Louisiana Private Annuity Agreement

Description

How to fill out Private Annuity Agreement?

It is feasible to spend numerous hours online searching for the legal document template that meets the requirements of state and federal laws that you seek.

US Legal Forms provides a vast selection of legal documents that have been evaluated by professionals.

It is easy to download or print the Louisiana Private Annuity Agreement from their service.

First, confirm that you have selected the correct document template for the county/city of your choice. Review the form outline to ensure you have chosen the proper form. If available, utilize the Review button to browse the document template as well.

- If you already possess a US Legal Forms account, you can sign in and click the Download button.

- Subsequently, you can complete, modify, print, or sign the Louisiana Private Annuity Agreement.

- Every legal document template you obtain is yours perpetually.

- To obtain an additional copy of any purchased document, navigate to the My documents tab and click the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the straightforward instructions below.

Form popularity

FAQ

The monthly payout from a $100,000 annuity can vary significantly based on several factors such as age, the type of annuity, and interest rates. A common estimate for a fixed annuity might yield anywhere from $400 to $600 per month. Utilizing a Louisiana Private Annuity Agreement tailored to your needs could help clarify these figures and set realistic expectations.

How to Report Annuity Income from Your 1099R on Your 1040 Tax Return. If you drew any income from annuities during the tax year under consideration, it goes on line 16 of Form 1040. The Forms 1099-R described above (without a check in the IRA box) reports distributions from pensions and annuities.

The annual annuity payment is calculated thus:Annual Annuity Payment = FMV of Property Transferred ÷ Present Value of Annuity Factor.Expected Return of Annuity = Annual Payment A Life Expectancy.Exclusion Ratio = Sellers Cost Basis A· Expected Return.More items...a¢

Each annuity payment is treated as part tax-free return of basis, part capital gain, and part ordinary income until your entire basis is recovered. Once your basis is recovered, the entire annuity is treated as part capital gain and part ordinary income until you have surpassed your life expectancy.

The private annuity arrangement does not, however, avoid taxation altogether. The annuitant is liable to pay capital gains taxes on the appreciated value of the asset sold, but on a deferred basis.

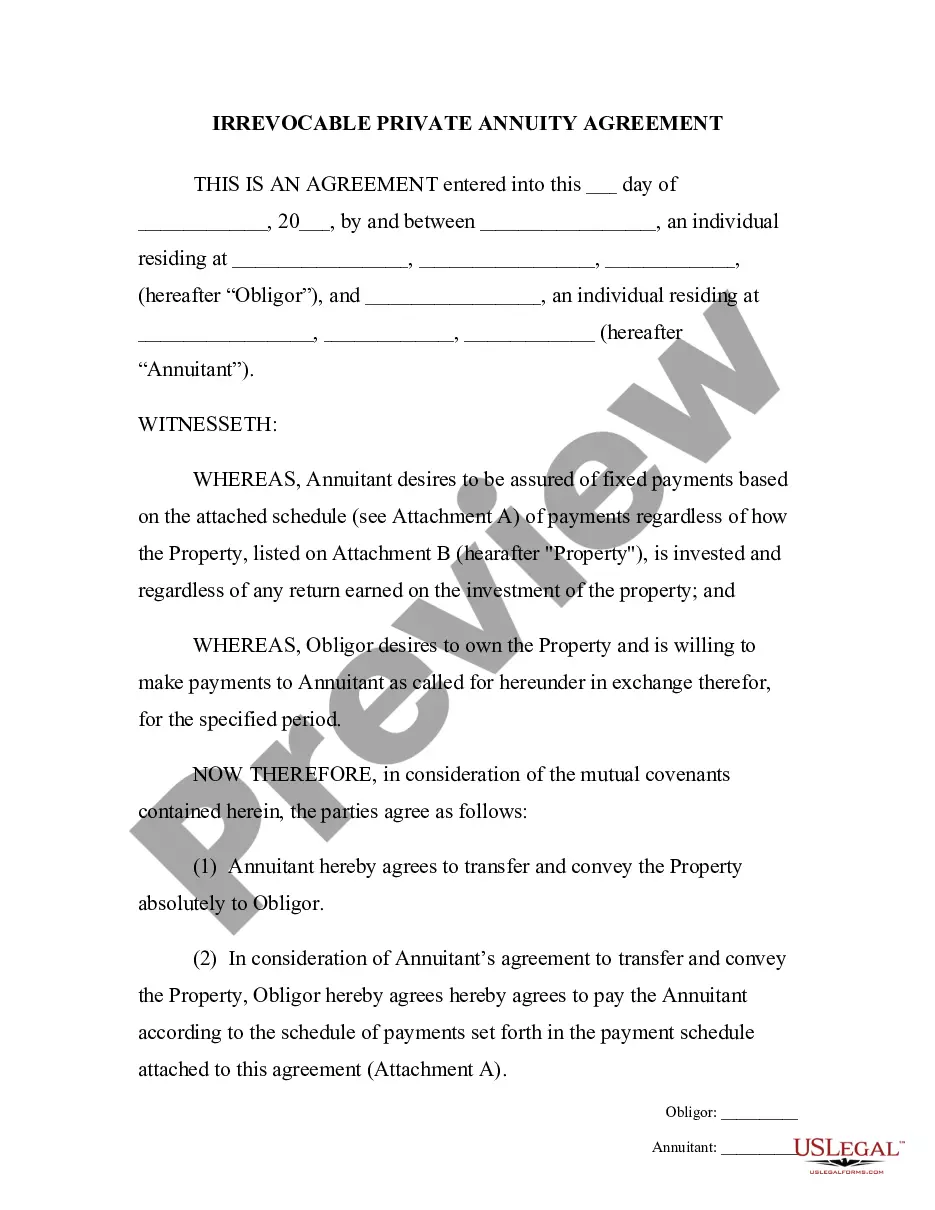

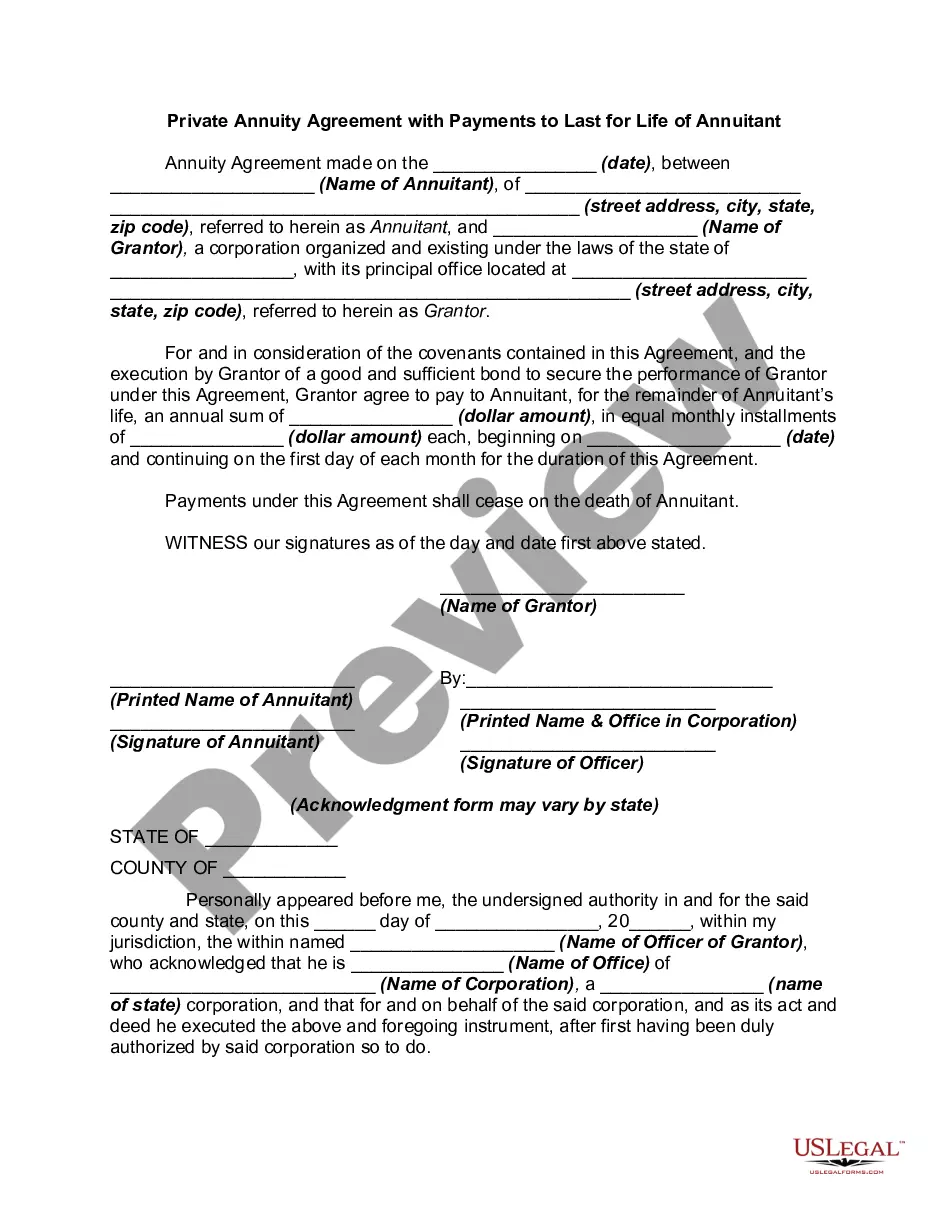

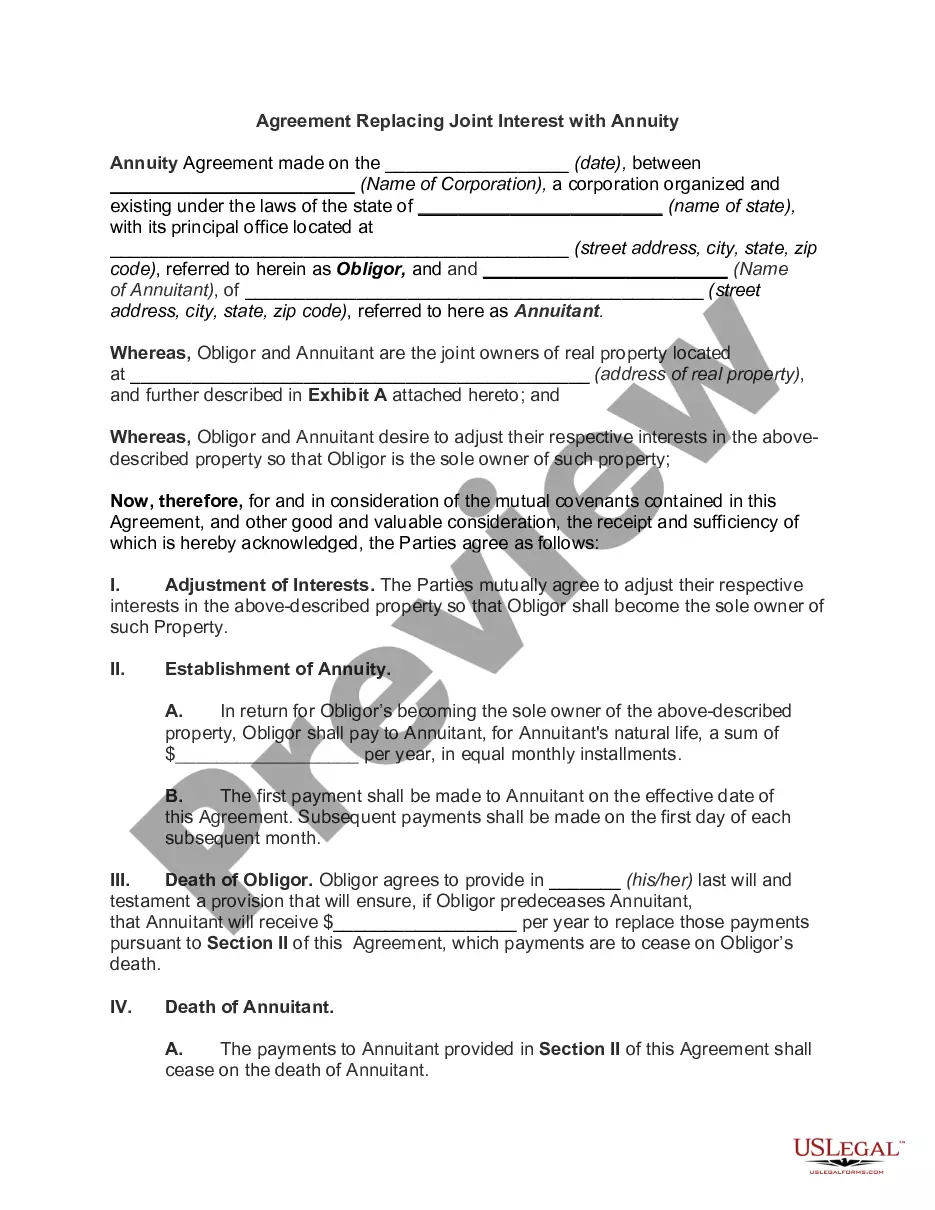

A private annuity is a special agreement in which an individual (annuitant) transfers property to an obligor. The obligor agrees to make payments to the annuitant according to an agreed-upon schedule in exchange for the property transfer.

First, a bit of good news: All annuities grow tax-deferred, meaning that you don't have to pay any taxes until you take a distribution either through a regular payment or a withdrawal from an accumulation annuity.

Withdrawals and lump-sum distributions from an annuity are taxed as ordinary income. They do not receive the benefit of being taxed as capital gains.

You do not owe income taxes on your annuity until you withdraw money or begin receiving payments. Upon a withdrawal, the money will be taxed as income if you purchased the annuity with pre-tax funds. If you purchased the annuity with post-tax funds, you would only pay tax on the earnings.

Distributions from your annuity are generally reportable on Form 1040, Form 1040-SR, or 1040-NR. You are required to attach Copy B of your 1099-R to your federal income tax return only if federal income tax is withheld and an amount is shown in Box 4.