A trustor is the person who creates a trust. A trustor is also called a grantor, donor or settlor. A trust is a separate legal entity that holds property or assets of some kind for the benefit of a specific person, group of people or organization known as the beneficiary/beneficiaries. When a trust is established, an individual or corporate entity is named to oversee or manage the assets in the trust. This individual or entity is called a trustee. A trustee can be a professional with financial knowledge, a relative or loyal friend or a corporation. More than one trustee can be named by the trustor.

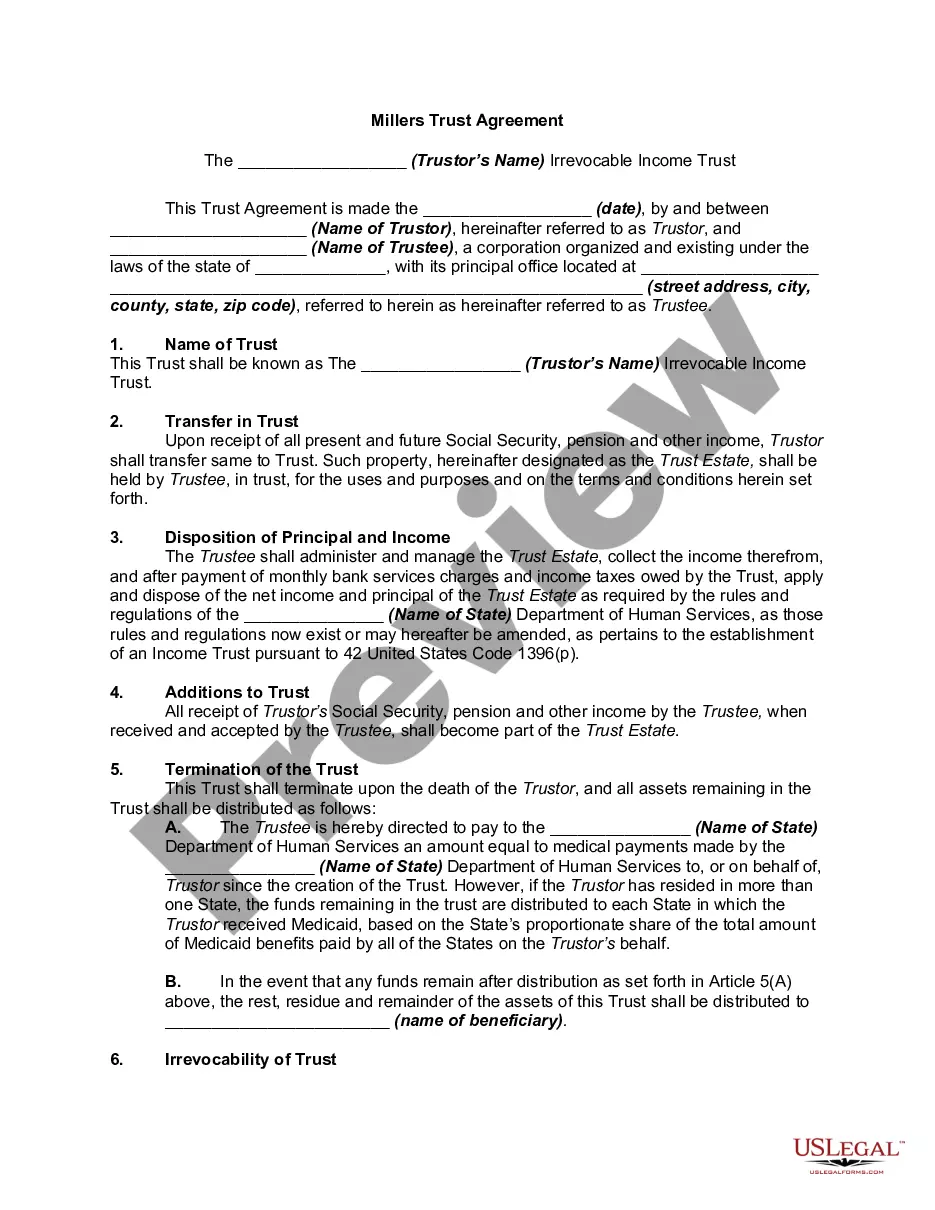

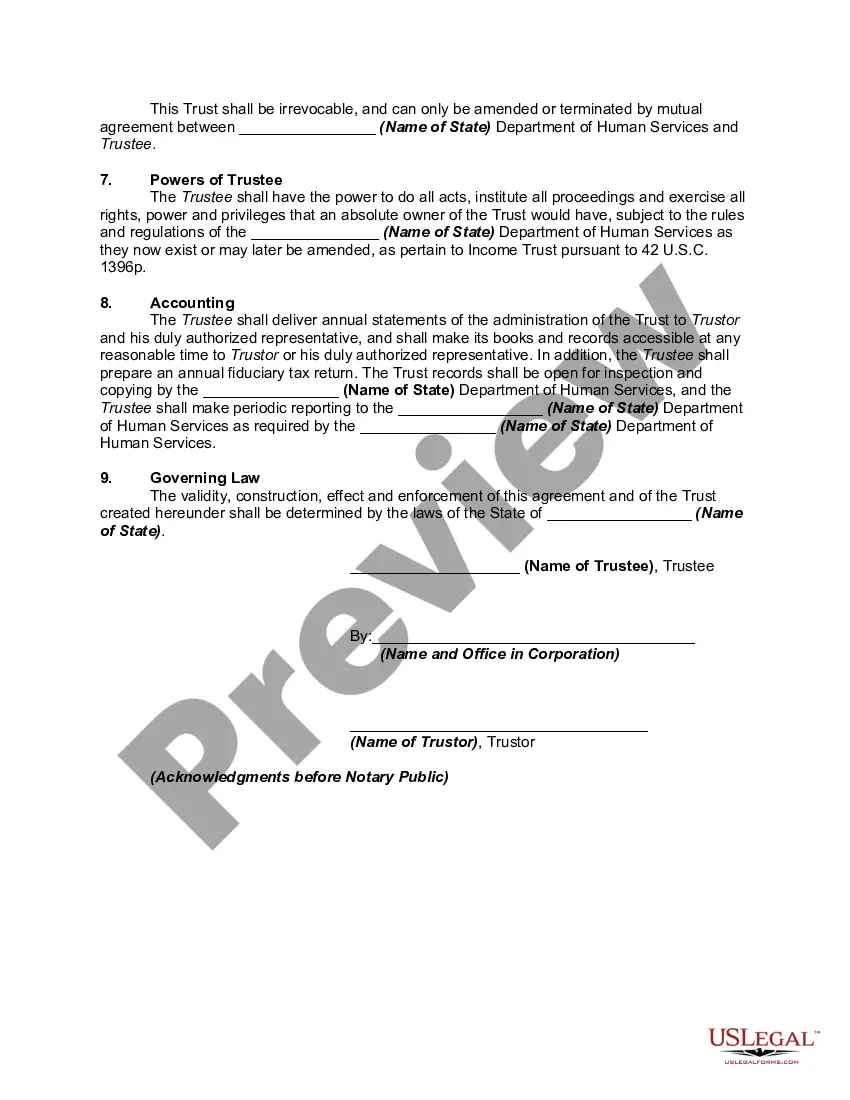

The qualified Medicaid income trust is a legal instrument which meets criteria in 42 United States Code 1396(p) and which allows individuals with income over the institutional care program limits to qualify for institutional care services or for home and community based services assistance.

A Medicaid trust may take various forms and laws vary by state. There are differing requirements under state laws regarding what assets may be counted or reached for recovery upon death. To comply with applicable requirements, professional financial advice should be sought. The term "Miller Trust" is an informal name. A more accurate name for this trust is an "Income Cap Trust". It has also been called an Income Assignment Trust. This is because, after the trust is created, the patient assigns his or her right to receive social security and pension to the trust.

The Louisiana Qualified Income Miller Trust, also commonly known as QIT, is a specialized legal instrument utilized to help individuals meet the income threshold requirements for Medicaid eligibility in the state of Louisiana. A QIT is specifically designed for elderly or disabled individuals who have excess income that surpasses Medicaid's income limit. The primary purpose of a Louisiana Qualified Income Miller Trust is to "qualify" or restructure an individual's income in such a way that it becomes permissible under Medicaid guidelines. By establishing this trust, the excess income is placed into the trust, thereby reducing the individual's countable income to meet the eligibility criteria. There are different types of Louisiana Qualified Income Miller Trusts, such as the Sole Benefit Trust and the Pooled Trust. 1. Sole Benefit Trust: This type of QIT is established solely for the benefit of the Medicaid applicant. It allows the individual to deposit their excess income into a trust account, which is then used to pay for their medical expenses and other approved costs of care. The individual must be the sole beneficiary of this trust, meaning that any remaining funds after their passing cannot be distributed to heirs or beneficiaries. 2. Pooled Trust: A Pooled Trust operates similarly to a Sole Benefit Trust but is managed by a nonprofit organization. These trusts pool together the resources of multiple Medicaid beneficiaries with disabilities. The trust funds are then managed and used for the benefit of each individual participant in accordance with Medicaid guidelines. Unlike the Sole Benefit Trust, any remaining funds in the Pooled Trust can be retained by the nonprofit organization to benefit other trust participants or for charitable purposes. The Louisiana Qualified Income Miller Trust is an essential tool for individuals who exceed the income limits for Medicaid eligibility but still require vital healthcare services. It allows them to restructure their income and qualify for Medicaid while ensuring that the excess income is dedicated to covering necessary medical expenses. By understanding the different types of Its available, individuals and their families can make informed decisions regarding their financial and healthcare planning.