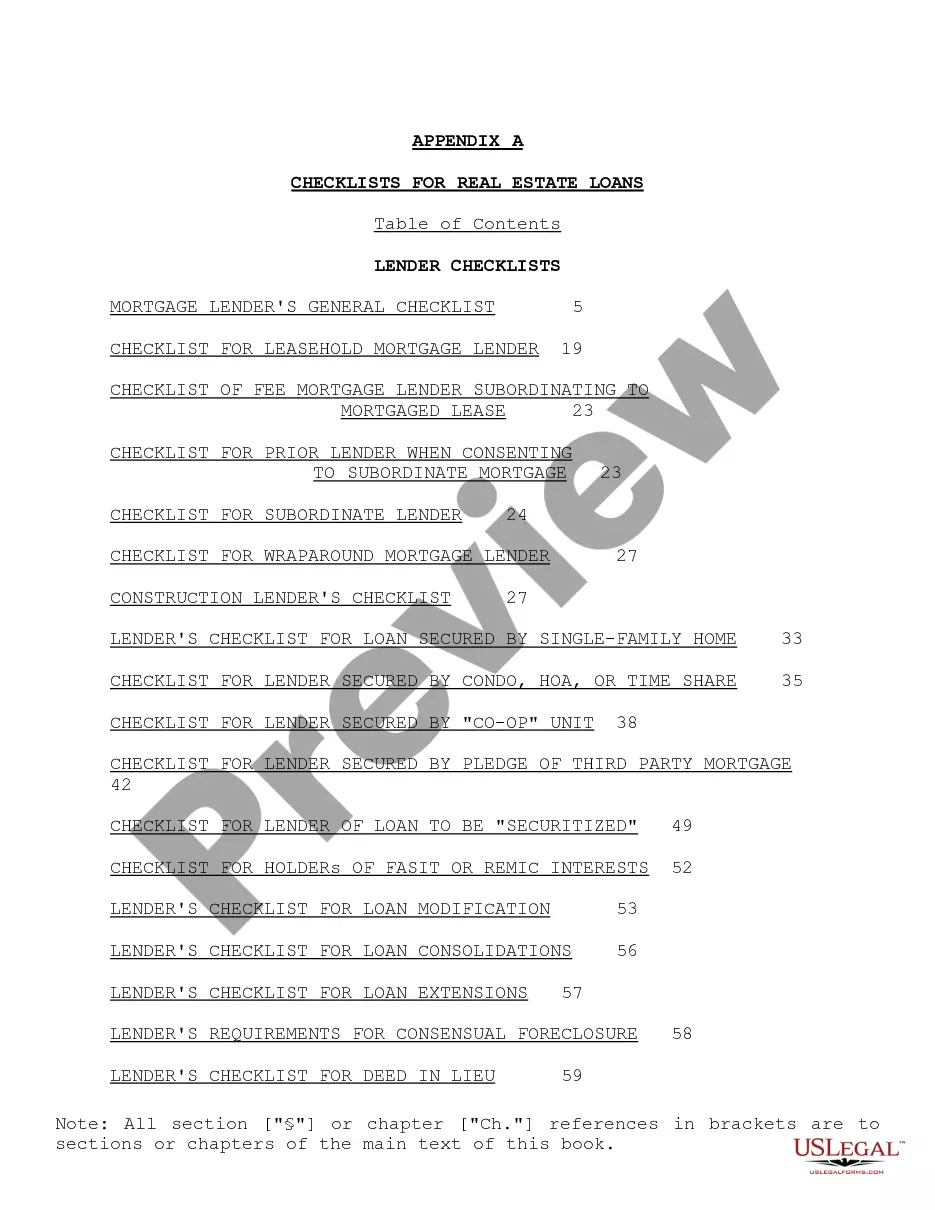

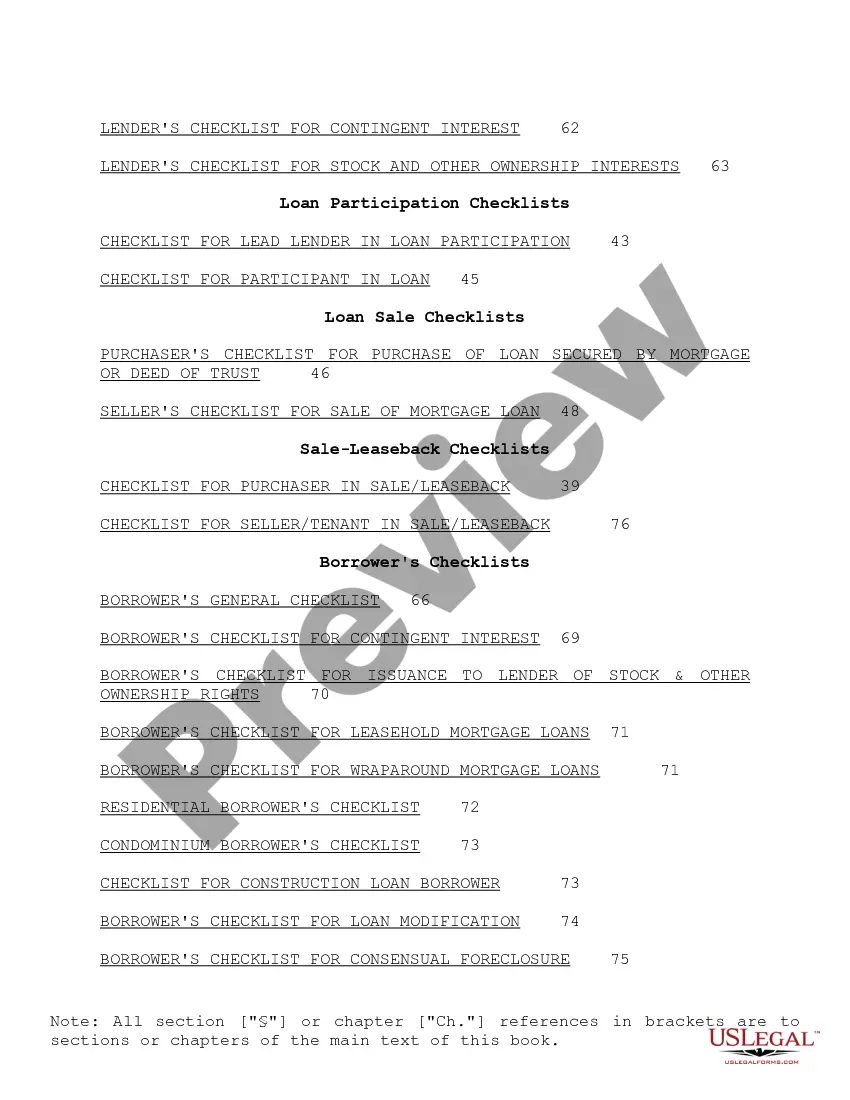

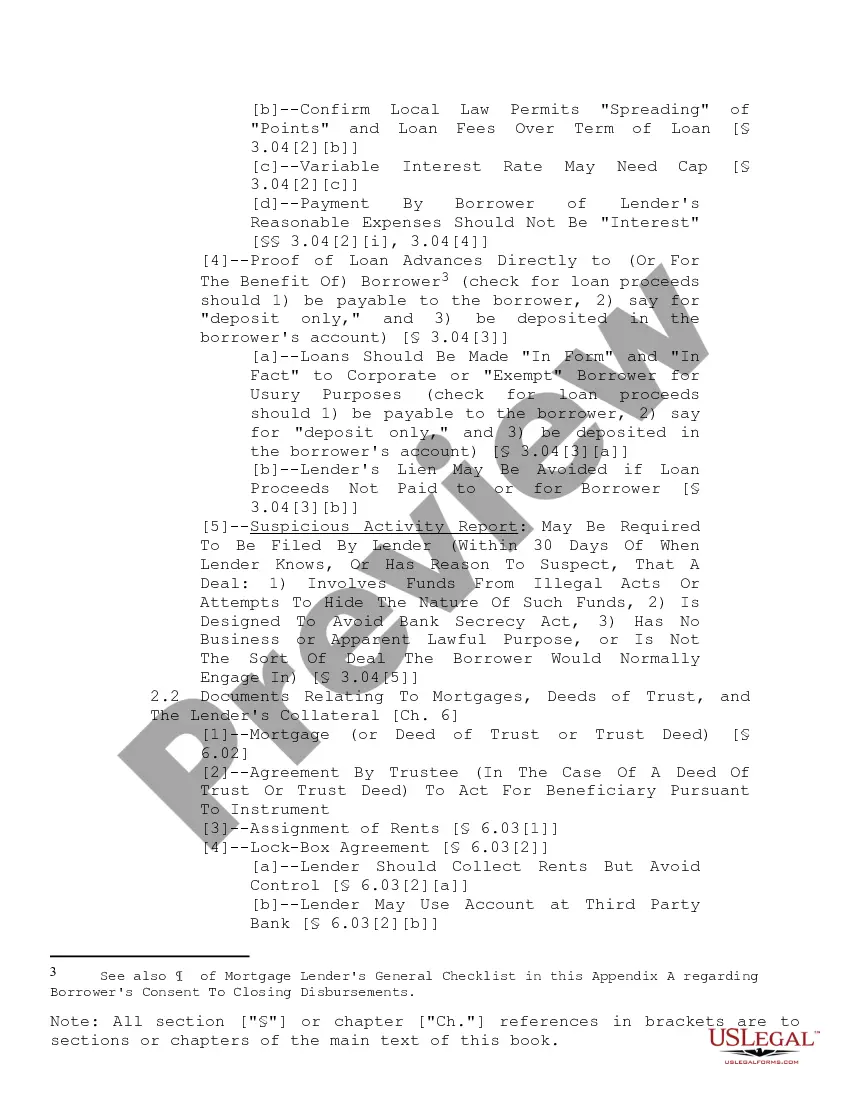

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Louisiana Checklist for Real Estate Loans: A Comprehensive Guide When it comes to real estate loans in Louisiana, it is crucial for both lenders and borrowers to go through an extensive checklist to ensure a smooth and successful lending process. This detailed description will provide an overview of the essential elements that constitute a Louisiana Checklist for Real Estate Loans, encompassing various types of loans. 1. Residential Real Estate Loan Checklist: This checklist caters to individuals seeking loans for residential properties, such as single-family homes, town homes, or condominiums. It includes the following key elements: — Verification of income and employment: lenders assess the borrower's ability to repay the loan by analyzing income and employment history. — Credit check: the borrower's creditworthiness is evaluated by reviewing credit reports and scores. — Down payment: lenders confirm the availability of the required down payment for the loan. — Property appraisal: to determine the property's value and ensure it meets the lender's requirements. — Title search and insurance: to uncover any liens, verify ownership, and secure the lender's investment through title insurance. — Homeowner's insurance: proof of insurance coverage to protect the property and lender against potential damages. — Flood zone determination: vital for properties located in flood-prone areas to assess the level of risk. 2. Commercial Real Estate Loan Checklist: This checklist focuses on loans for commercial properties such as offices, retail spaces, warehouses, or industrial complexes. It encompasses crucial factors like: — Business financial statements: lenders review cash flow, balance sheets, and income statements to assess the business's financial health. — Business plan: the borrower must provide a comprehensive plan outlining the objectives, projections, and strategy related to the commercial property. — Debt service coverage ratioDSCCR): lenders analyze the ratio between the property's net operating income and the debt payments to ensure the borrower's ability to repay the loan. — Environmental assessment: required to evaluate potential environmental risks associated with the property, such as contamination or hazardous materials. — Zoning compliance: confirmation that the property complies with local zoning regulations, permitted usage, and building codes. 3. Construction Loan Checklist: This specific checklist caters to borrowers seeking funds for construction projects. It includes: — Detailed construction plans: architectural and engineering plans that outline the project's scope, specifications, and materials. — Construction budget and contractor information: lenders require a comprehensive budget breakdown, along with contractor details. — Building permits and inspections: verification that all necessary permits are obtained, and construction adheres to local regulations. — Disbursement schedule: a detailed plan showing when and how the loan funds will be released throughout the construction process. Remember that each lender may have specific variations to these checklists or additional requirements. It is crucial for borrowers to consult their chosen lender to ensure they have a comprehensive understanding of the specific checklist and gather all necessary documentation. In conclusion, a Louisiana Checklist for Real Estate Loans consists of various types, such as residential, commercial, and construction loans. Each type includes unique elements to evaluate the borrower's eligibility, property value, compliance with regulations, and associated risks. Adhering to these checklists ensures a transparent and efficient lending process for both parties involved.Louisiana Checklist for Real Estate Loans: A Comprehensive Guide When it comes to real estate loans in Louisiana, it is crucial for both lenders and borrowers to go through an extensive checklist to ensure a smooth and successful lending process. This detailed description will provide an overview of the essential elements that constitute a Louisiana Checklist for Real Estate Loans, encompassing various types of loans. 1. Residential Real Estate Loan Checklist: This checklist caters to individuals seeking loans for residential properties, such as single-family homes, town homes, or condominiums. It includes the following key elements: — Verification of income and employment: lenders assess the borrower's ability to repay the loan by analyzing income and employment history. — Credit check: the borrower's creditworthiness is evaluated by reviewing credit reports and scores. — Down payment: lenders confirm the availability of the required down payment for the loan. — Property appraisal: to determine the property's value and ensure it meets the lender's requirements. — Title search and insurance: to uncover any liens, verify ownership, and secure the lender's investment through title insurance. — Homeowner's insurance: proof of insurance coverage to protect the property and lender against potential damages. — Flood zone determination: vital for properties located in flood-prone areas to assess the level of risk. 2. Commercial Real Estate Loan Checklist: This checklist focuses on loans for commercial properties such as offices, retail spaces, warehouses, or industrial complexes. It encompasses crucial factors like: — Business financial statements: lenders review cash flow, balance sheets, and income statements to assess the business's financial health. — Business plan: the borrower must provide a comprehensive plan outlining the objectives, projections, and strategy related to the commercial property. — Debt service coverage ratioDSCCR): lenders analyze the ratio between the property's net operating income and the debt payments to ensure the borrower's ability to repay the loan. — Environmental assessment: required to evaluate potential environmental risks associated with the property, such as contamination or hazardous materials. — Zoning compliance: confirmation that the property complies with local zoning regulations, permitted usage, and building codes. 3. Construction Loan Checklist: This specific checklist caters to borrowers seeking funds for construction projects. It includes: — Detailed construction plans: architectural and engineering plans that outline the project's scope, specifications, and materials. — Construction budget and contractor information: lenders require a comprehensive budget breakdown, along with contractor details. — Building permits and inspections: verification that all necessary permits are obtained, and construction adheres to local regulations. — Disbursement schedule: a detailed plan showing when and how the loan funds will be released throughout the construction process. Remember that each lender may have specific variations to these checklists or additional requirements. It is crucial for borrowers to consult their chosen lender to ensure they have a comprehensive understanding of the specific checklist and gather all necessary documentation. In conclusion, a Louisiana Checklist for Real Estate Loans consists of various types, such as residential, commercial, and construction loans. Each type includes unique elements to evaluate the borrower's eligibility, property value, compliance with regulations, and associated risks. Adhering to these checklists ensures a transparent and efficient lending process for both parties involved.