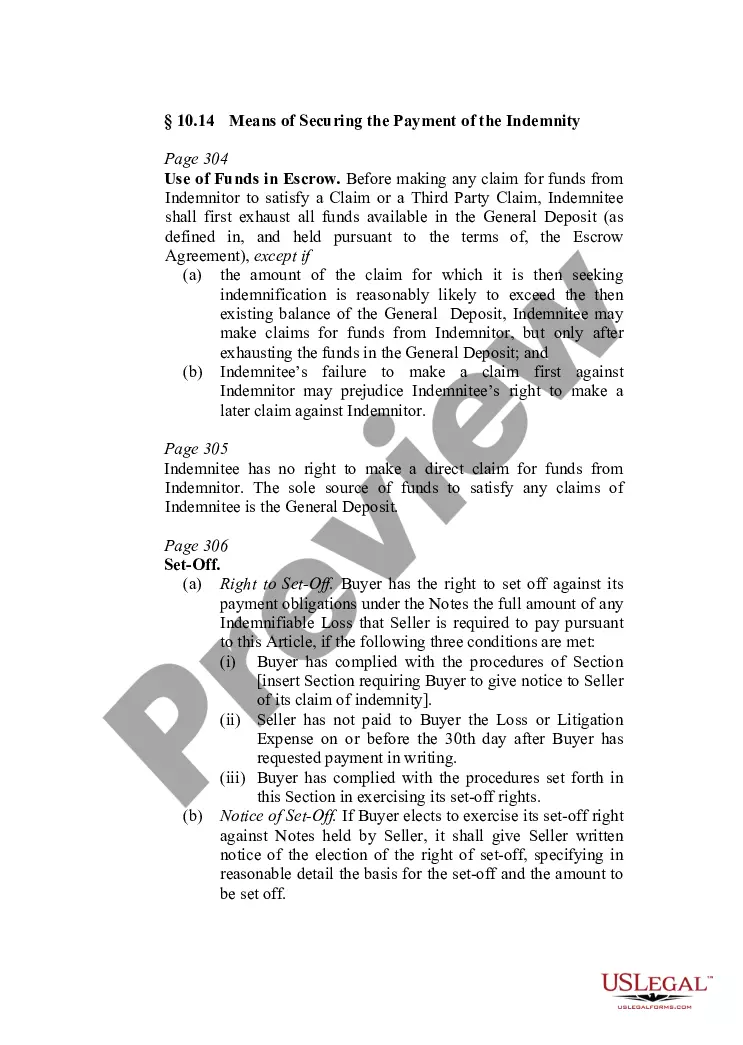

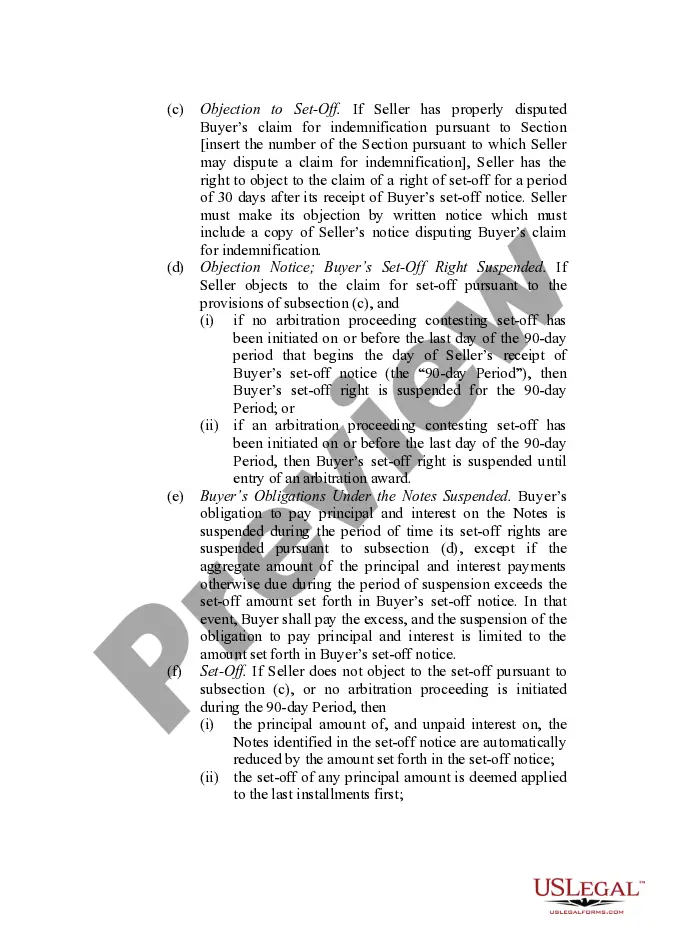

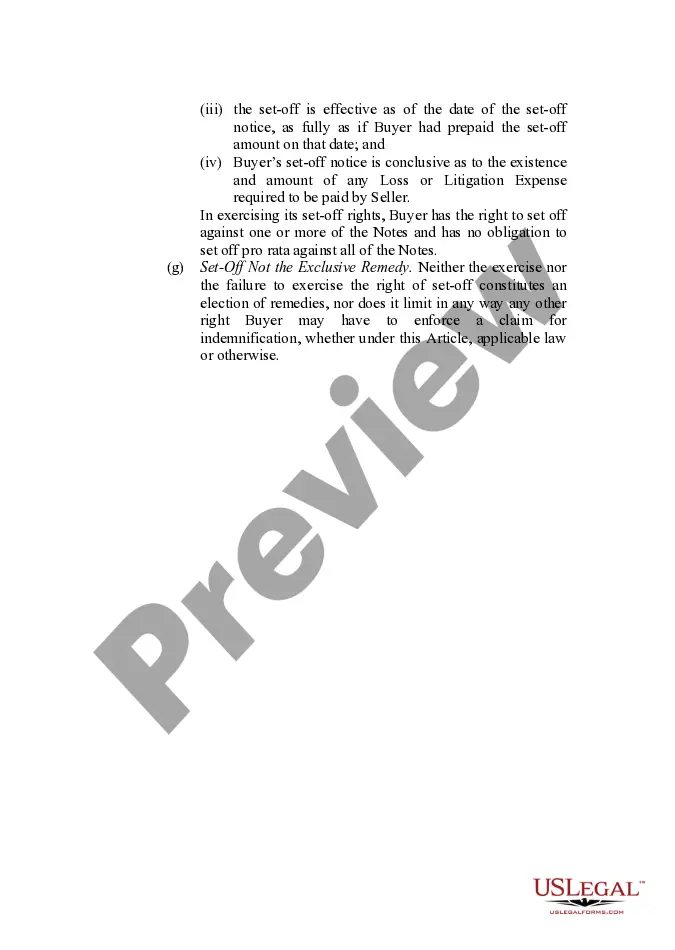

This form provides boilerplate contract clauses that outline means of securing the funds for payment of any indemnity, including use of an escrow fund or set-offs.

Louisiana Indemnity Provisions — Means of Securing the Payment of the Indemnity: In Louisiana, indemnity provisions are crucial in protecting parties from financial loss or liability in various contractual agreements. Indemnity provisions essentially shift the responsibility for certain risks or damages onto one party, known as the indemnity, to provide compensation or financial security to the other party, known as the indemnity. To ensure the payment of indemnity, several means of securing the payment may be implemented. 1. Insurance: One method of securing the payment of indemnity is through the use of insurance. Parties may require the indemnity to obtain liability insurance policies, such as general liability or professional liability insurance, that specifically cover the risks or liabilities outlined in the indemnity provision. By requiring insurance, the indemnity ensures that financial protection is in place in the event of a loss or claim. 2. Surety Bonds: Another means of securing payment under indemnity provisions is through surety bonds. A surety bond is a contract between three parties: the indemnity, the indemnity, and the surety company. The surety company agrees to guarantee the indemnity's performance or payment obligations in the event of default or non-compliance. This essentially provides the indemnity with an additional layer of financial security beyond insurance. 3. Letters of Credit: Letters of Credit (LOC) can also be utilized to secure indemnity payments. An LOC is a document issued by a financial institution, such as a bank, on behalf of a buyer or indemnity. It guarantees that a specified payment will be made to the indemnity upon the occurrence of a particular event, as set out in the indemnity provision. This method ensures that funds are available when needed, giving the indemnity peace of mind. 4. Cash Escrow: In certain situations, parties may opt to secure the payment of indemnity through a cash escrow arrangement. Here, the indemnity deposits a sum of money into an escrow account, typically controlled by a neutral third party. The funds are held until a specified event triggers the release of the money to the indemnity. This method provides a tangible form of security and ensures the payment of indemnity if necessary. By implementing these various means of securing the payment of indemnity, parties in Louisiana can effectively protect themselves against potential financial losses and liabilities. It is important to carefully consider the specific requirements and provisions in the agreement to ensure proper execution and enforcement of the indemnity provisions. Ultimately, these measures contribute to a fair and balanced contractual relationship between the parties involved.Louisiana Indemnity Provisions — Means of Securing the Payment of the Indemnity: In Louisiana, indemnity provisions are crucial in protecting parties from financial loss or liability in various contractual agreements. Indemnity provisions essentially shift the responsibility for certain risks or damages onto one party, known as the indemnity, to provide compensation or financial security to the other party, known as the indemnity. To ensure the payment of indemnity, several means of securing the payment may be implemented. 1. Insurance: One method of securing the payment of indemnity is through the use of insurance. Parties may require the indemnity to obtain liability insurance policies, such as general liability or professional liability insurance, that specifically cover the risks or liabilities outlined in the indemnity provision. By requiring insurance, the indemnity ensures that financial protection is in place in the event of a loss or claim. 2. Surety Bonds: Another means of securing payment under indemnity provisions is through surety bonds. A surety bond is a contract between three parties: the indemnity, the indemnity, and the surety company. The surety company agrees to guarantee the indemnity's performance or payment obligations in the event of default or non-compliance. This essentially provides the indemnity with an additional layer of financial security beyond insurance. 3. Letters of Credit: Letters of Credit (LOC) can also be utilized to secure indemnity payments. An LOC is a document issued by a financial institution, such as a bank, on behalf of a buyer or indemnity. It guarantees that a specified payment will be made to the indemnity upon the occurrence of a particular event, as set out in the indemnity provision. This method ensures that funds are available when needed, giving the indemnity peace of mind. 4. Cash Escrow: In certain situations, parties may opt to secure the payment of indemnity through a cash escrow arrangement. Here, the indemnity deposits a sum of money into an escrow account, typically controlled by a neutral third party. The funds are held until a specified event triggers the release of the money to the indemnity. This method provides a tangible form of security and ensures the payment of indemnity if necessary. By implementing these various means of securing the payment of indemnity, parties in Louisiana can effectively protect themselves against potential financial losses and liabilities. It is important to carefully consider the specific requirements and provisions in the agreement to ensure proper execution and enforcement of the indemnity provisions. Ultimately, these measures contribute to a fair and balanced contractual relationship between the parties involved.