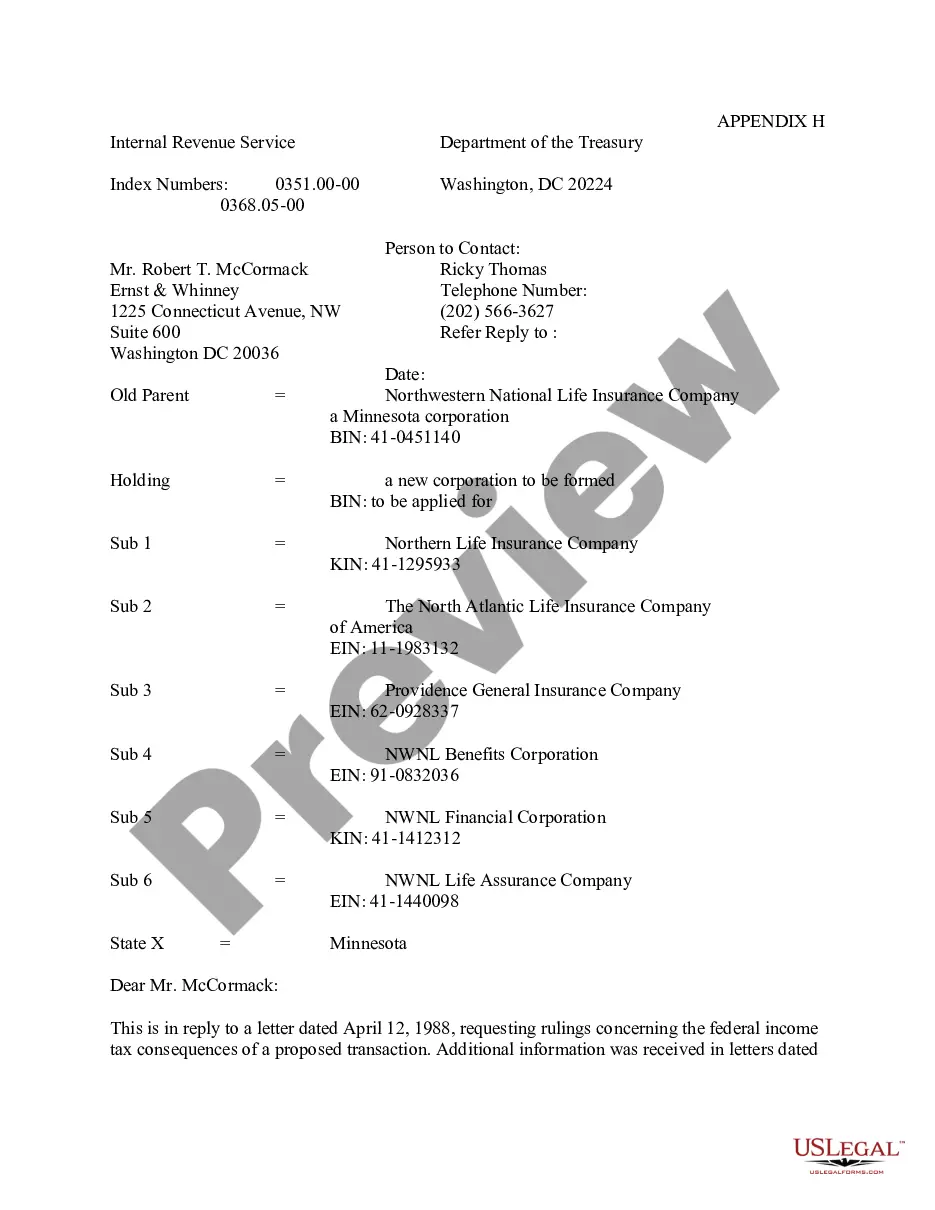

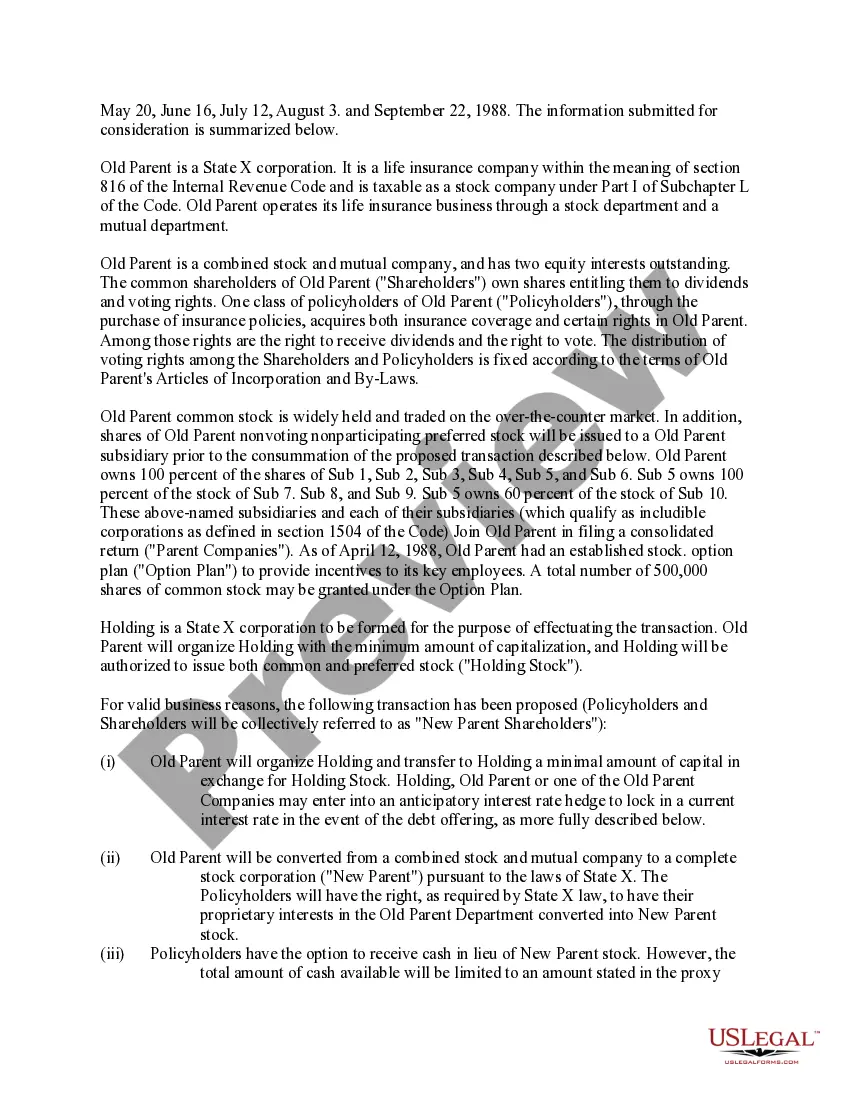

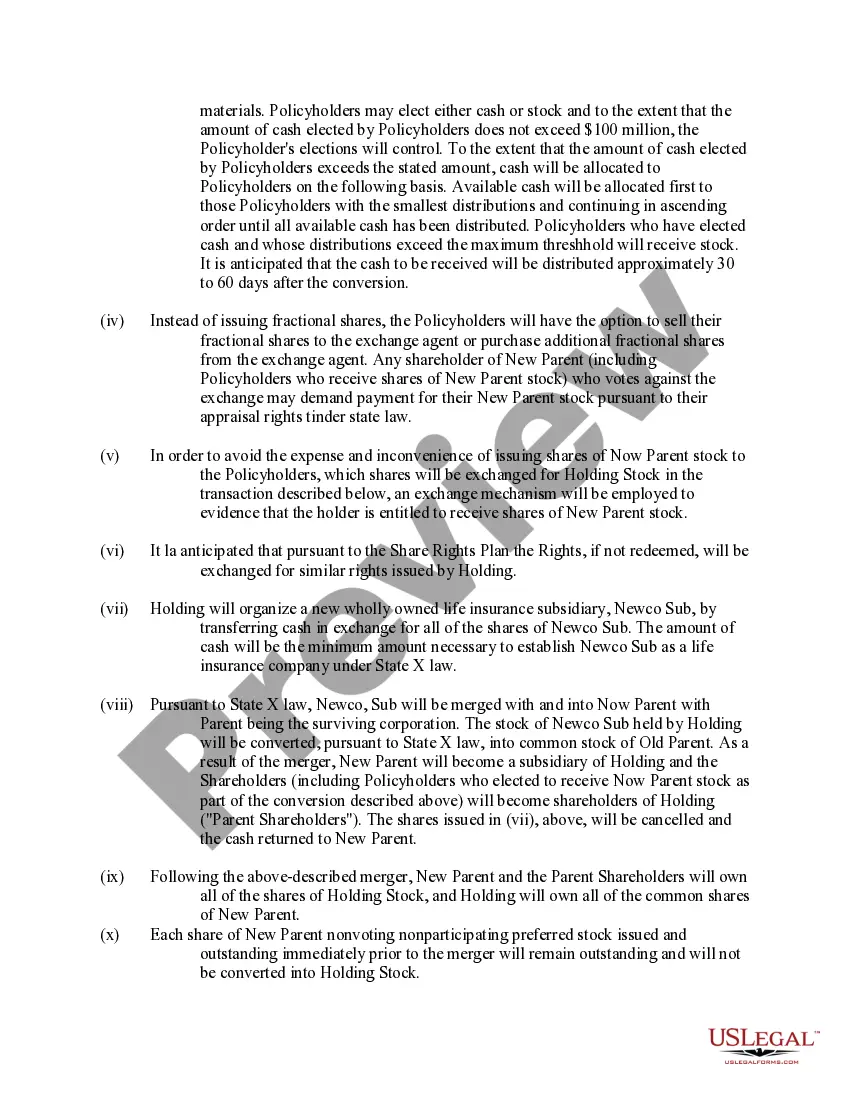

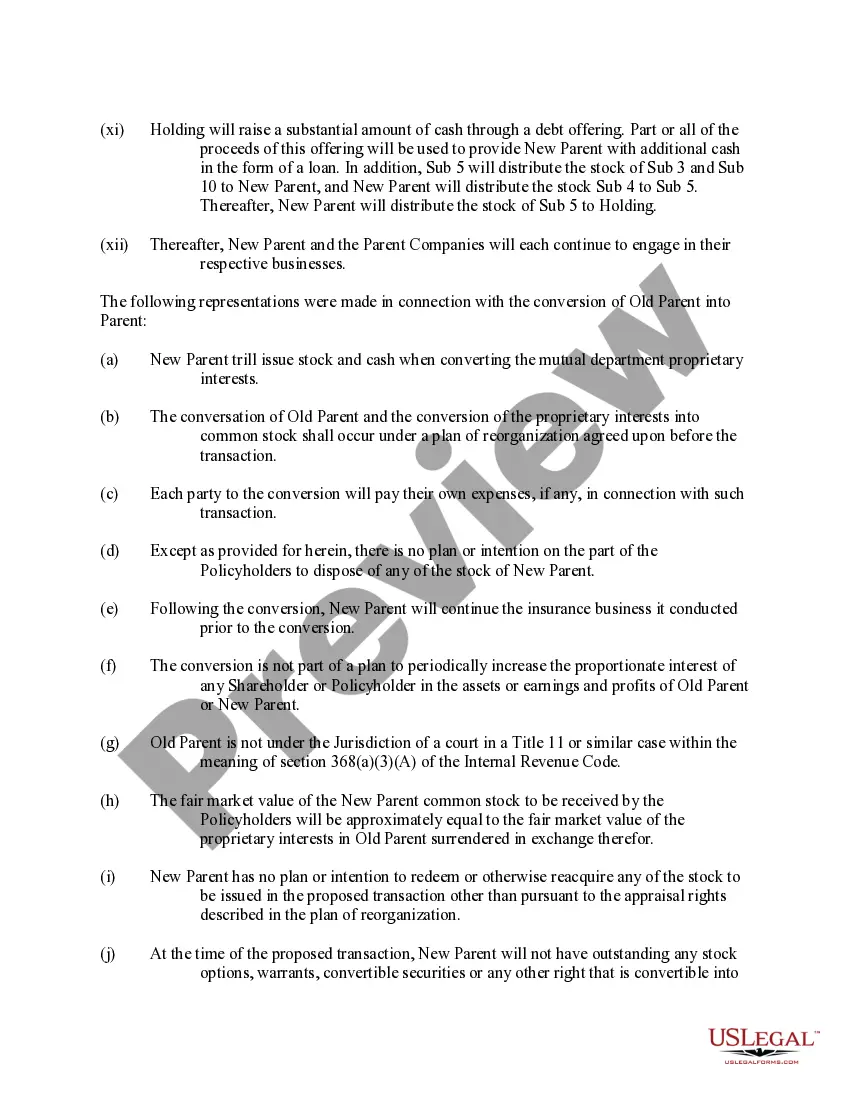

The Louisiana Internal Revenue Service (IRS) Ruling Letter is an official document issued by the Louisiana Department of Revenue (DR), which provides taxpayers with a written statement interpreting and applying the tax laws of the state. This ruling letter helps individuals, businesses, and tax professionals understand their rights and obligations regarding state taxes in Louisiana. The Louisiana IRS Ruling Letter serves as a binding statement of the DR's position on specific tax issues. It provides guidance and clarity on various tax matters, including income tax, sales tax, use tax, excise tax, and other state-imposed taxes. The letter explains how the DR interprets and applies the law to specific facts and circumstances, offering taxpayers a clearer understanding of how to comply with state tax requirements. The ruling letter is invaluable for taxpayers who require assurance regarding the tax treatment of specific transactions, issues, or industries. It eliminates ambiguity and provides a level of certainty for taxpayers, reducing the potential for misunderstandings or disputes with the DR. Different types of Louisiana IRS Ruling Letters exist to address various tax situations and scenarios. Some common types may include: 1. Income Tax Ruling Letters: These letters cover matters related to the Louisiana income tax code, such as tax deductions, credits, exemptions, and calculations. 2. Sales and Use Tax Ruling Letters: These letters pertain to the application and interpretation of Louisiana's sales and use tax laws for businesses engaged in selling tangible goods or providing taxable services. 3. Excise Tax Ruling Letters: These letters focus on excise taxes, which are imposed on specific goods like alcohol, tobacco, fuel, or gaming activities, outlining how these taxes should be applied and assessed. 4. Industry-Specific Ruling Letters: These letters address tax issues specific to particular industries, such as healthcare, transportation, construction, or manufacturing, providing industry-specific guidance for compliance. 5. General Ruling Letters: These letters cover general tax issues that don't fall under specific categories or address cross-cutting issues applicable to different types of taxes. It is essential for taxpayers to consult the appropriate ruling letter relevant to their tax situation, as interpretations and guidance may vary depending on the type of tax involved. The Louisiana IRS Ruling Letter provides a valuable resource that promotes compliance, uniformity, and consistency in tax administration across the state.

Louisiana Internal Revenue Service Ruling Letter

Description

How to fill out Louisiana Internal Revenue Service Ruling Letter?

If you have to complete, download, or printing legitimate record templates, use US Legal Forms, the most important variety of legitimate kinds, that can be found on the Internet. Utilize the site`s easy and handy research to obtain the documents you need. Numerous templates for organization and individual reasons are sorted by classes and states, or search phrases. Use US Legal Forms to obtain the Louisiana Internal Revenue Service Ruling Letter with a number of clicks.

Should you be presently a US Legal Forms buyer, log in in your bank account and then click the Download switch to obtain the Louisiana Internal Revenue Service Ruling Letter. You can even entry kinds you in the past saved inside the My Forms tab of the bank account.

Should you use US Legal Forms initially, refer to the instructions beneath:

- Step 1. Ensure you have chosen the form for that appropriate town/region.

- Step 2. Use the Review method to check out the form`s content. Do not overlook to see the description.

- Step 3. Should you be not satisfied using the develop, utilize the Search discipline towards the top of the display screen to locate other versions of your legitimate develop design.

- Step 4. After you have identified the form you need, click the Acquire now switch. Choose the rates program you like and add your qualifications to register to have an bank account.

- Step 5. Procedure the purchase. You should use your bank card or PayPal bank account to complete the purchase.

- Step 6. Select the format of your legitimate develop and download it on your own device.

- Step 7. Full, edit and printing or signal the Louisiana Internal Revenue Service Ruling Letter.

Every single legitimate record design you acquire is your own property for a long time. You might have acces to every single develop you saved with your acccount. Go through the My Forms segment and decide on a develop to printing or download once again.

Be competitive and download, and printing the Louisiana Internal Revenue Service Ruling Letter with US Legal Forms. There are thousands of professional and express-specific kinds you can utilize to your organization or individual needs.