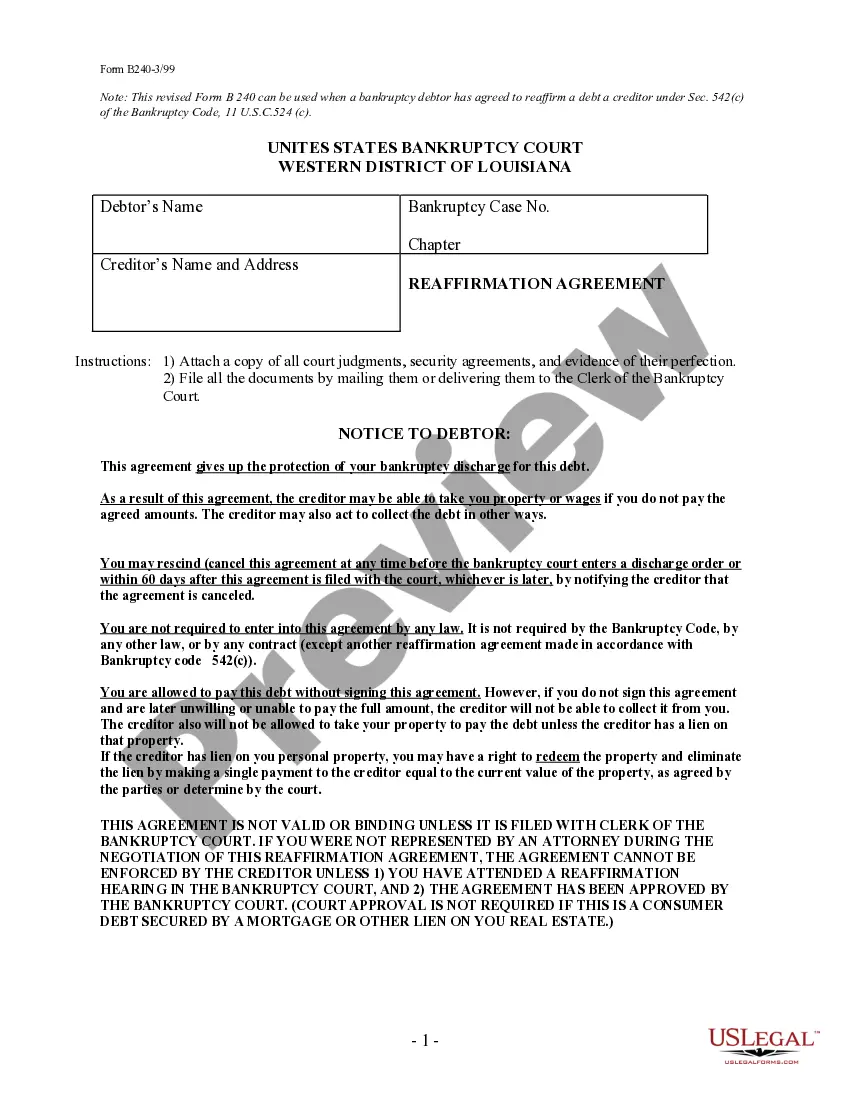

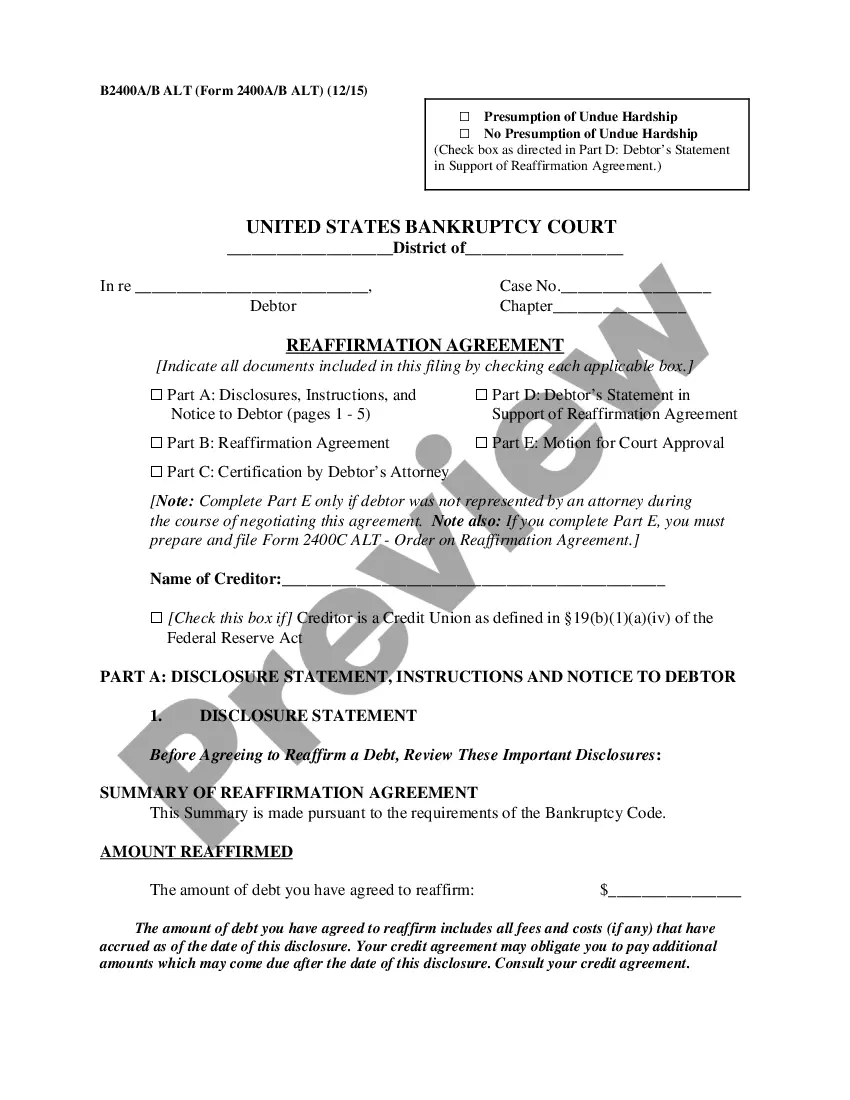

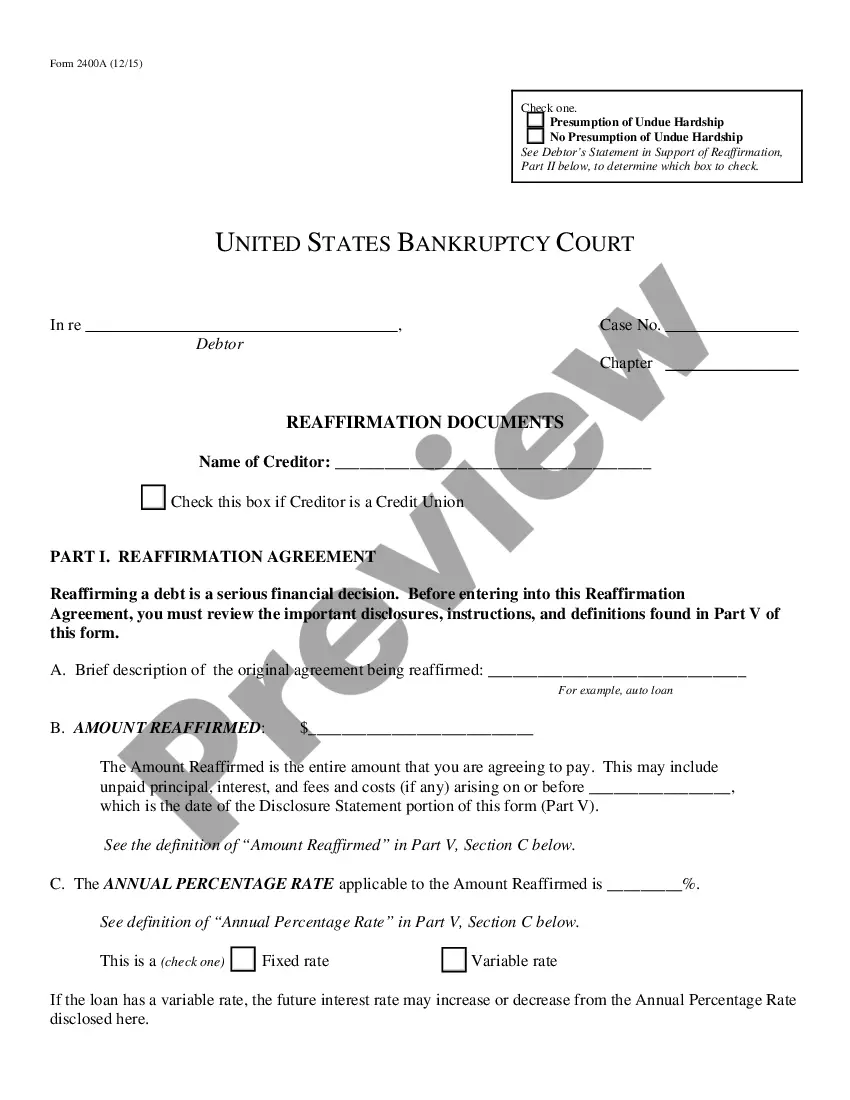

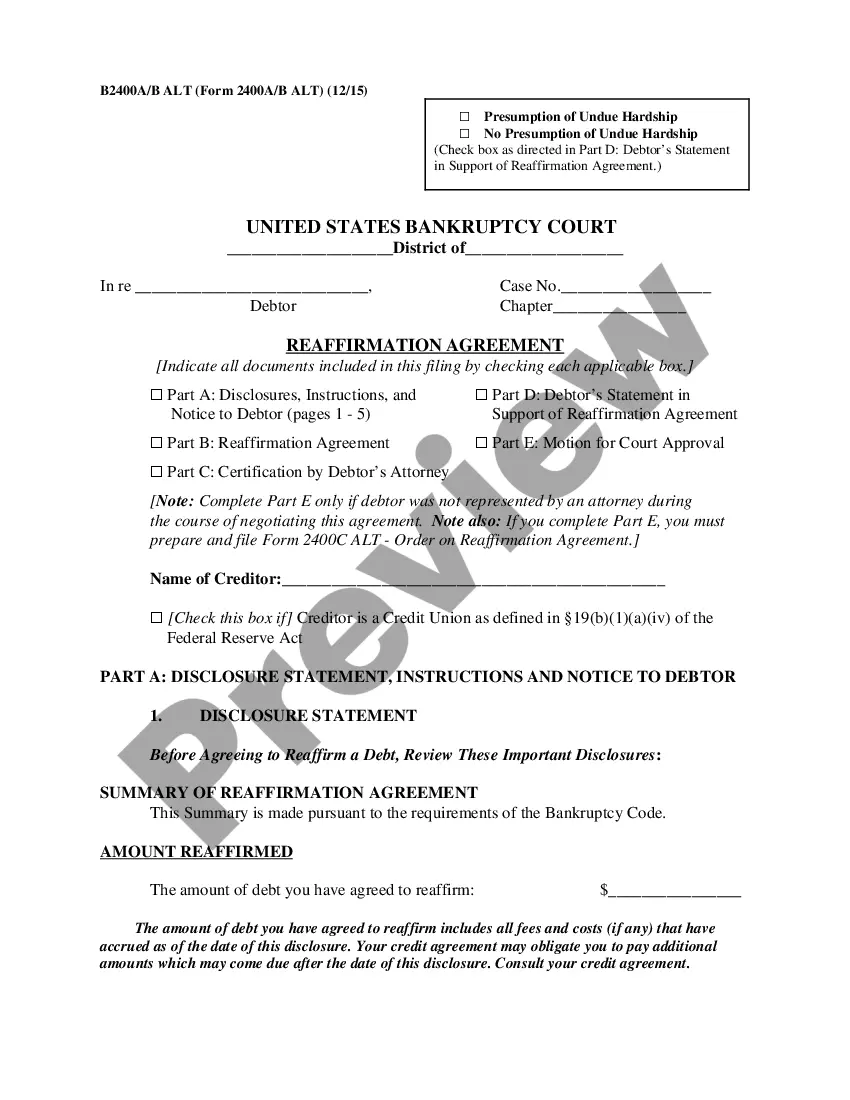

The reaffirmation agreement is used to reaffirm a particular debt. Once the debtor signs the agreement, the debtor gives up any protection of the bankruptcy discharge against the particular debt. The debtor is not required to enter into this agreement by any law.

Louisiana Reaffirmation Agreement

Category:

State:

Louisiana

Control #:

LA-BKR-801E

Format:

Word;

PDF;

Rich Text

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Louisiana Reaffirmation Agreement?

Greetings to the finest legal documents repository, US Legal Forms.

Here, you can discover any template including Louisiana Reaffirmation Agreement documents and obtain them (as many as you desire/require).

Create formal documents within a few hours, rather than days or weeks, without spending a fortune on a lawyer.

If the template satisfies all of your needs, click Purchase Now. To create an account, select a subscription plan. Use a card or PayPal account to sign up. Download the form in the required format (Word or PDF). Print the document and fill it out with your or your business’s details. Once you have completed the Louisiana Reaffirmation Agreement, send it to your attorney for validation. It’s an extra step but an essential one to ensure you’re fully protected. Register for US Legal Forms today and gain access to thousands of reusable templates.

- Acquire your state-specific document in just a few clicks and feel confident knowing it was prepared by our licensed attorneys.

- If you are an existing subscriber, simply Log In to your account and click Download next to the Louisiana Reaffirmation Agreement you need.

- Since US Legal Forms operates online, you will always have access to your saved documents, regardless of the device you are using.

- Find them in the My documents section.

- If you don't have an account yet, what exactly are you waiting for.

- Follow our instructions below to get started.

- If this is a state-specific form, verify its validity in the state you reside.

- Review the description (if provided) to ensure it’s the right template.

Form popularity

FAQ

Reaffirmation is voluntary Surrender may be the best thing if the car is simply too expensive or isn't reliable. You can choose to keep the car and continue paying without reaffirming. You take your chances that the lender will repossess the car, but you also keep the benefits of the bankruptcy discharge.

Reaffirmation agreements, although required by the bankruptcy laws for every secured debt that the debtor will continue to pay, are often not necessary in practice. This is because the only penalty for failure to sign the reaffirmation is that the creditor might repossess the collateral securing the loan.

Reaffirmation agreements are strictly voluntary. A debtor is not required to reaffirm any of his or her debts. If a debtor signs a reaffirmation agreement, the debtor agrees to pay a debt that otherwise might be discharged in his or her bankruptcy case.

To reaffirm a debt, you and the creditor agree to the terms of the new debt in a written reaffirmation agreement, which is filed with the court. You must file two court forms: Form 27 (the reaffirmation cover sheet) and Form 240A (the reaffirmation agreement itself.)

If you do not reaffirm the mortgage, your personal liability for paying the debt represented by the promissory note is discharged in your bankruptcy case.The company can foreclose the mortgage and force a foreclosure sale if you stop making payments.

To reaffirm a car loan, you must be able to show the court that the vehicle is necessary and that the payment is reasonable. You must also be able to show that the car payment isn't an undue hardship on your household (you'll still be able to afford the necessities of life). Effect of a reaffirmation agreement.

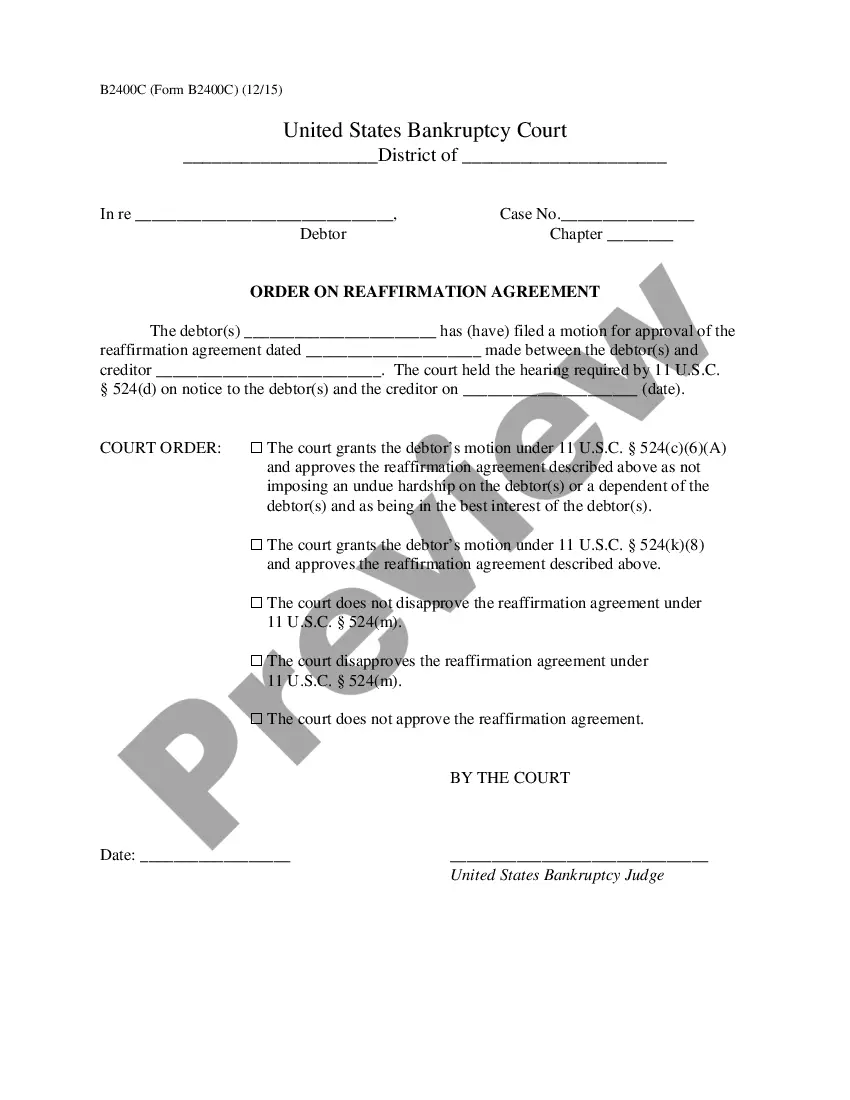

A reaffirmation must be filed with the Court before discharge. Once discharge has been entered, it is too late to reaffirm a debt. Theoretically you would have to reopen the bankruptcy, set aside your discharge, and then reaffirm the debt, then get your discharge reentered, and close the case.

If you don't sign a reaffirmation agreement, the lender can repossess your car after your case closes and the automatic stay lifts. Some car lenders are known to repossess the car immediately, even if you are current on payments.

Reaffirmation is the process wherein you agree to remain responsible for a debt so that you can keep the property securing the debt (collateral). You and the lender enter into a new contractusually on the same termsand submit it to the bankruptcy court.