Louisiana Checklist - Joint Venture Agreement

Description

How to fill out Checklist - Joint Venture Agreement?

You may spend several hours on the web attempting to find the lawful file format which fits the state and federal demands you want. US Legal Forms supplies thousands of lawful varieties that are examined by pros. You can actually obtain or printing the Louisiana Checklist - Joint Venture Agreement from your service.

If you already possess a US Legal Forms account, you are able to log in and click the Down load key. After that, you are able to full, change, printing, or indication the Louisiana Checklist - Joint Venture Agreement. Each and every lawful file format you buy is your own property eternally. To obtain one more version of any purchased form, go to the My Forms tab and click the related key.

If you use the US Legal Forms internet site the very first time, stick to the simple recommendations under:

- Initial, ensure that you have chosen the correct file format for your county/town of your choice. Read the form explanation to ensure you have selected the right form. If offered, utilize the Review key to appear with the file format also.

- If you want to find one more version of your form, utilize the Look for field to find the format that suits you and demands.

- After you have discovered the format you would like, just click Get now to continue.

- Pick the prices prepare you would like, key in your credentials, and sign up for a merchant account on US Legal Forms.

- Full the deal. You should use your bank card or PayPal account to cover the lawful form.

- Pick the file format of your file and obtain it in your product.

- Make changes in your file if required. You may full, change and indication and printing Louisiana Checklist - Joint Venture Agreement.

Down load and printing thousands of file themes while using US Legal Forms website, which provides the most important assortment of lawful varieties. Use professional and state-distinct themes to take on your organization or individual requires.

Form popularity

FAQ

There are a variety of ways to structure a joint venture: Collaboration agreement or contractual joint venture. ... Joint venture by way of legal entity. ... A limited company. ... What are the benefits of choosing a limited company? ... A limited liability partnership. ... A legal partnership.

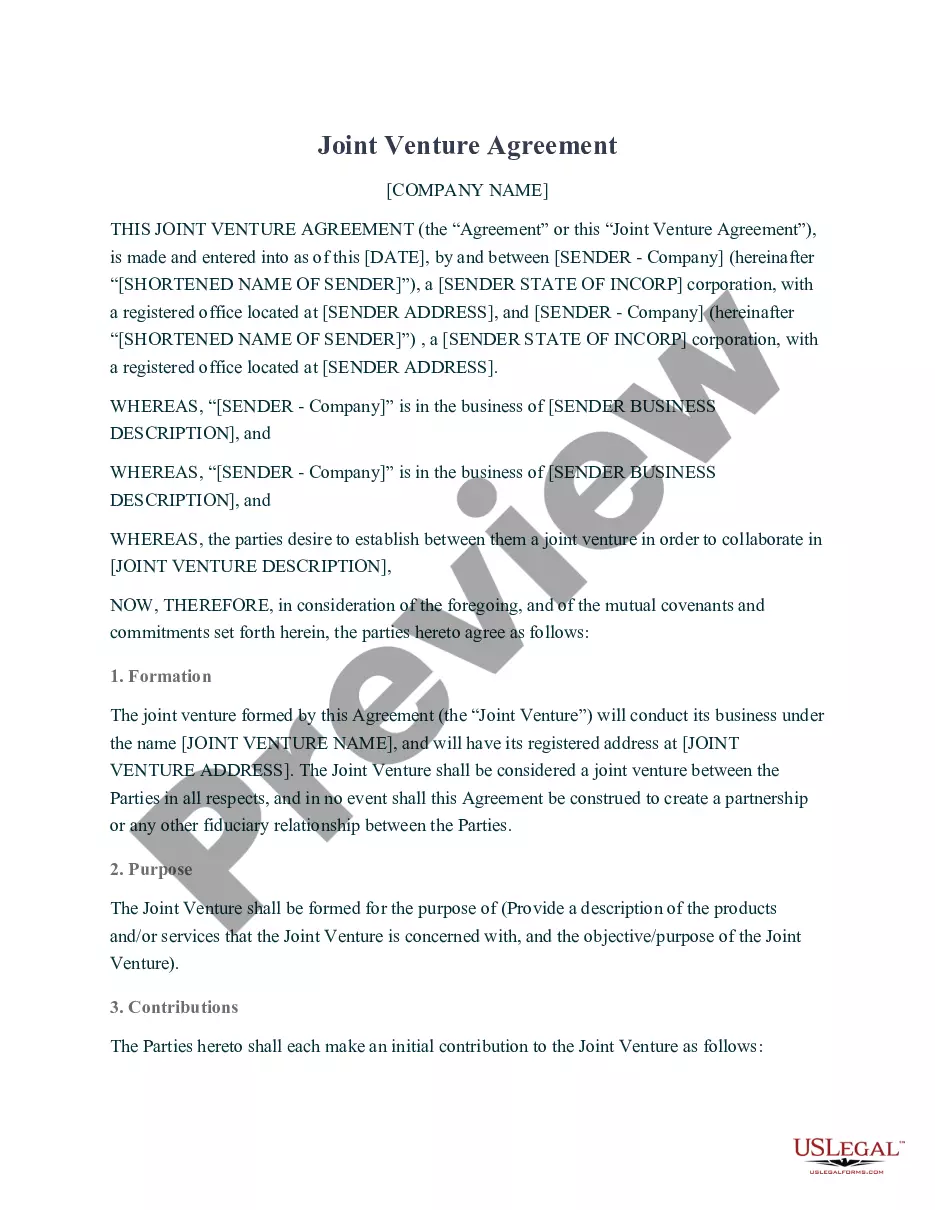

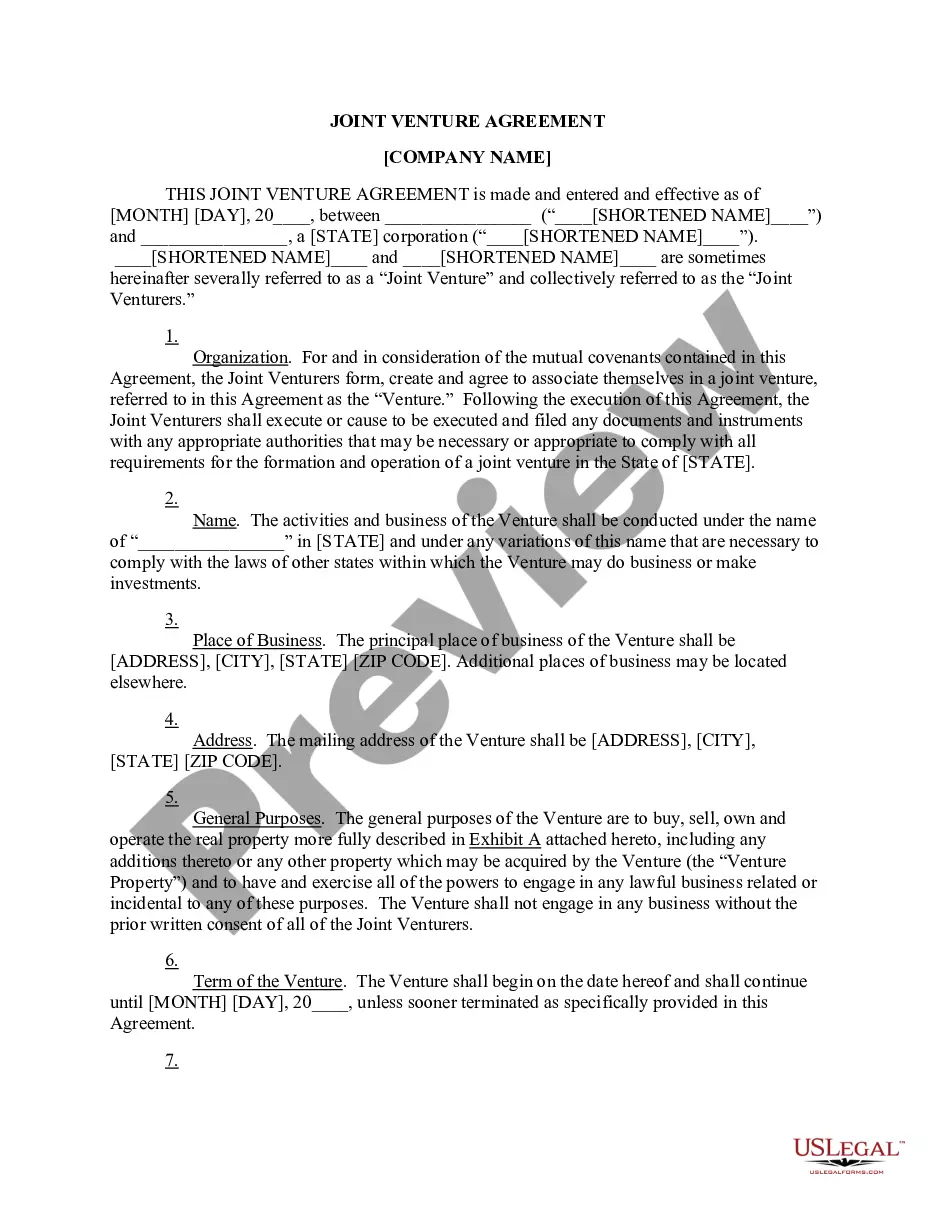

A written joint venture agreement should clearly lay out factors such as each party's stake of the business, roles, responsibilities, the management and decision-making processes, future rewards and the exit strategy.

What will each party do, and how will they do it? How will any property (including intellectual property created by the JV) be owned and dealt with? Who will be part of the management team for the JV and what will their obligations include? Also consider the scope of the business and territory of the JV.

Key Elements of a Joint Venture Agreement Business address. ... Joint venture types. ... Purpose of the agreement. ... Names and addresses of members. ... Duties and obligations. ... Voting and formal meeting requirements. ... Assignment of percentage ownership. ... Profit or loss allocation.

The agreement should clearly state the parties' intent to form a joint venture and what its purpose is. For one reason, this sort of mission statement helps manage the expectations of all parties involved. But also, joint ventures typically end once the stated goal is accomplished.

drafted joint venture agreement should cover essential aspects such as the purpose and goals of the venture, financial contributions, profitsharing arrangements, roles and responsibilities of each party, governance structure, dispute resolution mechanisms, exit strategies, and the duration of the venture.

Define the business purpose and goals of the joint venture. Determine the structure of the joint venture. Develop a clear understanding of the roles and responsibilities of each party. Negotiate and sign a joint venture agreement. Establish a governance framework for the joint venture.

It can be established via one of four basic legal structures: (a) Limited Liability Company, (b)Limited Liability Partnership (LLP), (c) a Partnership (or limited partnership), or (d) a purely Contractual Co-operation Agreement. Broadly, the four forms reflect varying degrees of integration of the interests in the JV.

Essentially, a joint venture is, as a matter of Louisiana case law, a partnership under Louisiana law. The jurisprudence has established that the essential elements of a joint venture are generally the same as those of partnership, i.e., two or more parties combining their property, labor, skill, etc.

Structuring A Joint Venture Agreement: 8 Important Elements 8 Key Elements in a Joint Venture Agreement. ... The identity of the businesses involved. ... The purpose of the joint venture. ... Resources to be shared. ... Sharing of profits and losses. ... Rights and duties. ... Dispute resolution. ... Governance.