Louisiana Inventory, Probate

Overview of this form

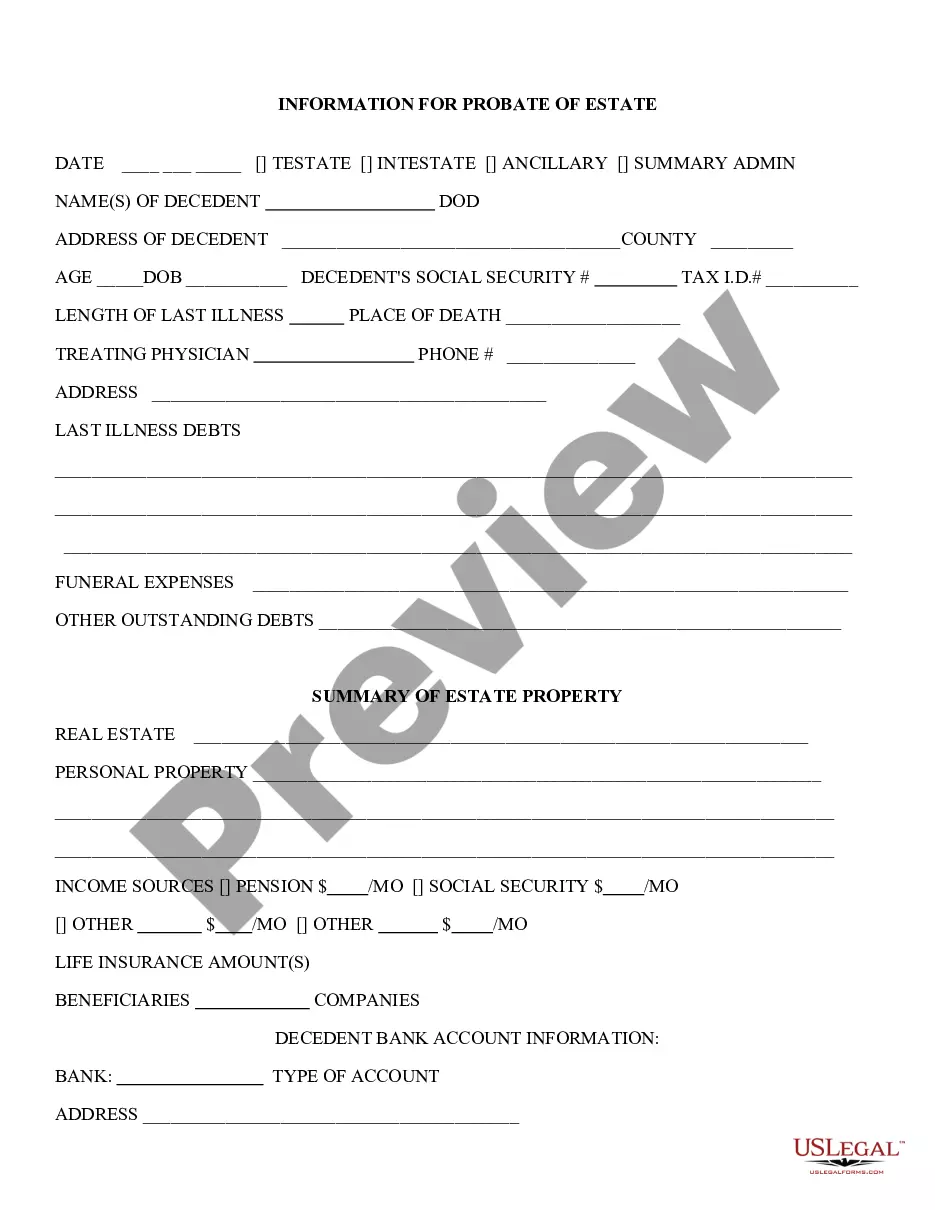

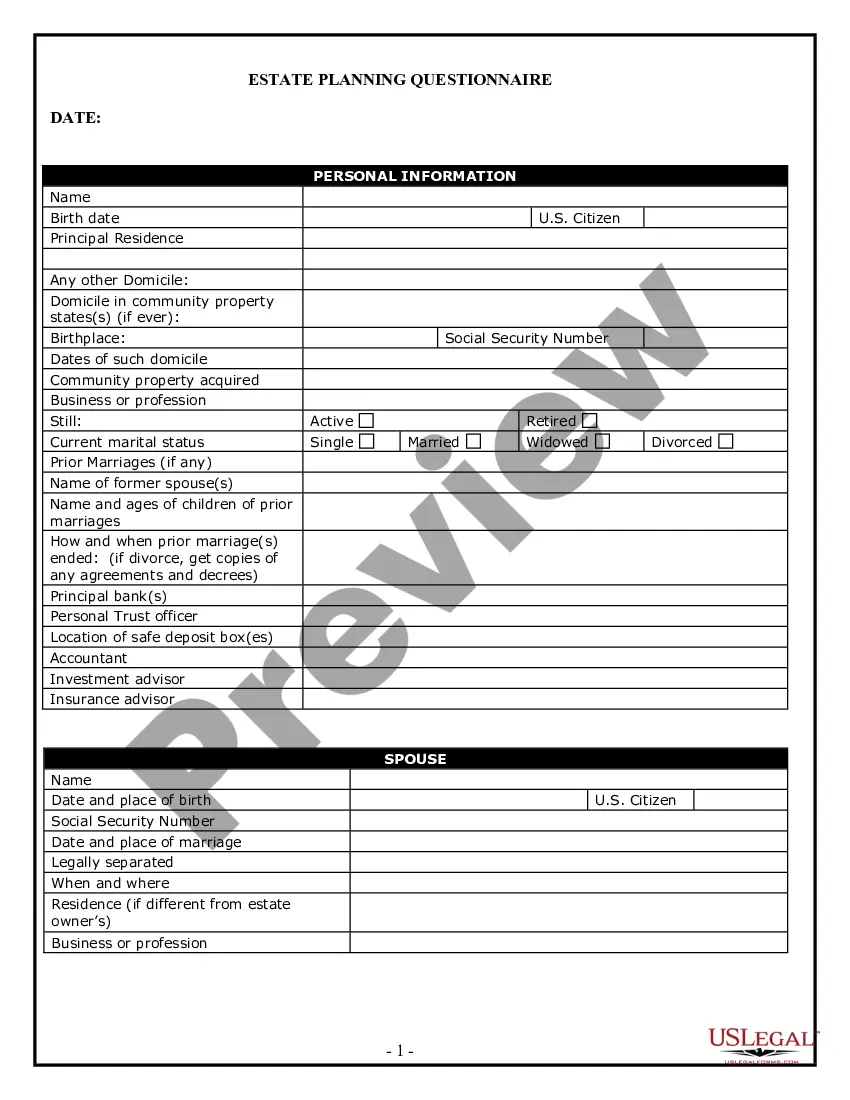

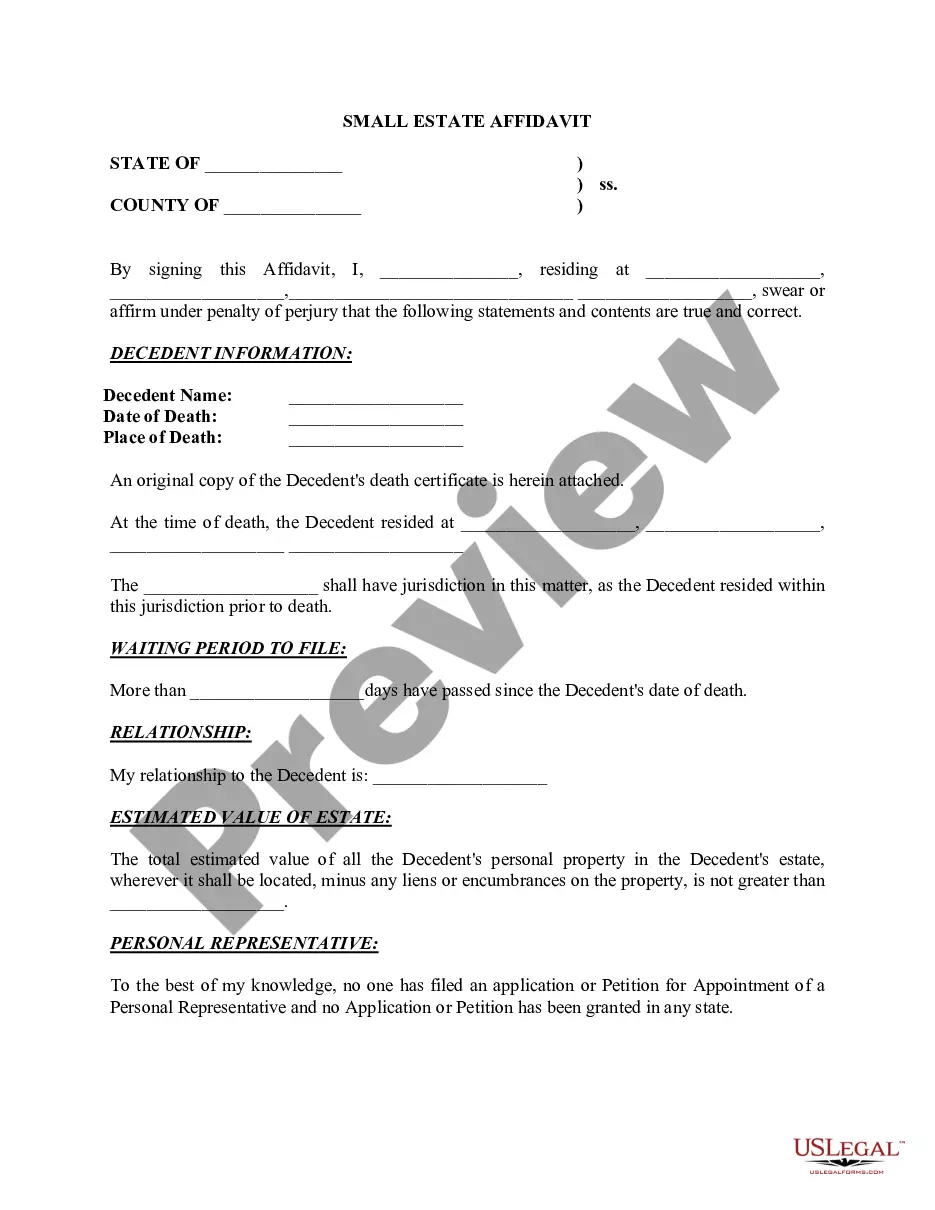

The Inventory, Probate form is a legal document used in the probate process to list and describe the assets of a deceased person. It serves as an official record that identifies the property owned by the decedent at the time of their death. This form is vital for ensuring that all assets are accounted for during probate proceedings, facilitating the distribution of these assets to rightful heirs and managing any outstanding debts and taxes. Unlike other legal forms related to estate planning, this inventory specifically addresses the categorization and valuation of real estate and other assets for court purposes.

Form components explained

- Heading indicating the state and parish of the inventory.

- Identification of the notary public who conducted the inventory.

- List of community assets, including property details and appraisals.

- Witnesses' names and signatures confirming the inventory.

- Valuation of listed assets, providing financial context for probate.

Common use cases

This form should be used when a person has passed away, and their estate is entering the probate process. It is essential for gathering and documenting all assets, particularly in situations where the decedent's will requires court supervision. You would use this form to ensure an accurate accounting of all property, which is critical when settling the estate and distributing assets among beneficiaries.

Who can use this document

- Executors or personal representatives of a deceased person's estate.

- Family members or heirs involved in the probate process.

- Legal professionals assisting with estate administration.

Instructions for completing this form

- Identify and list all real estate and personal property belonging to the decedent.

- Provide details about each property, including location, size, and physical characteristics.

- Document the value of each asset, referencing any appraisals or market values.

- Enter the names of competent witnesses present during the inventory process.

- Ensure the notary public signs and seals the document for legal validity.

Notarization guidance

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include all assets owned by the decedent.

- Inaccuracies in property descriptions or valuations.

- Omitting the signatures of required witnesses.

- Not notarizing the form when necessary.

Benefits of completing this form online

- Convenient access from anywhere, eliminating the need for physical paperwork.

- Editable templates that allow for accurate and individualized entries.

- Access to legal guidance ensures compliance with state laws.

- Quick download options for immediate use in probate proceedings.

Quick recap

- The Inventory, Probate form is essential for documenting all assets in a deceased's estate.

- It is used during the probate process to establish asset value and prepare for distribution.

- Complete the form accurately to avoid legal complications and ensure fair asset distribution.

Looking for another form?

Form popularity

FAQ

Real Estate, Bank Accounts, and Vehicles. Stocks and Bonds. Life Insurance and Retirement Plans. Wages and Business Interests. Intellectual Property. Debts and Judgments.

Determine Your State's Laws Regarding Inventory Forms. Review the Instructions Provided. Identify Real Property. Identify Personal Property. Identify Bank Accounts. Identify Retirement Accounts. Identify Non-Probate Assets. File the Form With the Court.

Q: How Long Does an Executor Have to Distribute Assets From a Will? A: Dear Waiting: In most states, a will must be executed within three years of a person's death.

All taxes and liabilities paid from the estate, including medical expenses, attorney fees, burial or cremation expenses, estate sale costs, appraisal expenses, and more. The executor should keep all receipts for any services or transactions needed to liquidate the assets of the deceased.

An inventory and appraisal is a required filing in California probate. The inventory and appraisal is a single document that (1) inventories the property in the decedent's estate and (2) contains an appraisal of the property in the inventory. California Probate Code § 8800(a).

When assets are being valued for probate, the valuation should be as at the date of death. For property, this will be what the market value at that time is; for personal possessions, it will be what they will fetch on the open market at the date of your death, and so on.

Before distributing assets to beneficiaries, the executor must pay valid debts and expenses, subject to any exclusions provided under state probate laws.The executor must maintain receipts and related documents and provide a detailed accounting to estate beneficiaries.

Beneficiaries are entitled to receive a financial accounting of the trust, including bank statements, regularly. When statements are not received as requested, a beneficiary must submit a written demand to the trustee.The court will review the trust account for any discrepancies or irregular activity.

Beneficiaries often must sign off on the inheritance they receive to acknowledge receipt of the distribution. For example, if you inherit a portion of real estate from the decedent, you must sign a deed accepting that real estate.