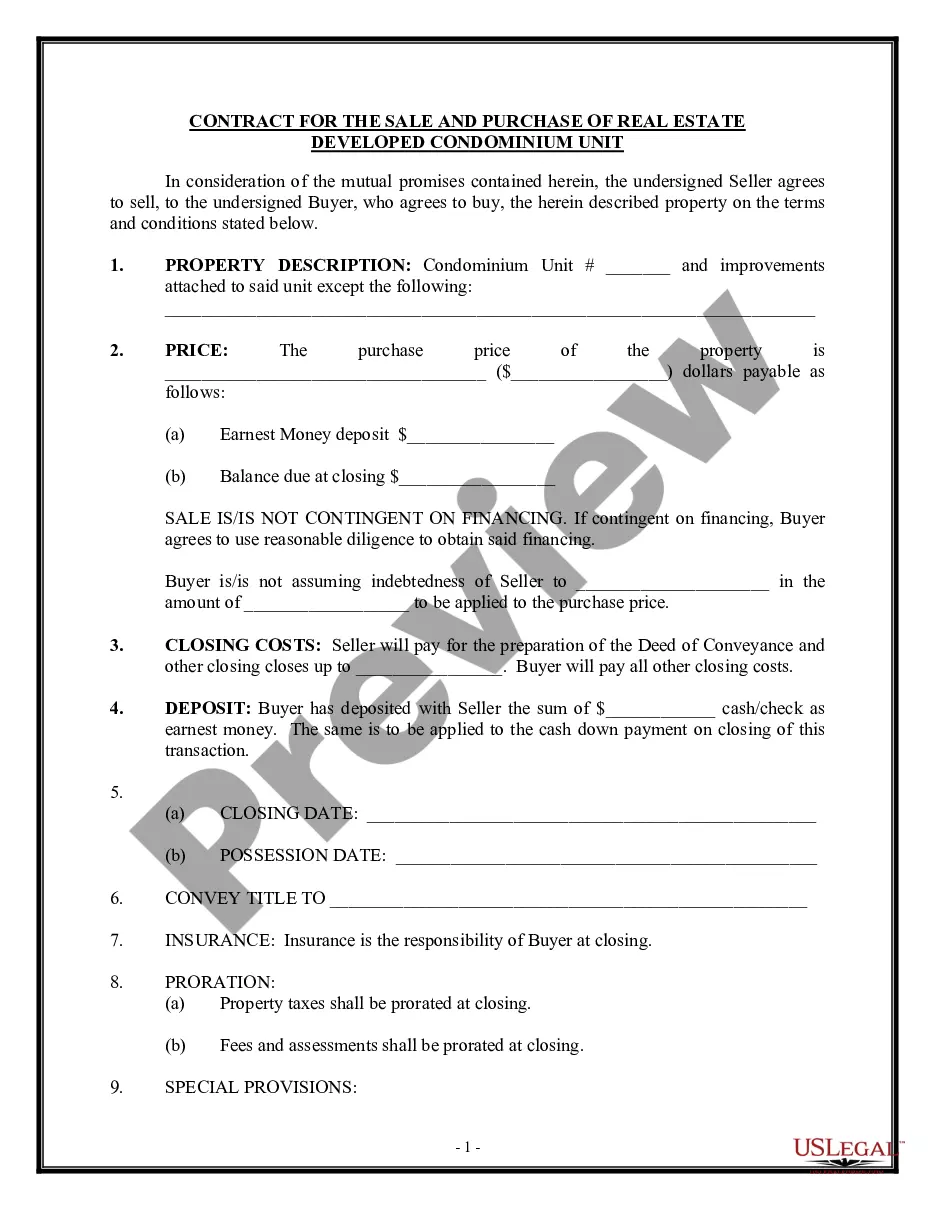

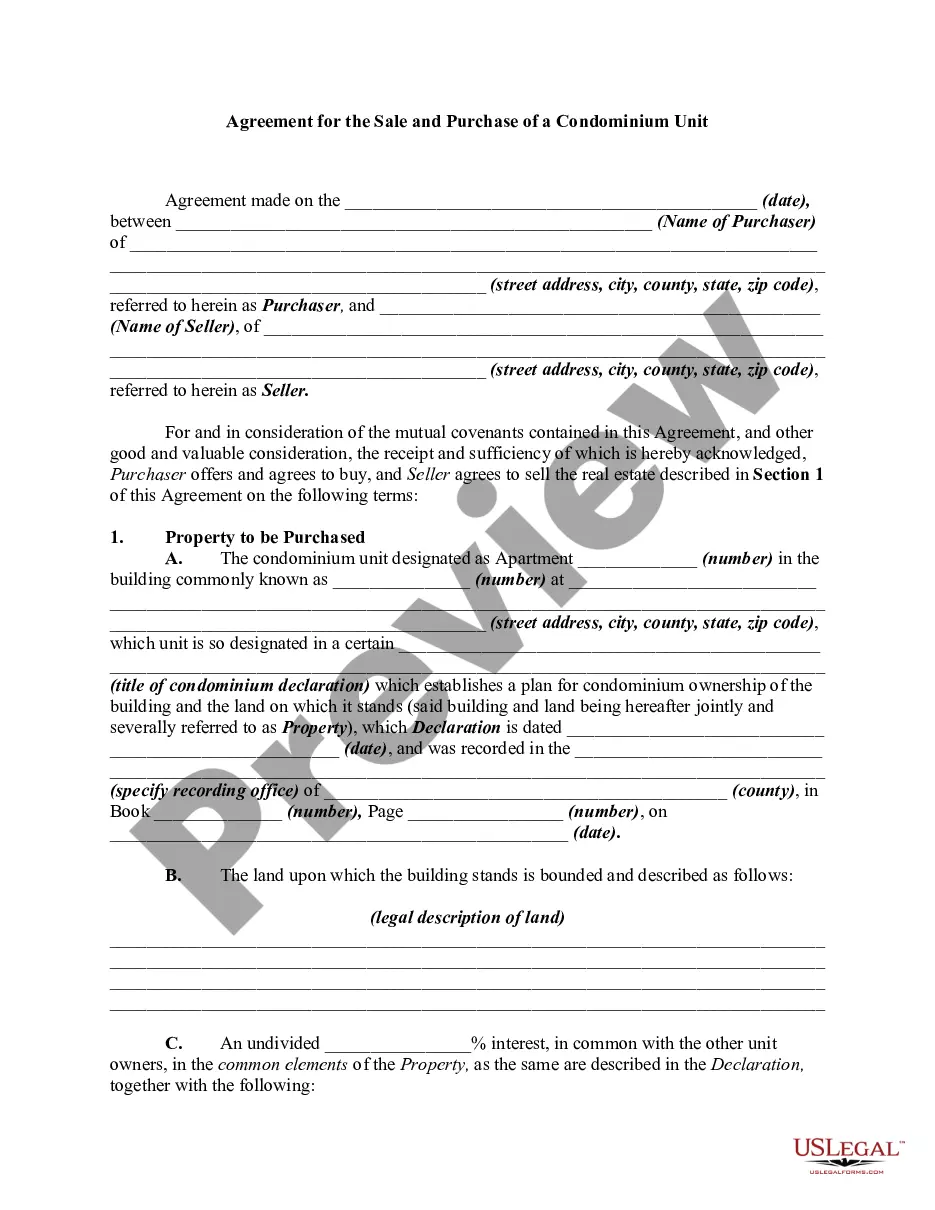

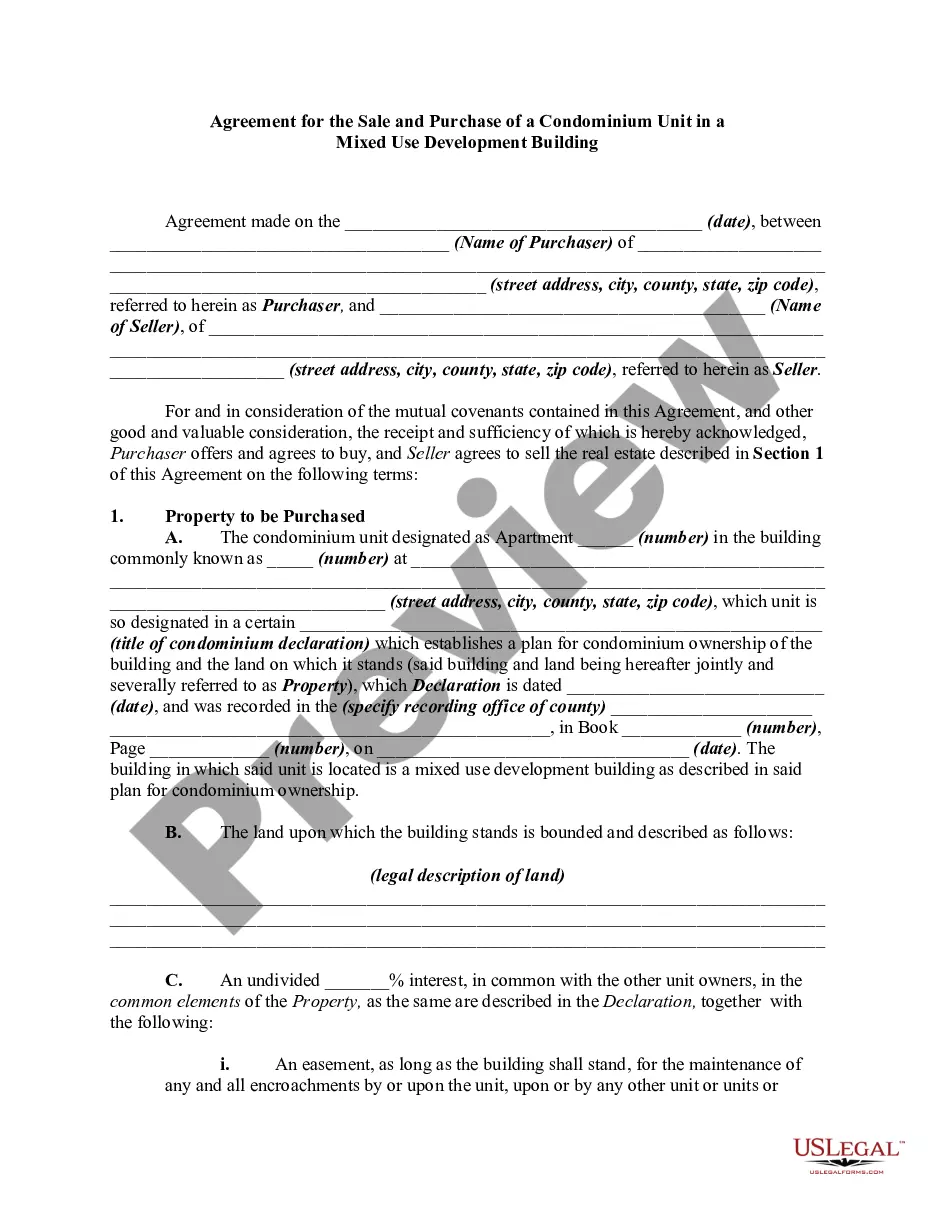

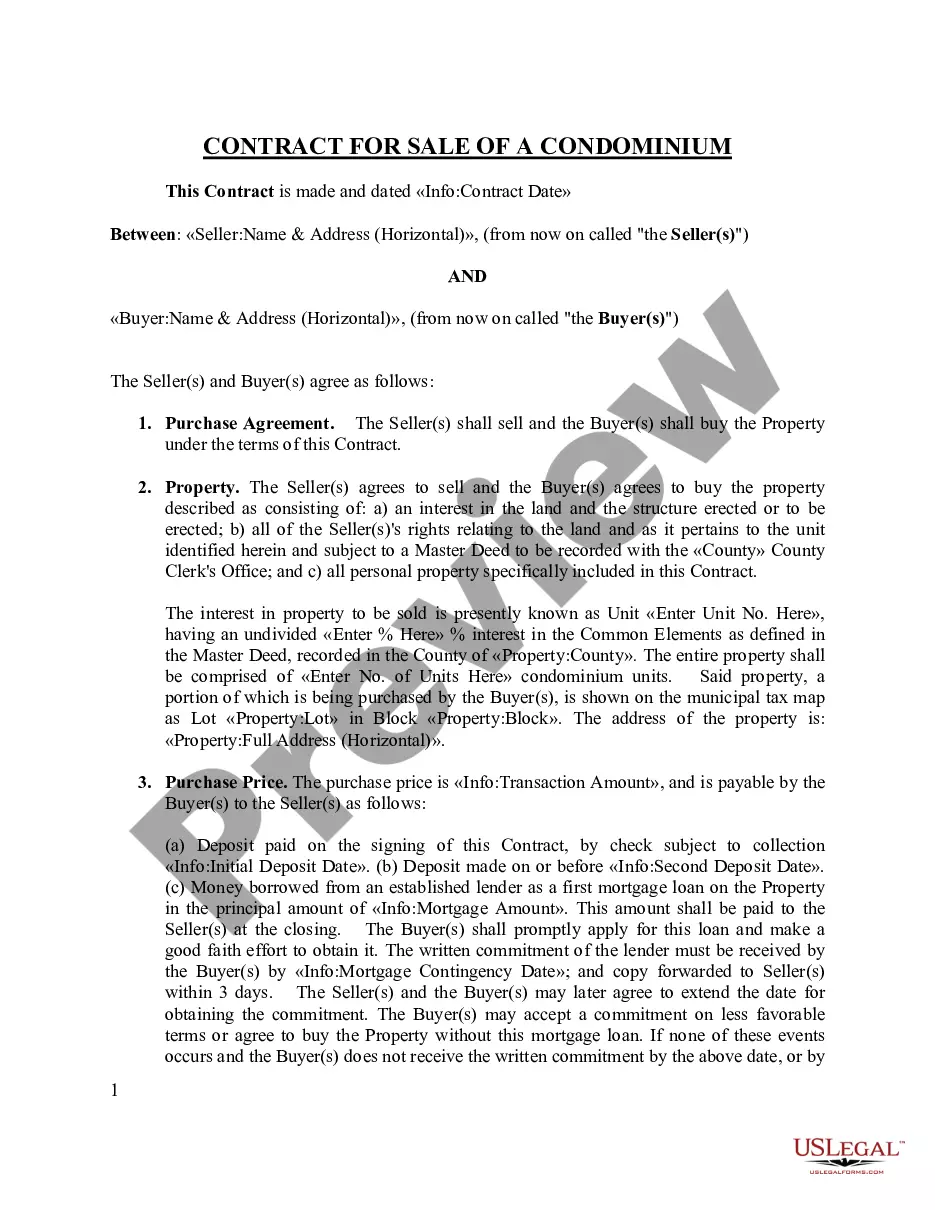

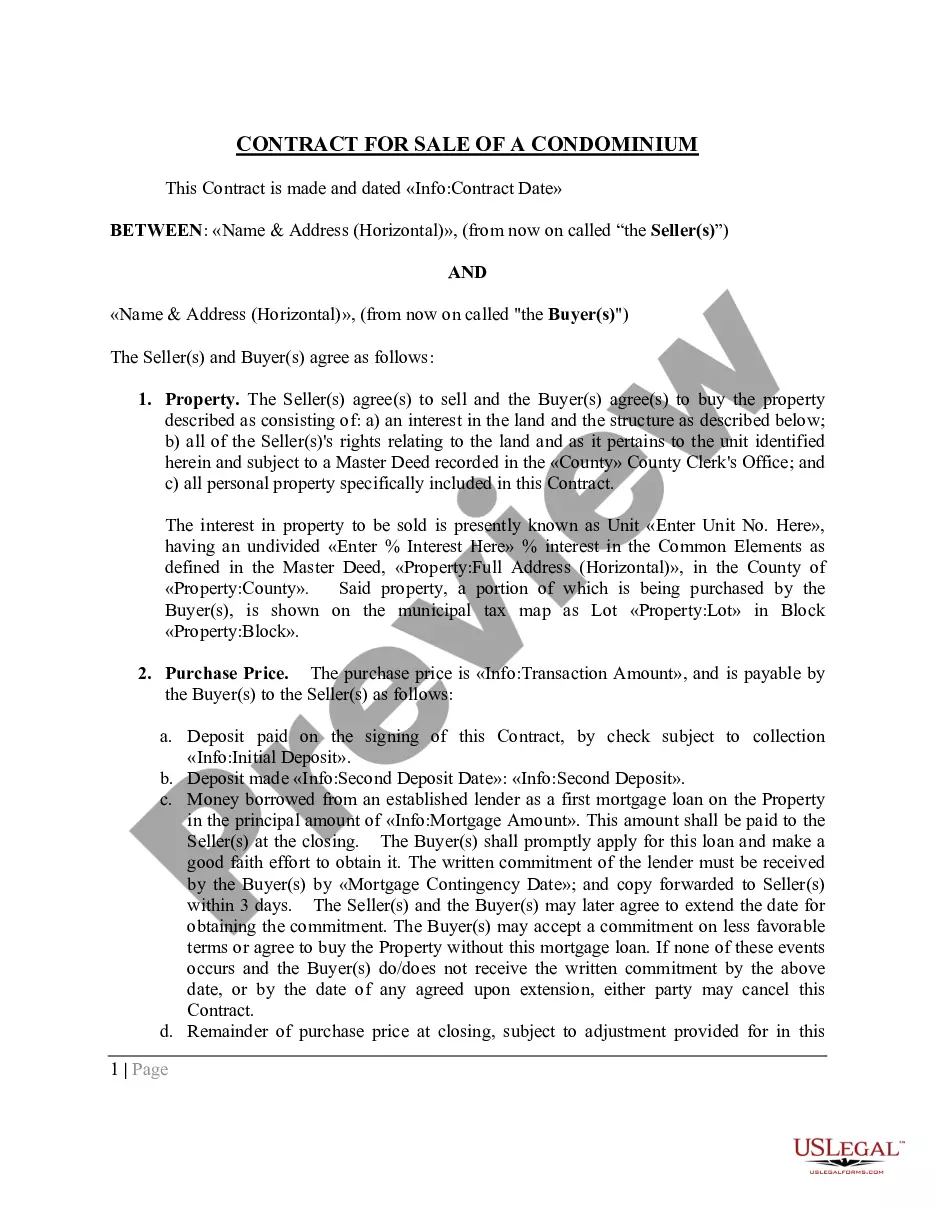

Louisiana Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement To Purchase Condominium With Purchase Money Mortgage Financing By Seller, And Subject To Existing Mortgage?

It is feasible to spend hours online trying to locate the legal document template that meets the federal and state criteria you require. US Legal Forms offers numerous legal forms that are reviewed by experts.

You can easily obtain or print the Louisiana Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage from our service. If you have a US Legal Forms account, you can Log In and click the Download button.

After that, you can complete, edit, print, or sign the Louisiana Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage. Every legal document template you purchase is yours indefinitely.

Select the pricing plan you prefer, enter your credentials, and register for an account on US Legal Forms. Complete the transaction. You can use your credit card or PayPal account to pay for the legal form. Choose the format of your document and download it to your device. Make adjustments to your document if necessary. You can complete, edit, sign, and print the Louisiana Agreement to Purchase Condominium with Purchase Money Mortgage Financing by Seller, and Subject to Existing Mortgage. Download and print numerous document templates using the US Legal Forms website, which offers the largest collection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- To get another copy of a purchased form, visit the My documents tab and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for your area/city of your choice.

- Review the form description to ensure you have chosen the correct form.

- If available, use the Preview button to look through the document template as well.

- If you wish to find another version of your form, use the Search field to obtain the template that suits your needs and requirements.

- Once you have located the template you need, click Purchase now to proceed.

Form popularity

FAQ

Disadvantages of subject-to loans Some mortgage companies call loans due if the property transfers to a new buyer. You may lose the house if you do not have the cash to pay off the mortgage and cannot get financing in your name. Finally, insuring the home can be very challenging.

For most homebuyers, the primary reason for buying subject-to properties is to take over the seller's existing interest rate. If present interest rates are at 4% and a seller has a 2% fixed interest rate, that 2% variance can make a huge difference in the buyer's monthly payment.

That said, there are two common reasons a homeowner would consider using a subject to mortgage strategy: they either can't sell at the price they want, or they need to sell sooner rather than later. The former reason would suggest the homeowner has little to no equity and need to sell at a certain price?no exceptions.

Buying a subject-to home is attractive to buyers if they can get a lower interest rate by taking over payments. This arrangement poses risks for the buyer if the lender requires a full loan payoff or if the seller goes into bankruptcy.

"Subject-To" is a way of purchasing real estate where the real estate investor takes title to the property but the existing loan stays in the name of the seller. In other words, "Subject-To" the existing financing. The investor now controls the property and makes the mortgage payments on the seller's existing mortgage.

For sellers, subject to is a good way to quickly dispose of a property if you need immediate debt relief or if you're facing foreclosure. Foreclosure is a major risk for buyers and sellers participating in a subject to, and it's generally a high-risk investment.

Wrap-Around ?Subject To? The seller usually has to pay interest rates on their mortgage to their lender, so they in turn ask the investor for an additional, proportional interest rate. For example, if the original homeowner's mortgage is at 4%, then the seller might ask for 6% from the carryback from the investor.

Although the buyer makes the mortgage payments, the seller remains responsible for the loan. When the property is sold subject to the loan the buyer is not liable to pay the lender, the original borrower is still primarily liable to the lender.