Louisiana Form of Note

Description

How to fill out Form Of Note?

US Legal Forms - among the biggest libraries of authorized forms in the United States - offers a wide range of authorized document web templates you can down load or print. Making use of the internet site, you may get a large number of forms for organization and person functions, sorted by groups, states, or keywords and phrases.You can find the most up-to-date versions of forms just like the Louisiana Form of Note in seconds.

If you already have a registration, log in and down load Louisiana Form of Note through the US Legal Forms local library. The Down load option will show up on each kind you view. You get access to all in the past delivered electronically forms from the My Forms tab of the bank account.

If you want to use US Legal Forms the first time, listed here are straightforward instructions to help you started:

- Ensure you have picked out the best kind for your personal town/area. Select the Review option to analyze the form`s content material. Read the kind information to ensure that you have chosen the appropriate kind.

- When the kind does not fit your demands, make use of the Look for industry on top of the monitor to obtain the one which does.

- If you are happy with the shape, confirm your decision by simply clicking the Acquire now option. Then, choose the prices plan you like and supply your accreditations to sign up for an bank account.

- Approach the transaction. Use your Visa or Mastercard or PayPal bank account to perform the transaction.

- Pick the structure and down load the shape in your system.

- Make changes. Load, modify and print and indication the delivered electronically Louisiana Form of Note.

Every single format you added to your account does not have an expiration particular date and is your own eternally. So, if you want to down load or print one more version, just visit the My Forms portion and click in the kind you will need.

Get access to the Louisiana Form of Note with US Legal Forms, one of the most substantial local library of authorized document web templates. Use a large number of expert and express-certain web templates that fulfill your business or person requirements and demands.

Form popularity

FAQ

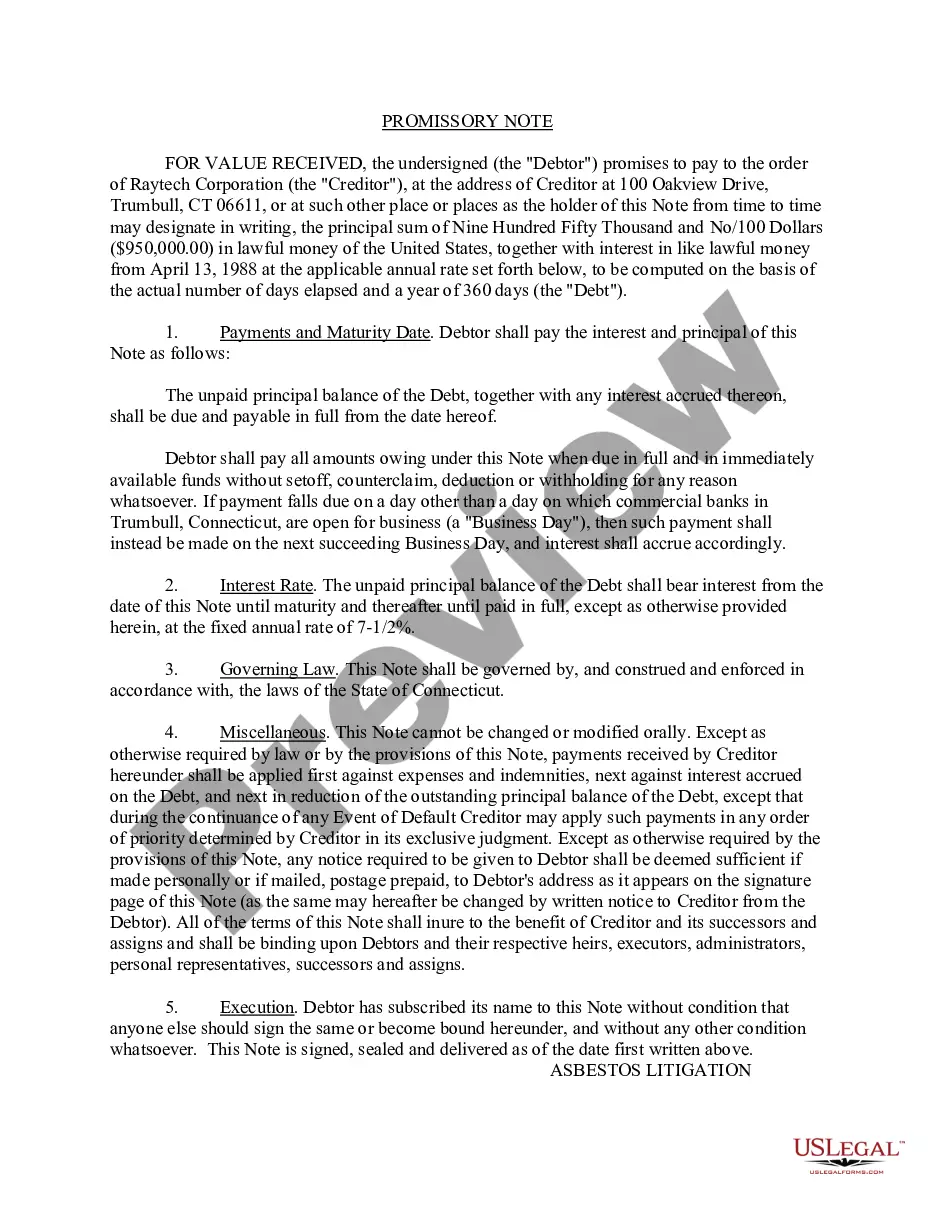

A promissory note is a form of debt that companies and individuals sometimes use, like loans, to raise money. The issuer, through the notes, promises to return the buyer's funds (principal) and to make fixed interest payments to the buyer in exchange for borrowing the money.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

A promissory note need only be signed and does not require an acknowledgement before a notary public to be valid.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

A promissory note typically contains all the terms pertaining to the indebtedness, such as the principal amount, interest rate, maturity date, date and place of issuance, and issuer's signature.

Promissory notes are quite simple and can be prepared by anyone. They do not need to be prepared by a lawyer or be notarized. It isn't even particularly significant whether a promissory note is handwritten or typed and printed.

First, you'll need the names and addresses of both the lender (or "payee") and the borrower. You should then list the basic promissory note terms and conditions: The amount of money being lent. The interest rate, if you are charging interest.

The note must also contain the terms and conditions between the two parties involved. This includes the amount of money or capital loaned, the interest rate and the repayment schedule. Once the parties address the conditions of the promissory note and sign it, it becomes a legally binding contract.