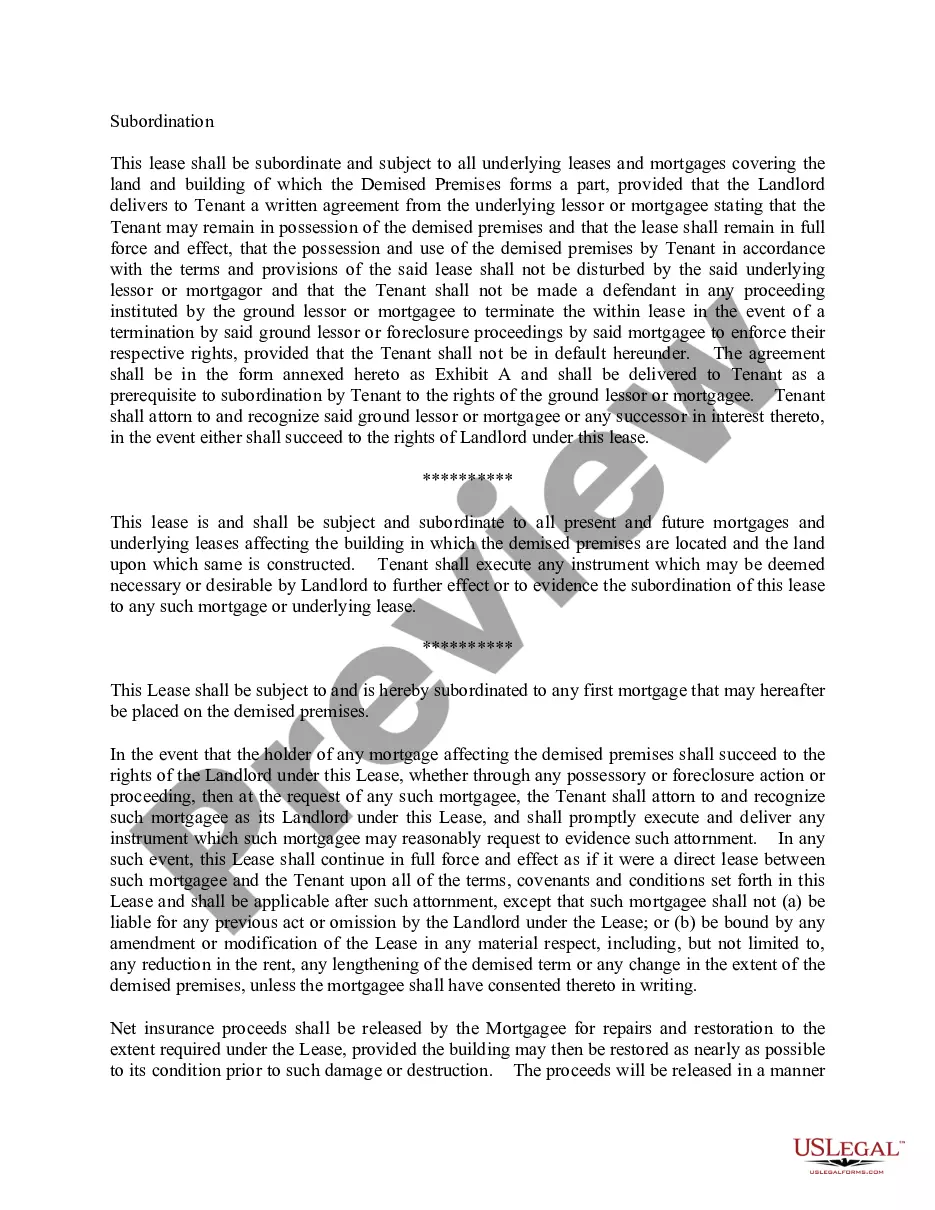

This office lease is subject and subordinate to all ground or underlying leases and to all mortgages which may affect the lease or the real property of which demised premises are a part and to all renewals, modifications, consolidations, replacements and extensions of any such underlying leases and mortgages. This clause shall be self-operative.

Louisiana Subordination Provision

Category:

State:

Multi-State

Control #:

US-OL20022A

Format:

Word;

PDF

Instant download

Description

How to fill out Subordination Provision?

You may commit hrs online attempting to find the legitimate papers design which fits the state and federal specifications you need. US Legal Forms gives a large number of legitimate forms that happen to be analyzed by specialists. You can easily down load or produce the Louisiana Subordination Provision from my assistance.

If you already have a US Legal Forms accounts, it is possible to log in and click the Obtain option. Afterward, it is possible to full, revise, produce, or sign the Louisiana Subordination Provision. Each legitimate papers design you purchase is the one you have eternally. To get another copy associated with a bought kind, proceed to the My Forms tab and click the related option.

Should you use the US Legal Forms site the very first time, adhere to the straightforward recommendations beneath:

- Very first, be sure that you have selected the best papers design for that area/area that you pick. Read the kind description to make sure you have picked the right kind. If available, use the Preview option to check from the papers design too.

- If you want to locate another model in the kind, use the Lookup field to find the design that fits your needs and specifications.

- Upon having found the design you want, simply click Get now to continue.

- Select the pricing program you want, key in your qualifications, and register for your account on US Legal Forms.

- Total the transaction. You may use your charge card or PayPal accounts to fund the legitimate kind.

- Select the structure in the papers and down load it to the device.

- Make changes to the papers if necessary. You may full, revise and sign and produce Louisiana Subordination Provision.

Obtain and produce a large number of papers layouts utilizing the US Legal Forms website, which offers the greatest assortment of legitimate forms. Use skilled and condition-specific layouts to take on your company or personal needs.

Form popularity

FAQ

Unless otherwise directed by the state or defendant, subpoenas shall be served by domiciliary service, personal service, or United States mail as provided in Paragraph B. Personal service is made when the sheriff tenders the subpoena to the witness.

Now listen up ? this is important. If you ignore the subpoena and don't show up, here's what could happen: You may be charged with contempt of court, which can mean fines or even jail time. The court could issue a warrant for your arrest.

Concomitantly, Louisiana Code of Civil Procedure Art. 1313(c) now permits service of court dates and deadlines to be served on an unrepresented party or attorney of record via e-mail. Of note, service is not complete unless the sender is in receipt of an electronic confirmation of delivery.

On motion to compel production or to quash, the person from whom production is sought shall show that the information sought is not reasonably accessible because of undue burden or cost. If that showing is made, the court may nonetheless order production from such sources if the requesting party shows good cause.

There are two types of service: personal service and domiciliary service. The law requires personal service in some kinds of cases and allows domiciliary service in other kinds of cases. Personal service means the "proper officer" directly delivers the paperwork to the person to be served.

Failure to respond to a subpoena is punishable as contempt by either the court or agency issuing the subpoena. Punishment may include monetary sanctions (even imprisonment although extremely unlikely).

A rule to show cause is a kind of motion. A motion asks the Court to do something. The Court acts by entering an order. Before the Court will enter most types of orders, the Court will first have a hearing where both sides are allowed to present evidence and make arguments on their own behalf.

Louisiana Laws - Louisiana State Legislature. Majority is attained upon reaching the age of eighteen years.