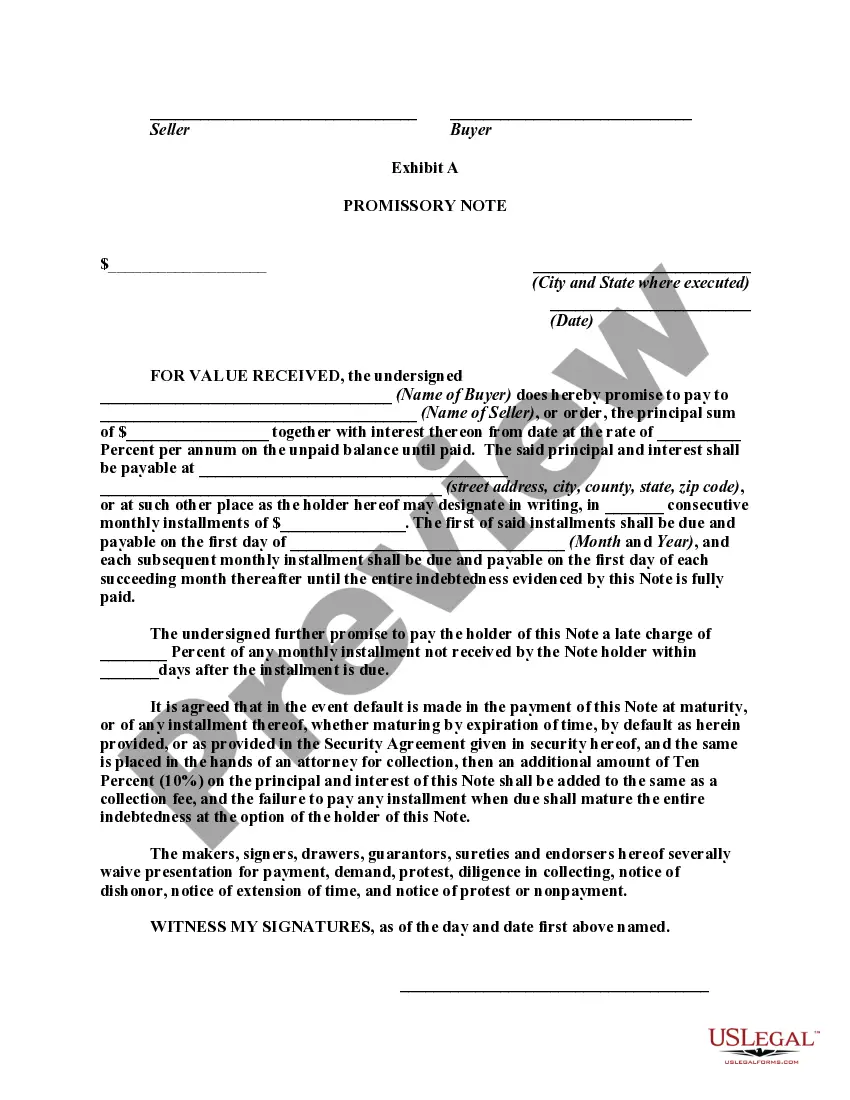

A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

A secured transaction involves a sale on credit or lending money where a creditor is unwilling to accept the promise of a debtor to pay an obligation without some sort of collateral. The creditor requires the debtor to secure the obligation with collateral so that if the debtor does not pay as promised, the creditor can take the collateral, sell it, and apply the proceeds against the unpaid obligation of the debtor.

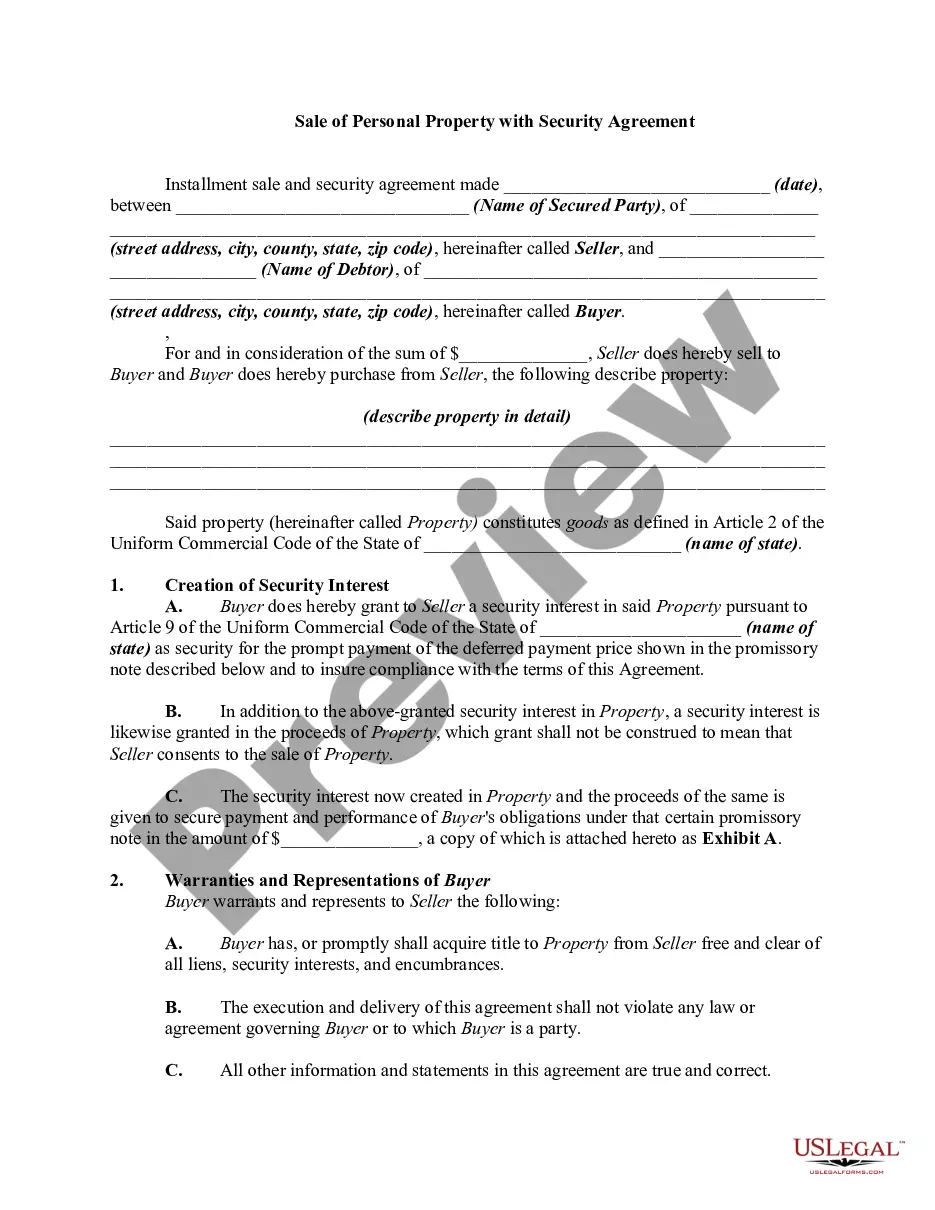

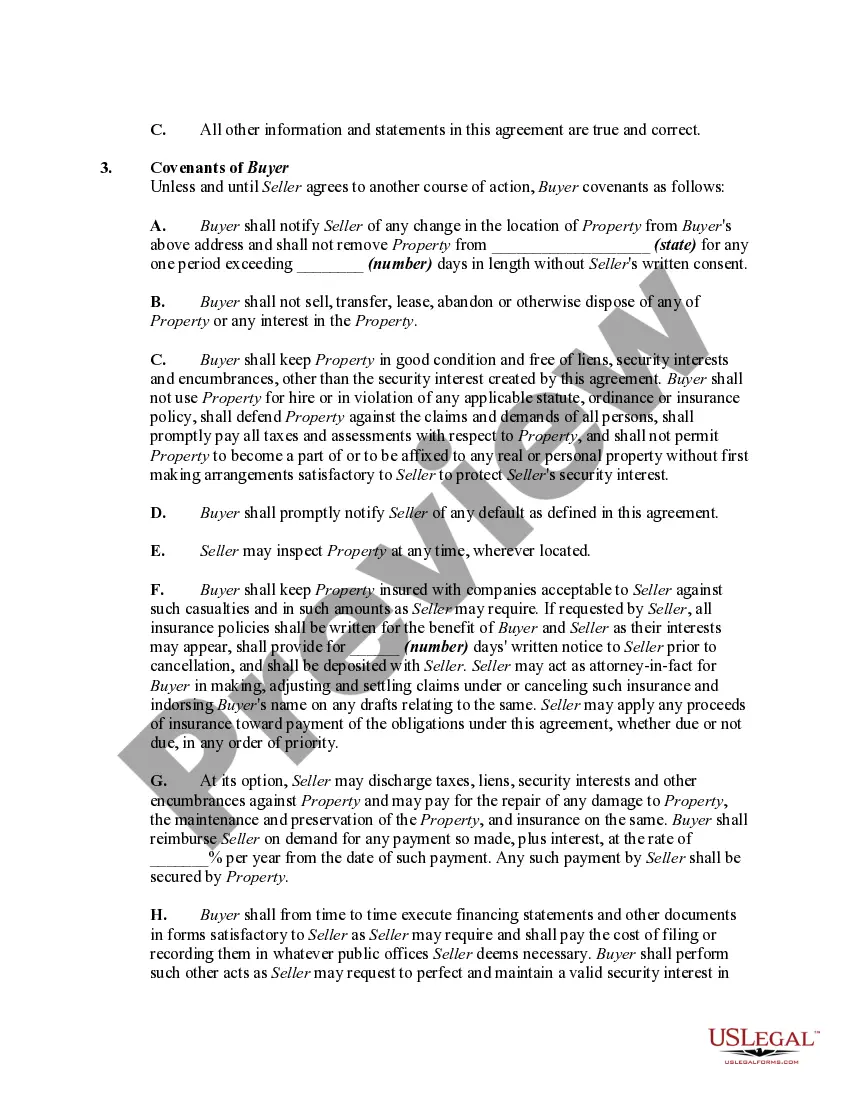

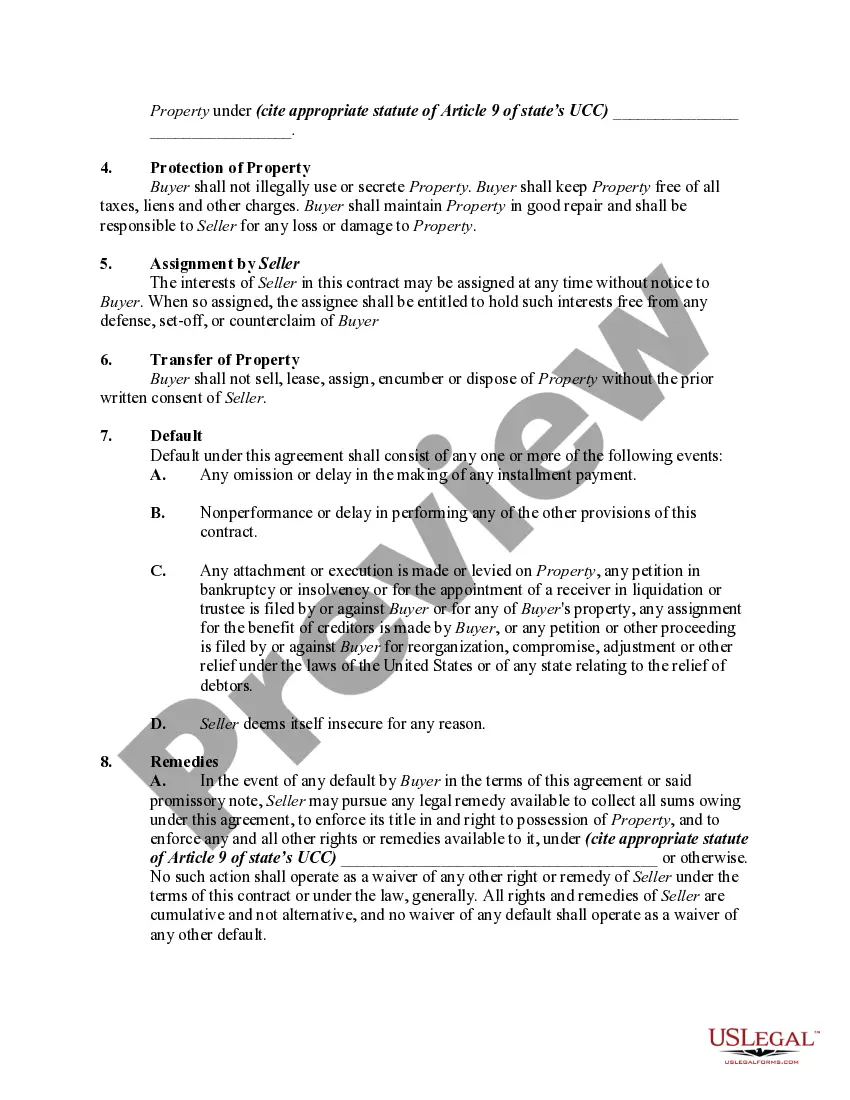

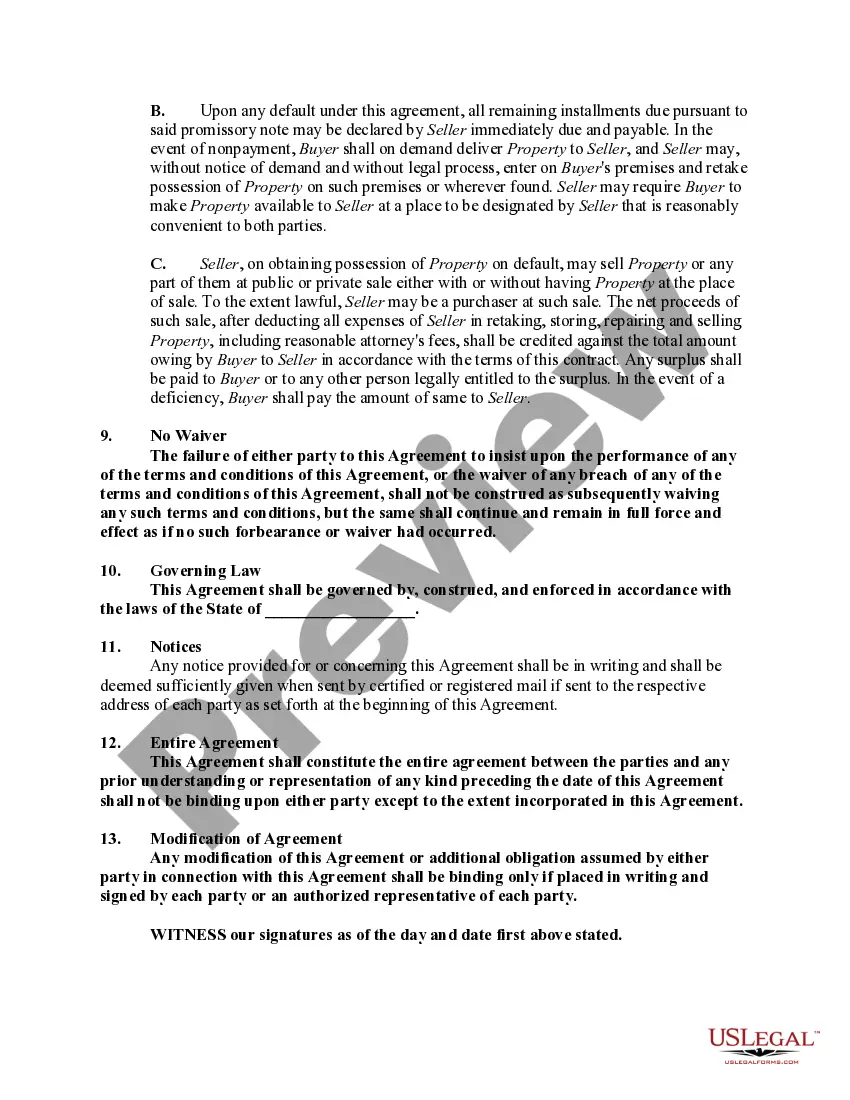

The Louisiana Sale of Personal Property with Security Agreement is a legal document that outlines the terms and conditions for the sale of personal property in the state of Louisiana. It provides both the buyer and the seller with protection and lays out their rights and obligations during the transaction. This type of agreement is commonly used when a seller wants to sell personal property, such as vehicles, machinery, or other valuable goods, and wants to ensure that if the buyer fails to make the payments as agreed, they have the right to repossess the property to recover their losses. The Louisiana Sale of Personal Property with Security Agreement includes several key components. First, it clearly identifies the parties involved — the seller, who is the owner of the property, and the buyer, who is purchasing the property. Their full legal names and contact information are stated in the agreement. The agreement also describes the personal property being sold, providing a detailed description of the items, including their make, model, serial numbers, and any other relevant identifiers. This ensures that there is no confusion about the specific items being sold. Payment terms are an essential part of this agreement. It outlines the purchase price of the personal property and how the buyer will make payments to the seller. The agreement may specify the amount of the down payment, the installment amounts, and the due dates for each payment. To secure the payment, the agreement establishes a security interest in the personal property being sold. This means that the seller has a legal right to repossess the property if the buyer defaults on the payments. The agreement may also include specific provisions regarding default, repossession process, and remedies available to the seller in case of default. Additional provisions can be included in the Louisiana Sale of Personal Property with Security Agreement to address specific circumstances or conditions. For example, the agreement might include clauses regarding insurance requirements, maintenance responsibilities, or even dispute resolution methods. Different types of Louisiana Sale of Personal Property with Security Agreement can include agreements for the sale of motor vehicles, furniture, electronics, or any other form of personal property. While the basic structure and purpose remain the same, the specific terms and conditions may vary depending on the type of property being sold. In conclusion, the Louisiana Sale of Personal Property with Security Agreement is an important legal document that protects both the buyer and the seller in a sale transaction. It ensures that the buyer receives the personal property they paid for, while the seller has the means to recover their losses if the buyer defaults on the agreed payments.The Louisiana Sale of Personal Property with Security Agreement is a legal document that outlines the terms and conditions for the sale of personal property in the state of Louisiana. It provides both the buyer and the seller with protection and lays out their rights and obligations during the transaction. This type of agreement is commonly used when a seller wants to sell personal property, such as vehicles, machinery, or other valuable goods, and wants to ensure that if the buyer fails to make the payments as agreed, they have the right to repossess the property to recover their losses. The Louisiana Sale of Personal Property with Security Agreement includes several key components. First, it clearly identifies the parties involved — the seller, who is the owner of the property, and the buyer, who is purchasing the property. Their full legal names and contact information are stated in the agreement. The agreement also describes the personal property being sold, providing a detailed description of the items, including their make, model, serial numbers, and any other relevant identifiers. This ensures that there is no confusion about the specific items being sold. Payment terms are an essential part of this agreement. It outlines the purchase price of the personal property and how the buyer will make payments to the seller. The agreement may specify the amount of the down payment, the installment amounts, and the due dates for each payment. To secure the payment, the agreement establishes a security interest in the personal property being sold. This means that the seller has a legal right to repossess the property if the buyer defaults on the payments. The agreement may also include specific provisions regarding default, repossession process, and remedies available to the seller in case of default. Additional provisions can be included in the Louisiana Sale of Personal Property with Security Agreement to address specific circumstances or conditions. For example, the agreement might include clauses regarding insurance requirements, maintenance responsibilities, or even dispute resolution methods. Different types of Louisiana Sale of Personal Property with Security Agreement can include agreements for the sale of motor vehicles, furniture, electronics, or any other form of personal property. While the basic structure and purpose remain the same, the specific terms and conditions may vary depending on the type of property being sold. In conclusion, the Louisiana Sale of Personal Property with Security Agreement is an important legal document that protects both the buyer and the seller in a sale transaction. It ensures that the buyer receives the personal property they paid for, while the seller has the means to recover their losses if the buyer defaults on the agreed payments.