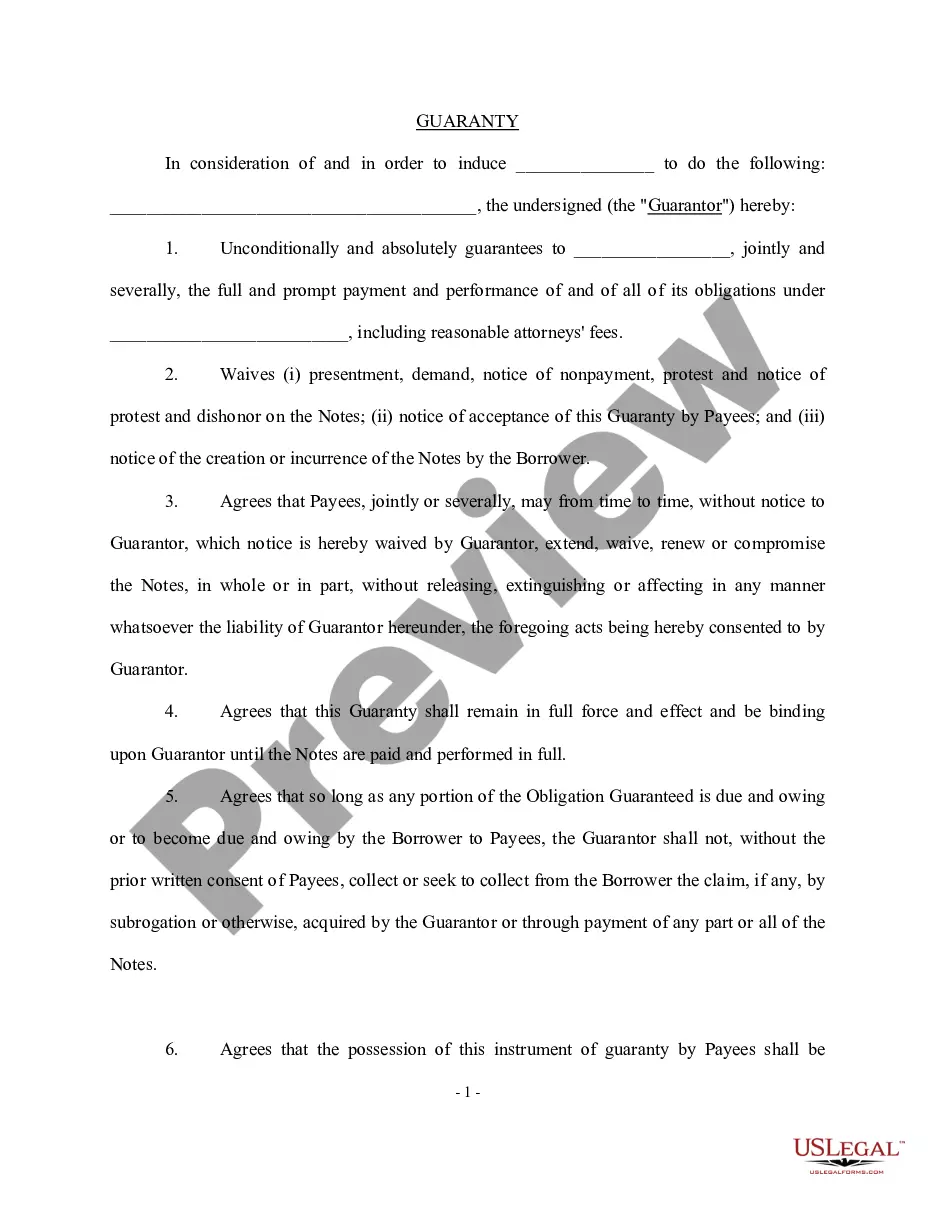

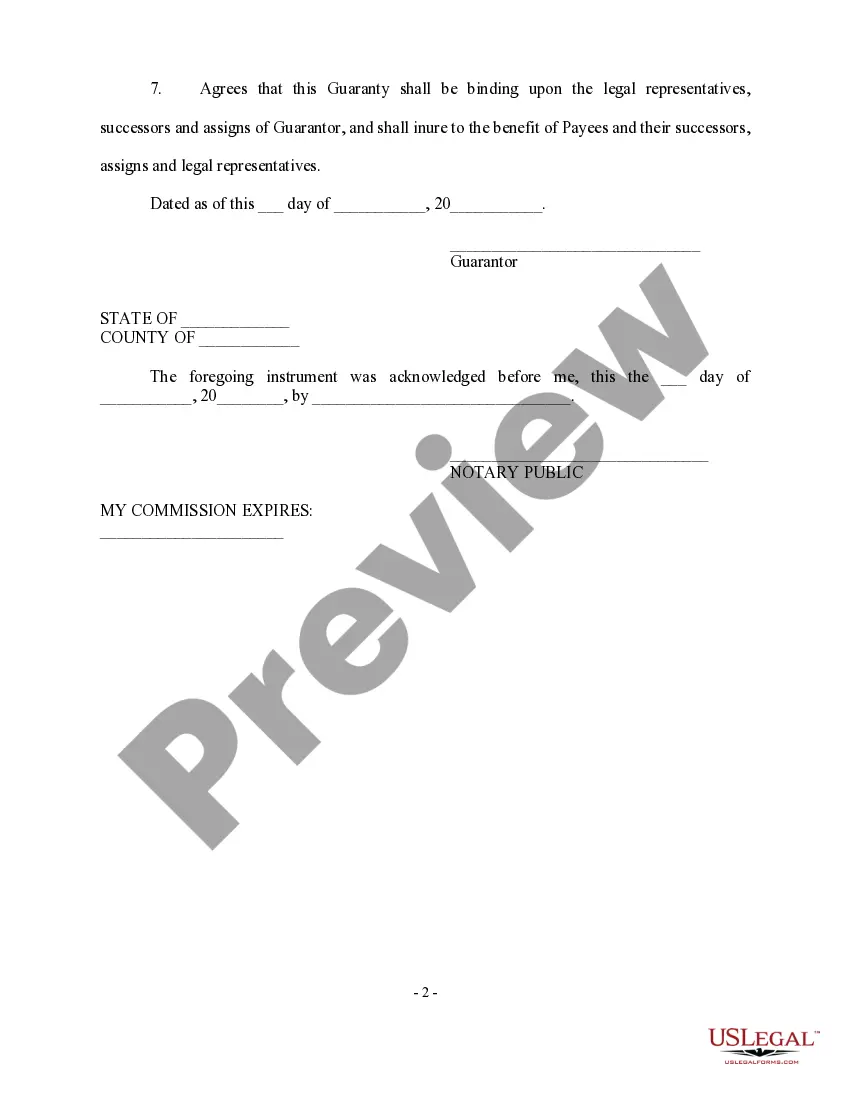

A Louisiana Personal Guaranty — General is a legal document that outlines the terms and conditions under which an individual (the guarantor) agrees to be held personally liable for the debts or obligations of another party (the debtor). It is commonly used in commercial transactions where creditors seek additional assurance of repayment. Keywords: Louisiana, personal guaranty, general, legal document, terms and conditions, individual, personally liable, debts, obligations, creditor, repayment. There are two main types of Louisiana Personal Guaranty — General: 1. Unlimited Personal Guaranty: In this type, the guarantor accepts unlimited liability for the debtor's obligations, ensuring that the creditor can pursue any and all assets of the guarantor to satisfy the debt. This type of guaranty typically provides the creditor with the highest level of security. 2. Limited Personal Guaranty: Unlike the unlimited personal guaranty, the limited personal guaranty places a cap on the guarantor's liability. The guarantor is responsible only for a specific amount or a defined portion of the debtor's obligations, limiting the creditor's ability to recover beyond the agreed-upon limit. This type is often utilized when the guarantor is willing to support the debtor but wishes to restrict their personal liability. Both types of Louisiana Personal Guaranty — General serve as crucial risk management tools for creditors, as they provide an extra layer of protection in case the debtor defaults on their obligations. It is essential for both the guarantor and the creditor to carefully review and negotiate the terms of the personal guaranty. The document should clearly specify the obligations covered, the conditions triggering the guarantor's liability, any limitation put on the guarantor's liability, and the rights and remedies available to the creditor in case of default. In summary, a Louisiana Personal Guaranty — General is a legally-binding agreement that holds an individual liable for the debts or obligations of another party. The guaranty provides creditors with additional security and allows them to pursue the guarantor's personal assets in case of default. By distinguishing between unlimited and limited personal guaranties, individuals can tailor their level of liability to suit their specific circumstances while still providing support for the debtor.

Louisiana Personal Guaranty - General

Description

How to fill out Louisiana Personal Guaranty - General?

US Legal Forms - one of several greatest libraries of lawful types in the States - delivers a wide array of lawful record themes you may acquire or print out. Using the site, you can get a large number of types for enterprise and individual functions, sorted by categories, claims, or keywords and phrases.You can get the most recent versions of types much like the Louisiana Personal Guaranty - General in seconds.

If you currently have a subscription, log in and acquire Louisiana Personal Guaranty - General from your US Legal Forms catalogue. The Down load option will show up on every single type you perspective. You have accessibility to all earlier downloaded types in the My Forms tab of your profile.

If you want to use US Legal Forms the very first time, listed below are basic instructions to get you started:

- Ensure you have chosen the right type for your city/state. Click the Preview option to examine the form`s content. See the type explanation to ensure that you have selected the correct type.

- When the type doesn`t match your requirements, utilize the Search area on top of the screen to obtain the one that does.

- Should you be satisfied with the form, confirm your selection by clicking on the Acquire now option. Then, choose the costs plan you want and offer your qualifications to register for the profile.

- Method the purchase. Use your credit card or PayPal profile to complete the purchase.

- Find the structure and acquire the form on your own product.

- Make adjustments. Fill out, modify and print out and signal the downloaded Louisiana Personal Guaranty - General.

Each and every web template you included with your account lacks an expiration particular date and it is your own eternally. So, if you would like acquire or print out one more version, just check out the My Forms area and then click about the type you require.

Obtain access to the Louisiana Personal Guaranty - General with US Legal Forms, probably the most comprehensive catalogue of lawful record themes. Use a large number of expert and condition-specific themes that meet your company or individual requires and requirements.