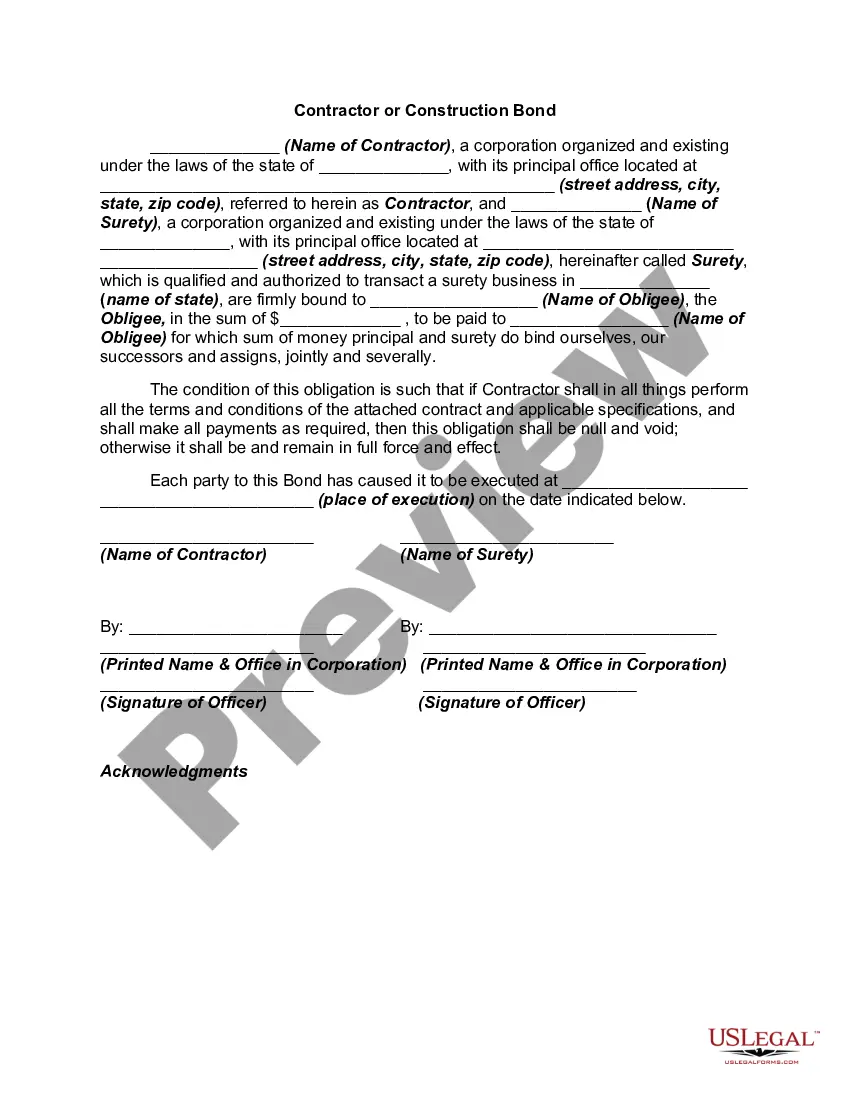

A Surety makes itself liable for another's debts, defaults or obligations, etc. In other words, it is acting as a co-signer or guarantor for a specific deposit, performance or contract. A performance bond is a non-cancelable commitment issued by the surety to the owner of the project (obligee) guaranteeing that the contractor will complete the referenced contract within its set terms and conditions. The surety is in effect co-signing the contract. A payment bond guarantees that all sub contractors, labor and material suppliers will be paid leaving the project lien free. required to post a bond in case of any losses incurred as a result of their work or failure to complete work on the contract for the project. The bond serves as an insurance policy to the property owner or other party who may incur such loss.

A Louisiana contractor or construction bond is a legal agreement between three parties: the contractor, the project owner (also known as the obliged), and a surety bond company. It is a necessary requirement for contractors in Louisiana to obtain bonding before undertaking certain construction projects. The purpose of this bond is to protect the project owner and ensure the contractor fulfills their contractual obligations. There are several types of contractor or construction bonds available in Louisiana, each serving a specific purpose. Here are some of the most common ones: 1. Bid Bond: This type of bond guarantees that if the contractor is awarded a project after winning the bid, they will enter into a contract and provide the required performance and payment bonds. It ensures that the bidding contractor will not back out of the project after being awarded. 2. Performance Bond: This bond guarantees that the contractor will complete the project according to the agreed-upon terms and specifications. If the contractor fails to complete the project, the bonding company will compensate the project owner for the losses incurred up to the bond's limit. 3. Payment Bond: A payment bond guarantees that the contractor will pay all subcontractors, suppliers, and laborers involved in the project. If the contractor fails to make the necessary payments, the bonding company will cover the outstanding amounts. 4. Maintenance Bond: This bond ensures that the contractor will correct any defects or issues in their workmanship or materials even after the project's completion. It typically covers a specific duration after the project is finished. 5. Supply Bond: In cases where a contractor is responsible for the supply of materials or equipment, a supply bond guarantees that they will deliver the specified goods according to the agreed-upon terms. 6. Subdivision Bond: This bond is required for contractors engaged in developing subdivisions or residential areas. It guarantees that the contractor will take care of needed infrastructure improvements, such as roads, utilities, and drainage, within the given timeline. 7. License and Permit Bond: This bond is necessary to obtain or renew a contractor's license in Louisiana. It ensures that the contractor will comply with all applicable laws, regulations, and building codes. These Louisiana contractor or construction bonds provide additional security to the project owner, ensuring that they have recourse if the contractor fails to meet their obligations. Obtaining the appropriate bond is an essential step for contractors in Louisiana to gain credibility, increase their chances of winning bids, and protect their reputation in the industry.A Louisiana contractor or construction bond is a legal agreement between three parties: the contractor, the project owner (also known as the obliged), and a surety bond company. It is a necessary requirement for contractors in Louisiana to obtain bonding before undertaking certain construction projects. The purpose of this bond is to protect the project owner and ensure the contractor fulfills their contractual obligations. There are several types of contractor or construction bonds available in Louisiana, each serving a specific purpose. Here are some of the most common ones: 1. Bid Bond: This type of bond guarantees that if the contractor is awarded a project after winning the bid, they will enter into a contract and provide the required performance and payment bonds. It ensures that the bidding contractor will not back out of the project after being awarded. 2. Performance Bond: This bond guarantees that the contractor will complete the project according to the agreed-upon terms and specifications. If the contractor fails to complete the project, the bonding company will compensate the project owner for the losses incurred up to the bond's limit. 3. Payment Bond: A payment bond guarantees that the contractor will pay all subcontractors, suppliers, and laborers involved in the project. If the contractor fails to make the necessary payments, the bonding company will cover the outstanding amounts. 4. Maintenance Bond: This bond ensures that the contractor will correct any defects or issues in their workmanship or materials even after the project's completion. It typically covers a specific duration after the project is finished. 5. Supply Bond: In cases where a contractor is responsible for the supply of materials or equipment, a supply bond guarantees that they will deliver the specified goods according to the agreed-upon terms. 6. Subdivision Bond: This bond is required for contractors engaged in developing subdivisions or residential areas. It guarantees that the contractor will take care of needed infrastructure improvements, such as roads, utilities, and drainage, within the given timeline. 7. License and Permit Bond: This bond is necessary to obtain or renew a contractor's license in Louisiana. It ensures that the contractor will comply with all applicable laws, regulations, and building codes. These Louisiana contractor or construction bonds provide additional security to the project owner, ensuring that they have recourse if the contractor fails to meet their obligations. Obtaining the appropriate bond is an essential step for contractors in Louisiana to gain credibility, increase their chances of winning bids, and protect their reputation in the industry.