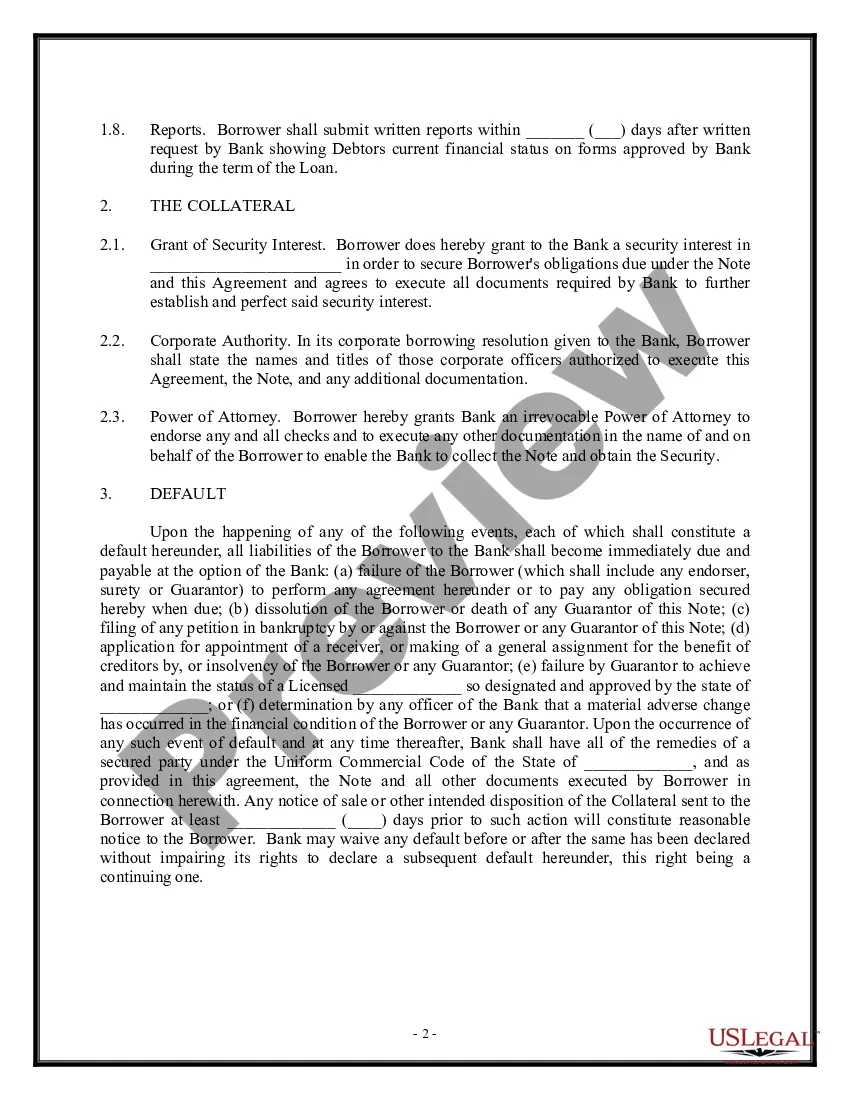

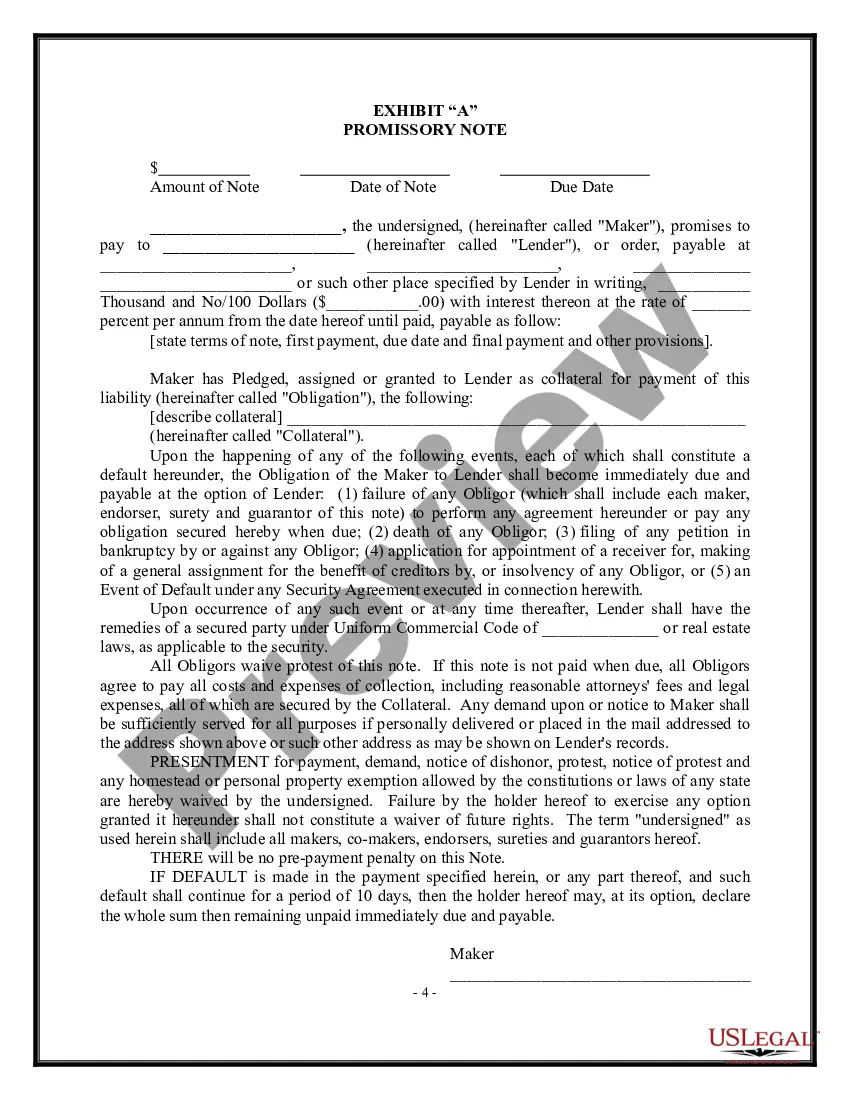

A Massachusetts Loan Agreement — Short Form is a legal document designed to outline the terms and conditions of a loan between two parties in the state of Massachusetts. This agreement is used when the loan amount is relatively small and the parties involved want a concise and straightforward contract. The Massachusetts Loan Agreement — Short Form typically includes essential elements such as the names and contact information of both the lender (often referred to as the "creditor") and the borrower (known as the "debtor"). It also includes the principal loan amount, the interest rate (if applicable), and the repayment terms. Additional provisions in the agreement may cover topics like late fees, prepayment penalties, and the date by which the loan must be fully repaid. There may also be sections addressing the consequences of default or breach of the agreement by either party. Different types of Massachusetts Loan Agreement — Short Form may include: 1. Personal Loan Agreement: This type of agreement is used when an individual lends money to another individual. It can be for any purpose, such as covering personal expenses, purchasing a vehicle, or financing a small business. 2. Business Loan Agreement: This agreement is specifically tailored for loans involving a business entity. It outlines the terms and conditions for borrowing money to fund business operations, expand business activities, or invest in assets. 3. Promissory Note: While not technically a type of loan agreement, a promissory note is often used in conjunction with a Massachusetts Loan Agreement — Short Form. It serves as written evidence of the borrower's promise to repay the loan and includes details such as the repayment schedule, interest rate, and any collateral involved. 4. Family Loan Agreement: This type of loan agreement is used when a loan is made between family members or close friends. It allows for more flexibility and informal terms but still ensures legal protection for both parties. In summary, a Massachusetts Loan Agreement — Short Form is a concise document that clearly defines the terms and conditions of a loan within the state. It can vary depending on the nature of the loan, such as personal, business, or familial. Having such an agreement in place provides legal protection and promotes transparency between the lender and borrower.

Massachusetts Loan Agreement - Short Form

Description

How to fill out Massachusetts Loan Agreement - Short Form?

Are you in the place that you need to have files for either business or personal functions virtually every working day? There are plenty of legal record templates available online, but locating ones you can depend on is not effortless. US Legal Forms delivers a huge number of form templates, like the Massachusetts Loan Agreement - Short Form, that are published in order to meet federal and state demands.

In case you are currently familiar with US Legal Forms website and have your account, basically log in. After that, you can down load the Massachusetts Loan Agreement - Short Form template.

Should you not provide an account and wish to begin using US Legal Forms, follow these steps:

- Obtain the form you require and ensure it is to the appropriate city/county.

- Utilize the Review key to review the shape.

- See the description to ensure that you have chosen the appropriate form.

- When the form is not what you`re looking for, take advantage of the Search discipline to discover the form that meets your requirements and demands.

- When you get the appropriate form, simply click Buy now.

- Choose the pricing plan you need, submit the specified information to produce your account, and pay money for the order with your PayPal or bank card.

- Pick a practical file formatting and down load your backup.

Discover all the record templates you might have bought in the My Forms food selection. You can get a further backup of Massachusetts Loan Agreement - Short Form whenever, if necessary. Just go through the essential form to down load or produce the record template.

Use US Legal Forms, probably the most considerable collection of legal forms, to save time and steer clear of mistakes. The support delivers appropriately produced legal record templates which can be used for a variety of functions. Make your account on US Legal Forms and begin producing your way of life a little easier.