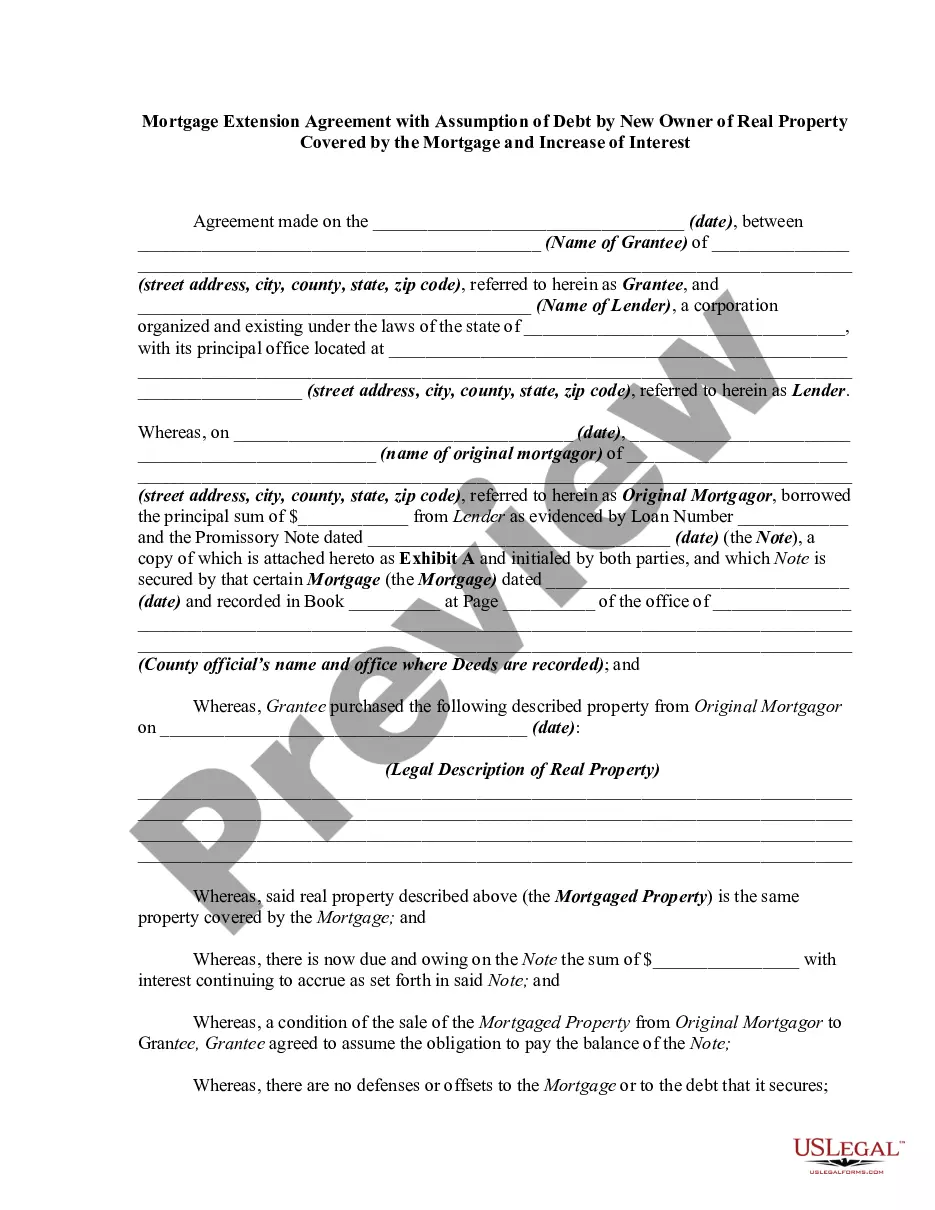

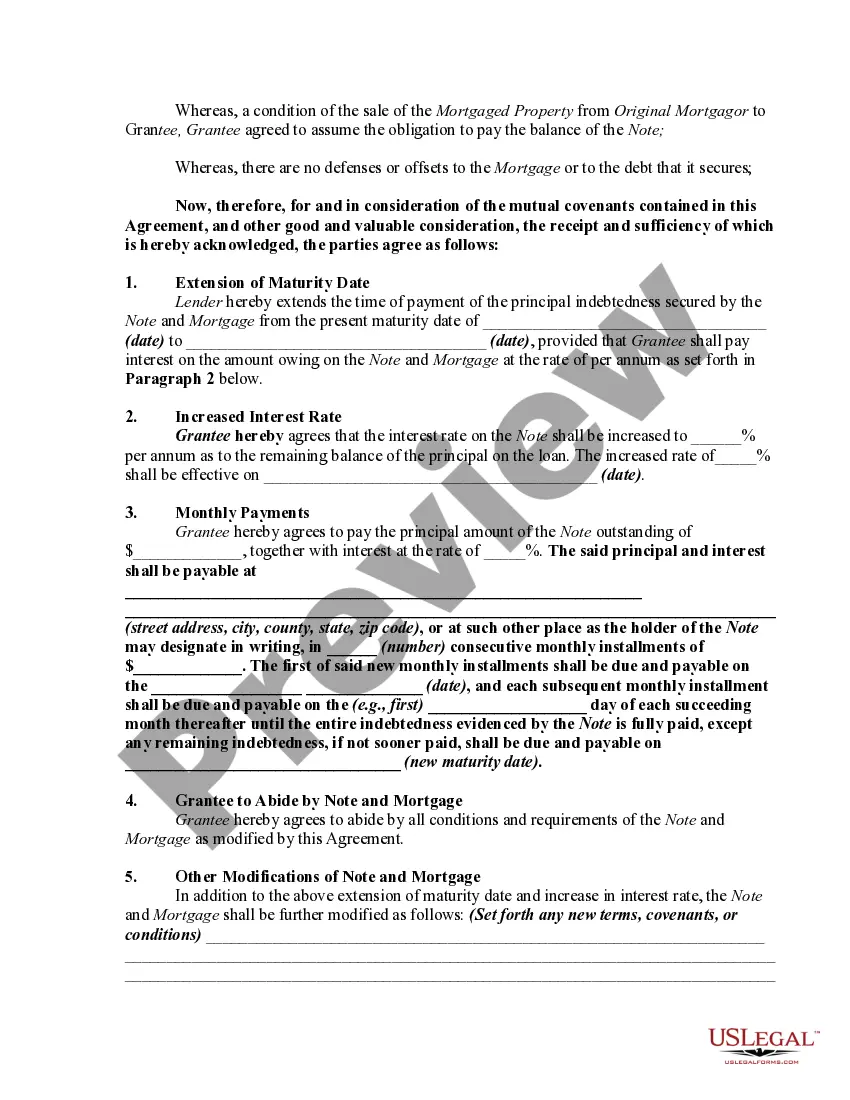

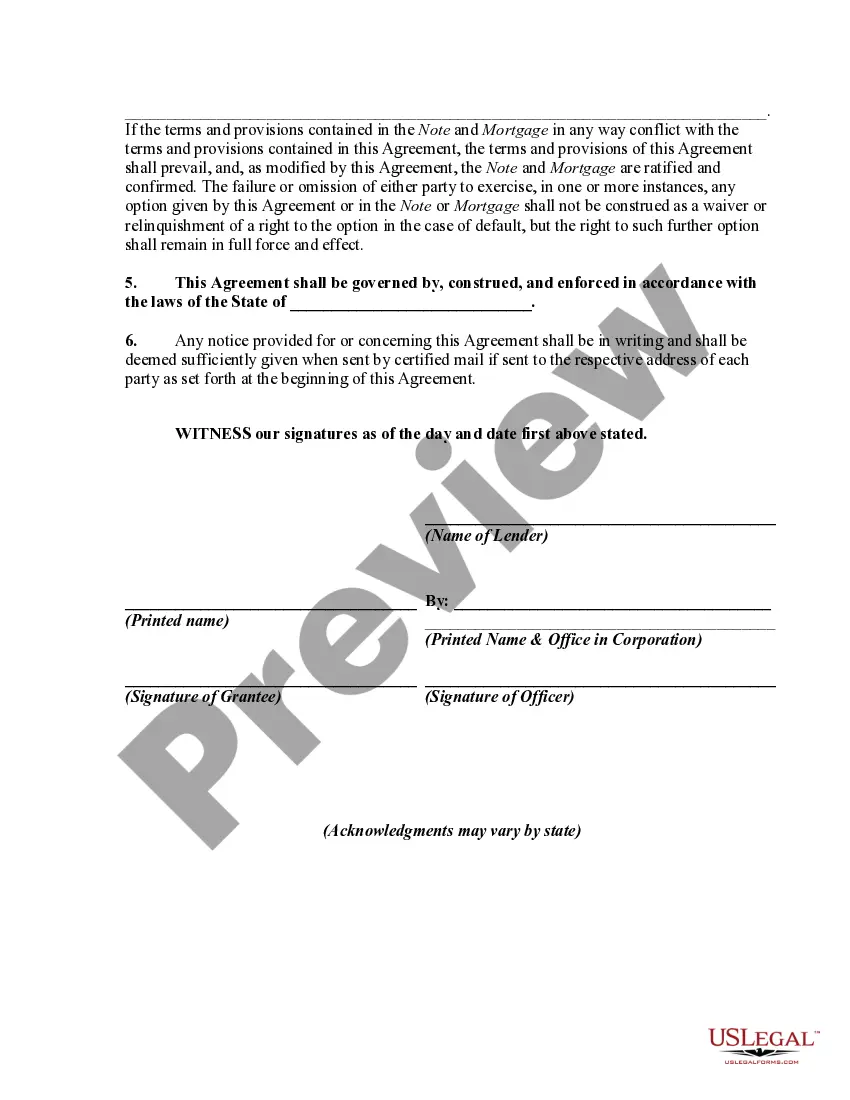

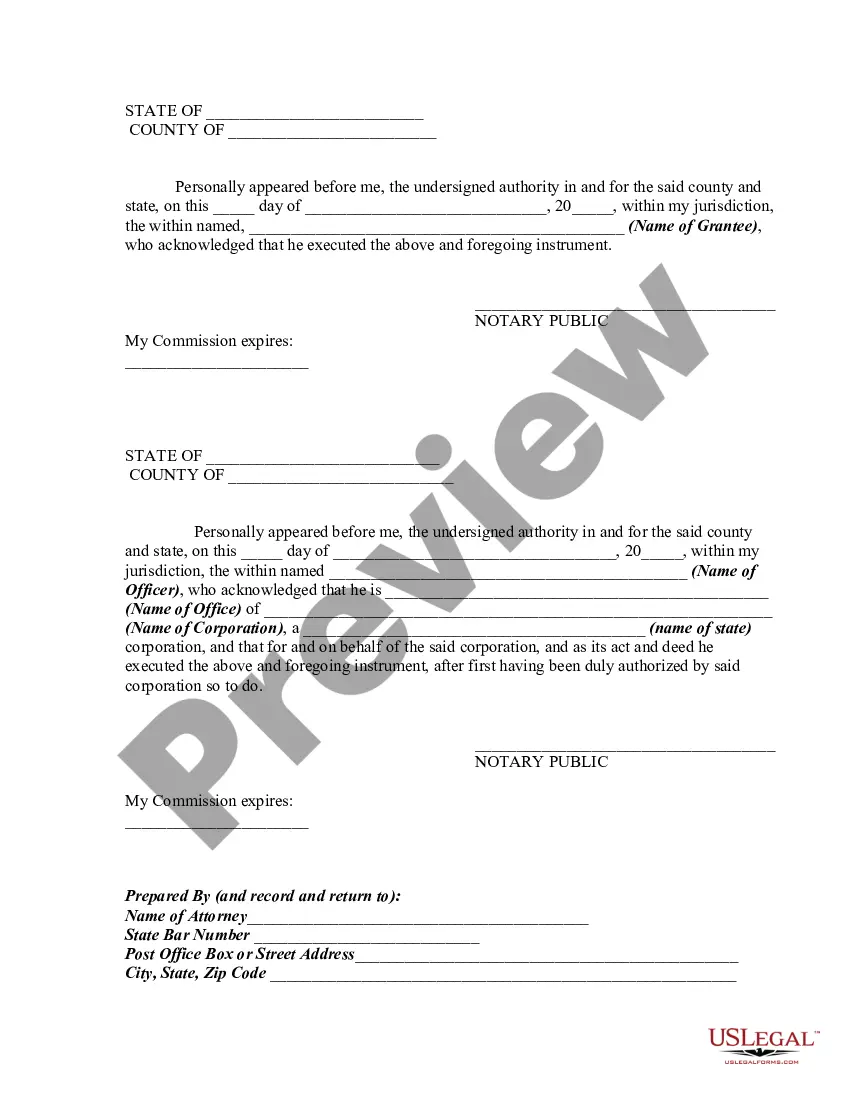

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Louisiana Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest refers to a legal document executed in Louisiana that allows a new owner of a real property, which is covered by an existing mortgage, to assume the debt and extend the mortgage agreement while also negotiating an increase in the interest rate. This agreement is commonly used in real estate transactions where a new owner is willing to assume the mortgage obligations and extend the duration of the loan while also adjusting the interest rate. The key components of a Louisiana Mortgage Extension Agreement with Assumption of Debt are as follows: 1. Parties involved: The agreement identifies the parties involved, including the current property owner, the new owner, and the mortgage lender. Each party's full legal names and contact information are typically included. 2. Property details: The agreement provides a detailed description of the real property, including the address, legal description, and any relevant tax identification numbers or references to prior deeds. 3. Existing mortgage terms: The agreement outlines the original terms of the mortgage, including the loan amount, interest rate, repayment period, and any other essential terms and conditions. 4. Assumption of debt: The new owner agrees to assume all existing mortgage obligations, including the outstanding principal balance, interest, and any other fees or charges associated with the loan. This clause ensures that the new owner is legally responsible for the debt. 5. Extension of mortgage: The agreement establishes the new duration of the mortgage, which may be extended beyond the original term. Both parties negotiate and agree on the extended length of the loan, ensuring that all future payments and obligations are accounted for. 6. Increase of interest: This clause addresses any changes in the interest rate. The agreement specifies the revised interest rate agreed upon by the parties. This increase in the interest rate usually reflects the potentially higher risk faced by the lender when a new owner assumes the mortgage debt. 7. Terms and conditions: The agreement sets forth any additional terms and conditions that are relevant to the extension of the mortgage and assumption of debt, such as late payment penalties, default provisions, or any other requirements set by the lender. Different types or variations of a Louisiana Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest may include: 1. Partial assumption: In some cases, the new owner assumes only a portion of the original mortgage debt. This may occur when the new owner provides a down payment or has additional financing sources to cover a percentage of the property purchase. 2. Adjustable-rate extension: Instead of negotiating an increase in the interest rate, the parties may agree to extend the mortgage term with an adjustable interest rate. This means that the interest rate can fluctuate based on market conditions or other agreed-upon factors. 3. Balloon payment extension: If the original mortgage agreement included a balloon payment, the parties may agree to extend the loan term while maintaining the balloon payment provision. This allows the new owner to make smaller monthly payments but requires a substantial final payment at the end of the extended term. In conclusion, a Louisiana Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest is a legal document that allows a new owner to assume an existing mortgage, extend the loan term, and negotiate an increase in the interest rate. This agreement ensures a smooth transfer of ownership while protecting the rights and obligations of all parties involved in the real estate transaction.