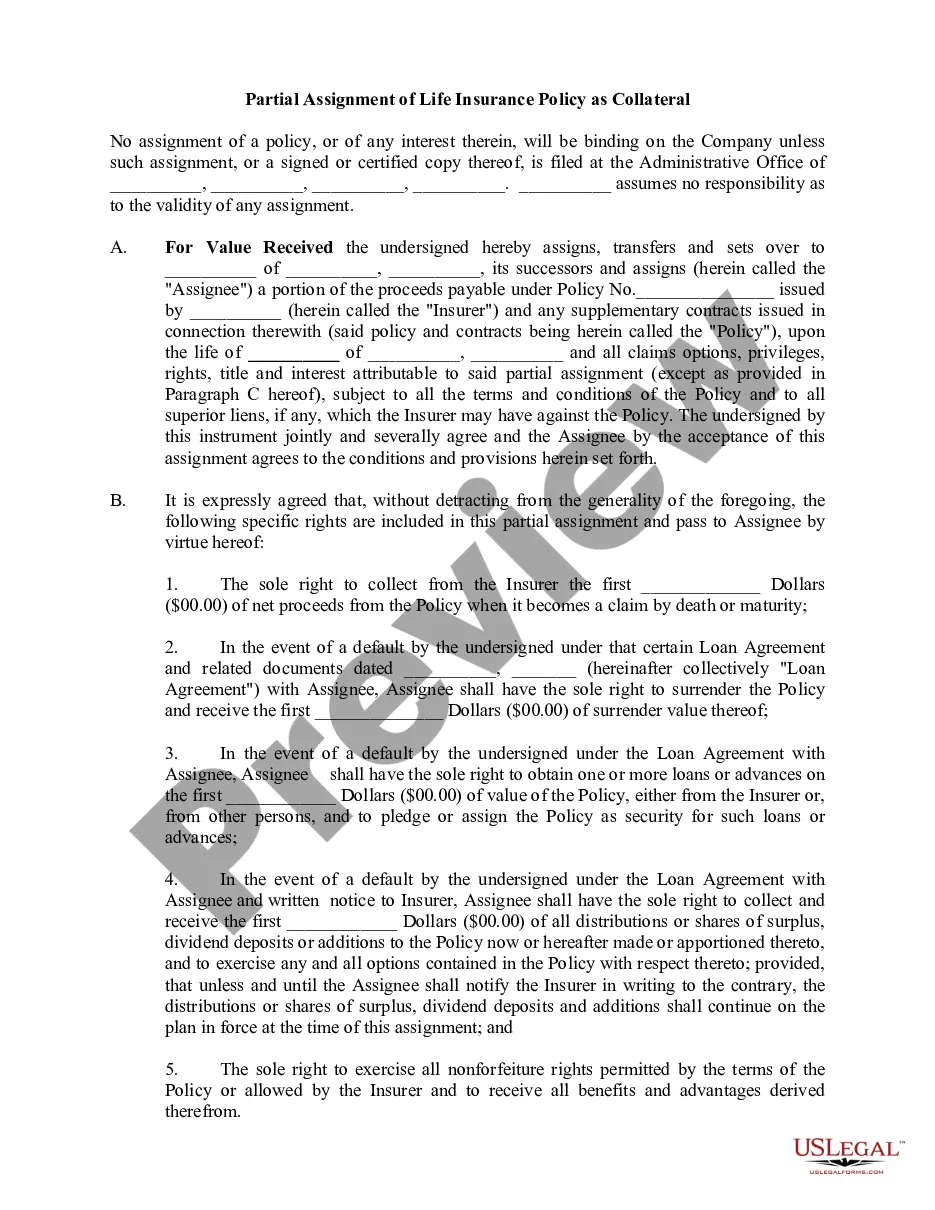

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

You can request a loan from your life insurance company for any reason, and there isn't an approval process. The only requirement is that you have sufficient cash value to borrow against (minimum amounts vary by insurer).

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

A collateral assignment supersedes your beneficiaries' rights to the death benefit. If you die, the life insurance company pays the lender, or assignee, the loan balance. As noted earlier, any remaining benefit goes to your beneficiaries.

A collateral assignment of life insurance is a method of securing a loan by using a life insurance policy as collateral. If you pass away before the loan is repaid, the lender can collect the outstanding loan balance from the death benefit of your life insurance policy.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.