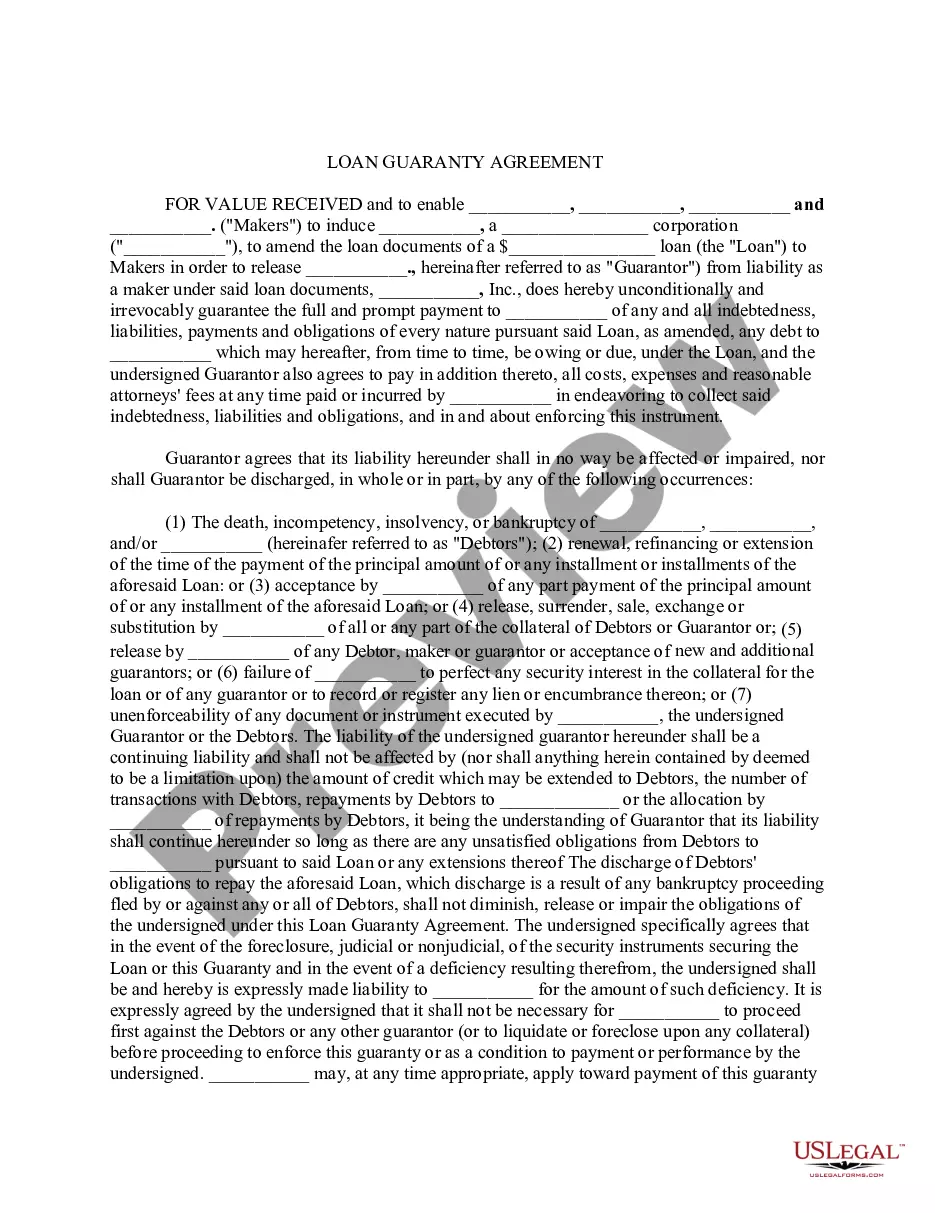

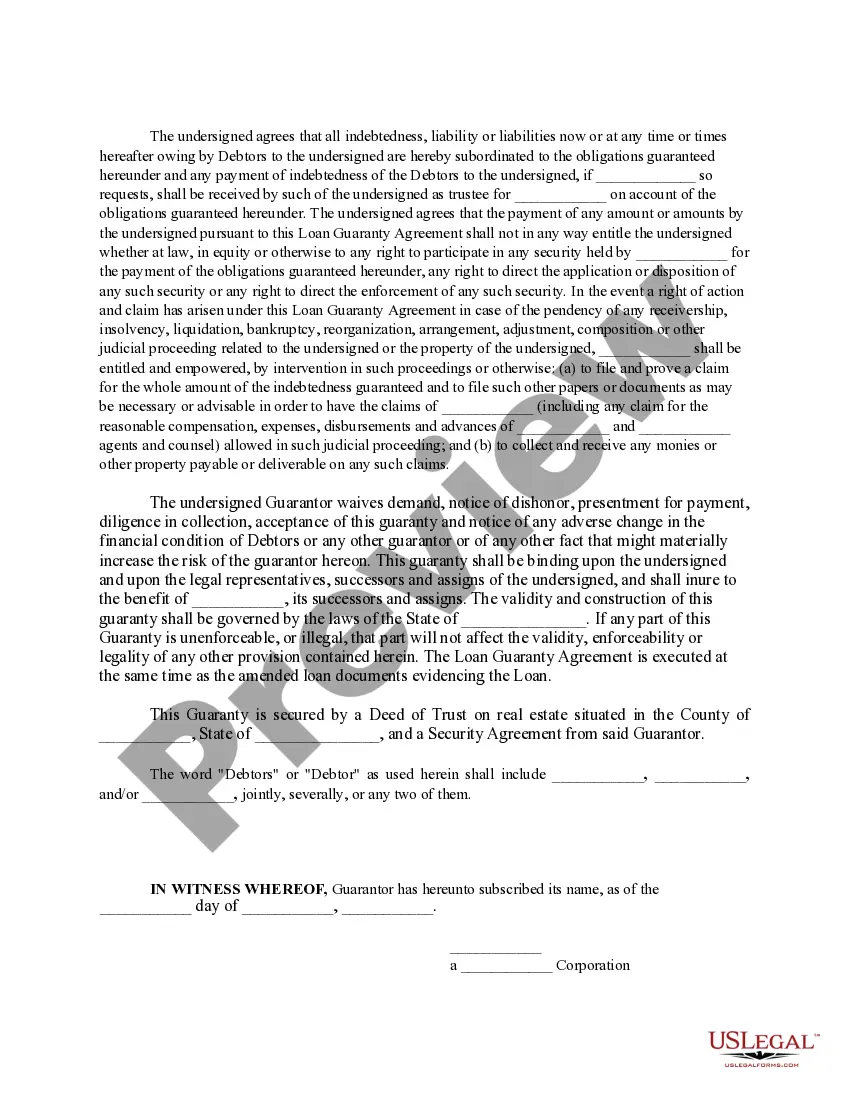

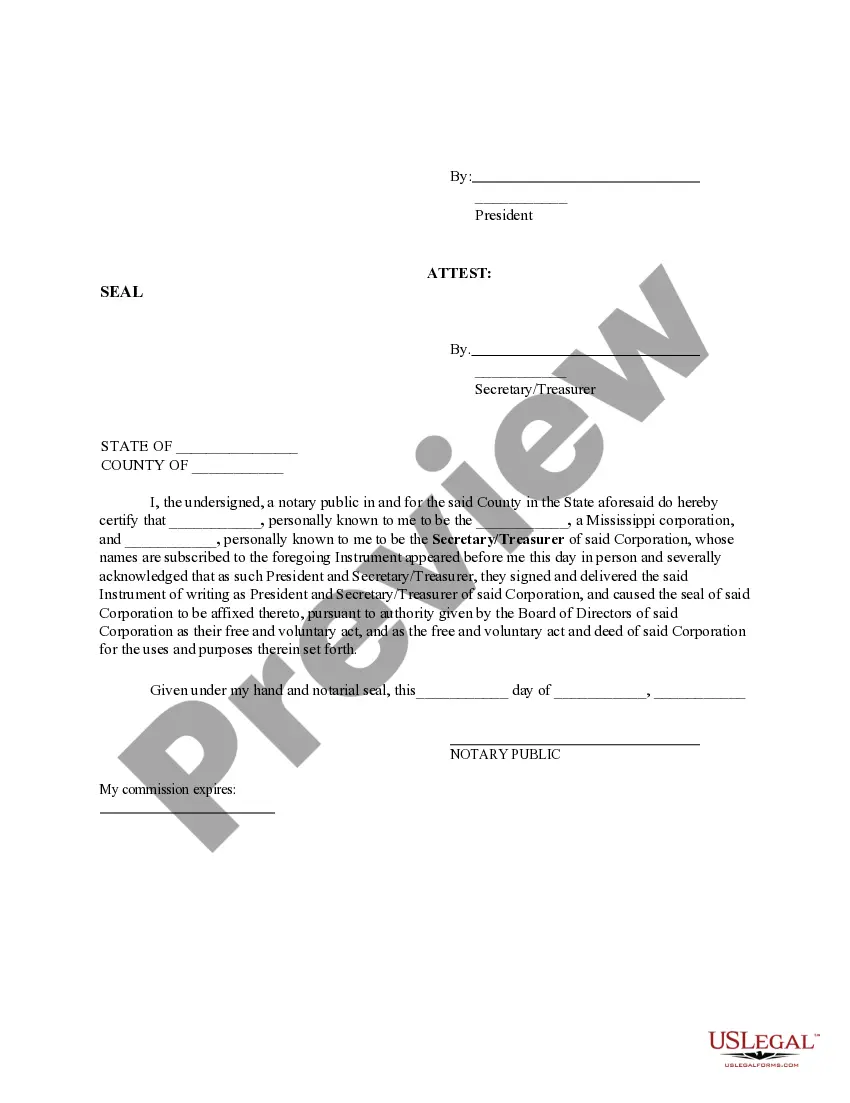

The Louisiana Loan Guaranty Agreement is a legal document that serves as a financial tool to provide reassurance and support for lenders in the lending industry. It offers protection to lenders by allowing them to request a loan guarantor who will assume responsibility if the borrower defaults on their loan obligations. This agreement is particularly useful for lenders who may have doubts about the borrower's ability to repay, providing them with necessary security to approve the loan application. The Louisiana Loan Guaranty Agreement involves three parties: the lender, the borrower, and the loan guarantor. The lender provides the loan amount to the borrower, who is the primary recipient of the loan. The loan guarantor, on the other hand, acts as a backup, promising to repay the loan if the borrower fails to fulfill their obligations. Different types of Louisiana Loan Guaranty Agreements include: 1. Personal Loan Guaranty Agreement: This type of agreement involves a loan guarantor who is usually a family member, friend, or acquaintance of the borrower. They guarantee the repayment of the loan, using their personal assets as collateral. 2. Small Business Loan Guaranty Agreement: These agreements are specifically designed to support small businesses. The guarantor, often a business partner or owner, pledges to repay the loan in case the business defaults. It helps small businesses gain access to financing that they might not otherwise qualify for. 3. Commercial Loan Guaranty Agreement: This type of agreement is typically used in commercial real estate transactions or large business loans. The guarantor, usually a business entity or a financially strong individual, assumes the responsibility of repaying the loan should the borrower default. 4. Construction Loan Guaranty Agreement: This agreement is commonly used in the construction industry, where the guarantor ensures that the funds will be available to complete a construction project. If the borrower fails to meet their obligations, the guarantor steps in to repay the loan and safeguard the interests of involved parties. In Louisiana, Loan Guaranty Agreements are governed by state laws and regulations, ensuring compliance and protection for all parties involved. It is crucial for lenders, borrowers, and guarantors to thoroughly understand the terms and conditions of the agreement before entering into it, ensuring a clear understanding of the rights and responsibilities of each party.

Louisiana Loan Guaranty Agreement

Description

How to fill out Louisiana Loan Guaranty Agreement?

Are you currently in the situation the place you need to have documents for either organization or specific uses almost every time? There are a variety of legal file web templates available online, but getting versions you can trust is not effortless. US Legal Forms delivers 1000s of develop web templates, just like the Louisiana Loan Guaranty Agreement, which can be published to satisfy federal and state specifications.

Should you be currently knowledgeable about US Legal Forms site and have an account, simply log in. Afterward, you can acquire the Louisiana Loan Guaranty Agreement format.

Unless you offer an profile and wish to begin using US Legal Forms, adopt these measures:

- Get the develop you need and ensure it is for the proper town/county.

- Make use of the Review switch to check the form.

- Read the explanation to ensure that you have selected the right develop.

- When the develop is not what you are looking for, make use of the Research discipline to get the develop that suits you and specifications.

- Whenever you discover the proper develop, just click Get now.

- Pick the pricing program you desire, complete the required details to create your bank account, and buy the transaction using your PayPal or charge card.

- Select a convenient paper file format and acquire your backup.

Locate all the file web templates you possess bought in the My Forms food selection. You can get a further backup of Louisiana Loan Guaranty Agreement whenever, if necessary. Just go through the required develop to acquire or print the file format.

Use US Legal Forms, by far the most extensive variety of legal types, in order to save time and stay away from mistakes. The support delivers professionally created legal file web templates that you can use for a range of uses. Produce an account on US Legal Forms and initiate creating your lifestyle easier.

Form popularity

FAQ

Redhibition in Louisiana The concept of redhibition dates back to the Louisiana Civil Code of 1870. While the law has changed over the years, Louisiana redhibition statutes offer a legal remedy for consumers who purchased a defective automobile, watercraft, or recreational vehicle.

The Louisiana New Home Warranty Act (LNHWA) provides the exclusive warranties, remedies, and peremptive periods as between builder and owner relative to home construction and no other provisions of law relative to warranties and redhibitory vices and defects shall apply.

The Louisiana Civil Code provides an implied warranty for all things sold. Specifically, a seller warrants the buyer against all redhibitory vices and defects.

The legislature finds a need to promote commerce in Louisiana by providing clear, concise, and mandatory warranties for the purchasers and occupants of new homes in Louisiana and by providing for the use of homeowners' insurance as additional protection for the public against defects in the construction of new homes.

What Is the Louisiana New Home Warranty Act? In the 1980s, the Louisiana legislature enacted a law to protect residents buying newly built homes. The law states that builders of newly constructed homes must ensure the homes are free of certain defects for up to five years.